The IEA World Energy Outlook for 2013 is out and it’s a very mixed bag for Australia. From the FT:

Its 2012 forecast that the US would be a net oil exporter by 2030 helped bring shale oil production to global attention. But this year the organisation downplayed the significance of US production growth, with Mr Birol calling shale “a surge, rather than revolution”.

The IEA still expects US oil output to reduce the world’s dependence on Middle Eastern oil in the near term: it now forecasts that the US will displace Saudi Arabia as the world’s biggest oil producer in 2015, two years earlier than it had estimated just 12 months ago.

But it expects US light tight oil production, which includes shale, to peak in 2020 and decline thereafter, even as global demand continues to grow to 101m barrels a day by 2035, from about 90m b/d today.

In part this is why, as the SMH reports, Australian energy will be in demand:

Surging energy demand in Asia will deliver ”a golden age” for the Australian economy but also set the world on a path of dangerous climate change as fossil fuel-sourced emissions soar, according to the International Energy Agency.

China will soon dislodge the US as the world’s biggest oil importer and India will be the largest coal importer by the early 2020s as the centre of energy demand shifts ”decisively” to emerging economies, the IEA said in its World Energy Outlook 2013 report.

Asia will ”need every bit of Australia’s energy exports … coal, gas and maybe even uranium,” Fatih Birol, chief economist for the energy group, said. ”I see a golden age for the Australian economy to come, looking at the export volumes … and the prices we expect.”

Australia, the world’s largest exporter of coking coal, will regain the title of biggest overall coal exporter by 2030. Shipments of coking and thermal coal will rise 57 per cent from 2011 levels to 410 million tonnes per year by 2035, the report said.

With two-thirds of the world’s total investment in liquefied natural gas pouring into Australia, the country will rival Qatar as the largest LNG exporter by 2020. Three of Australia’s seven export projects under construction tap coal-seam gas, production of which will leap from 6 billion cubic metres in 2011 to 100 bcm by 2035 – provided sensitive water management issues can be resolved, the report said.Rising global demand, though, will come with a hefty climate cost. Energy-related greenhouse gas emissions – now about two-thirds of the total – are likely to rise by 20 per cent to 37.2 gigatonnes by 2035, according to IEA’s mid-range scenario. ”Some people talk about the ‘green growth’ in Asia. When I look at the numbers … it’s black growth,” Dr Birol said.

Hmm, well, aside from the fact that our civilisation may collapse, that sounds pretty good.

Climate change aside, there are some inconsistencies. In the LNG component of the report, the IEA also sees the following:

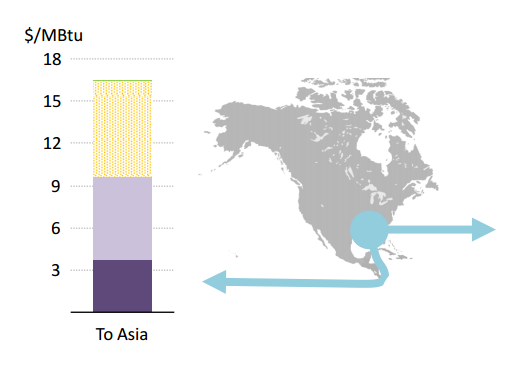

That’s some awful cheap LNG to Asia from the US, at under $10 it’s below my forecasts, leading to this:

A process of energy cost equalisation (within reason).

Remember that Australia’s new wave of LNG projects has a break even point around $12 mmbtu. So the future is blindingly bright except for a climate calamity and our big LNG projects having no profit margin.

The full report is purchase only but a fact sheet is available here.