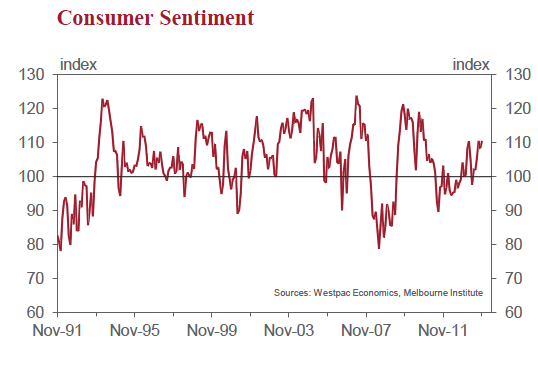

• The Westpac Melbourne Institute Index of Consumer Sentiment increased by 1.9% in November from 108.3 in October to 110.3 in November.

After a modest fall last month the Index has returned to be back near its previous peaks in 2013 registered in March and September. These are the highest reads since the July-December period in 2010 when the Index averaged an impressive 114.

It is encouraging that the Index has returned to these levels after it surged 4.7% in September following the election result.

The survey was conducted in a week when the Reserve Bank kept rates on hold and the unemployment rate was reported to have held at 5.7%. Importantly, house prices were reported to have risen by 1.9% in the September quarter, with prices in Sydney rising by 3.6% to be up by 11.4% for the year. Melbourne house prices were reported to have risen by 1.9% for a yearly gain of 6.8% while movements in Brisbane (1.2%qtr; 4.1%yr); Perth (0.2%qtr; 8.6%yr) and Adelaide (–0.6%qtr; 1.0%yr) were less impressive. Not surprisingly, the confidence of respondents who wholly own their house was boosted by 6.1% whereas those folks who are renting registered a drop in confidence of 2.8%.

This theme around the impact of house prices on confidence was apparent in the state measures. State Consumer Sentiment Indexes were up 7.7% in NSW and 3.2% in Western Australia but rose only 0.9% in Victoria and fell by 4.2% in Queensland and 8.3% in South Australia.

While the unemployment rate was reported unchanged in October (albeit due to an upward revision to the September reading) the October labour force report depicted a very weak labour market.

Over the 4 months to October the economy actually lost 42,000 full time jobs. The unemployment rate did not rise over that period only because workers have been voluntarily leaving the work force altogether, likely in part because they feel discouraged in their job search. This weakness continues to be apparent in the measure of unemployment expectations in the Consumer Sentiment survey. The Unemployment Expectations Index rose by 0.9% in November to reach 144.7. That is 11% above the level in November 2011 whereas the Consumer Sentiment Index is 6.7% above its level in November 2011. In effect despite the Reserve Bank reducing interest rates by 225 basis points since November 2011 and Consumer Sentiment increasing respondents are more concerned about the outlook for unemployment, and by implication their job security, than they were two years ago.

Confidence around the housing market was also apparent in the Index of House Price Expectations which rose by 3.1% to be 23% above its October 2012 level. There was also a rise in the “Time to Buy a Dwelling” Index of 4.2% including a very strong increase in NSW, solid rises in Western Australia and Queensland but falls in Victoria and South Australia.

This strong housing theme was also apparent in components of the Consumer Sentiment Index. The sub-index tracking assessments of “family finances vs a year ago” increased by 13.3%, presumably boosted by respondents’ assessment of the increasing value of their housing asset. However in a sign that the medium term outlook may not have been as supportive, the subindex tracking expectations for “family finances next 12 months” fell by 7.9%. The sub-indexes tracking views on the economic outlook over the next year were largely unchanged. In a sign of related confidence around housing and the apparent lift in wealth there was a 4.4% rise in the sub-index tracking views on “whether now is a good time to buy a major household item”.

The Reserve Bank Board next meets on December 3. In its recent Statement on Monetary Policy the Bank lowered its growth forecast for 2014 from 3% to a below trend 2.5%. It also indicated that “it was appropriate to hold the cash rate steady, but not to close off the possibility of reducing it further”. As indicated in this report some of the big issues for policy are around a very strong housing market in some regions of the country, particularly Sydney, and very soft job markets. The Bank is clearly positioned to await developments in these areas over the course of the next few months. For our part we believe the prudent decision would be to ease rates further but not before more data is available.

That rules out the December meeting and could make even February doubtful although, at this stage, we think the best policy response will be to cut in February.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.