Regular reader will recall that MB uses a “five drivers” model of Australian dollar valuation. Six weeks ago I described how they were turning bullish for the currency. A fortnight ago I described how that had reversed.

Revisiting those drivers today and it’s a still weak picture:

- interest rate differentials;

- global and Australian growth (more recently this has become more nuanced for the Aussie to be more about Chinese growth);

- investor sentiment and technicals; and

- the US dollar

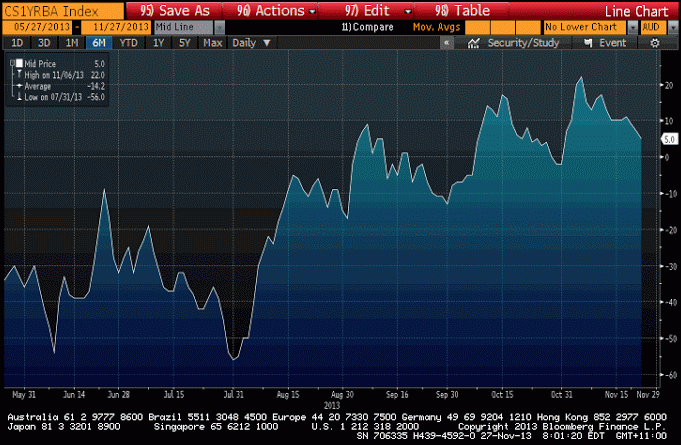

First, interest rate differentials are still favourable to the Aussie but the widening of the spread has stalled. Local interest rate markets have almost priced out all rate rises for next year now:

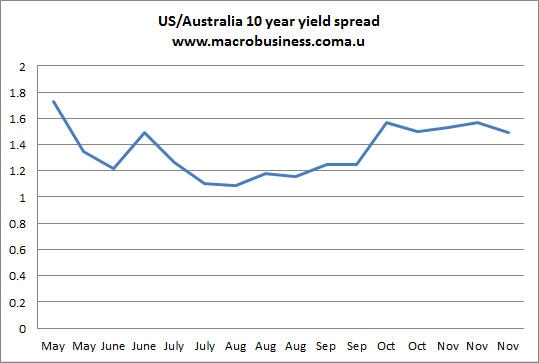

And the spread between US and Australian ten year bonds has plateaued in the past month:

Taper remains on the radar for early next year despite mixed US data flow. The US ten year is facing less upwards pressure as taper wavers but it’s still more pressure to appreciate than our local rates as the RBA turns bearish and deploys the jawbone.

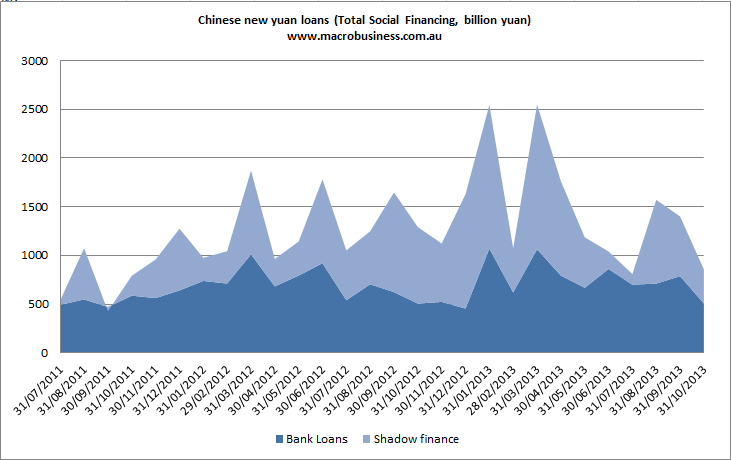

On driver two – global, local and Chinese growth – I would describe where we’re at as the “peak is in”. Although global growth may accelerate next year, Chinese growth is going to slow over the next six months. The evidence for this is declining lending:

And the emptying fiscal stimulus pipeline:

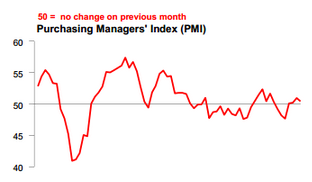

The Plenum was also largely Australia neutral or negative and the Flash PMI is suggesting the better part of this Chinese growth pulse is behind us:

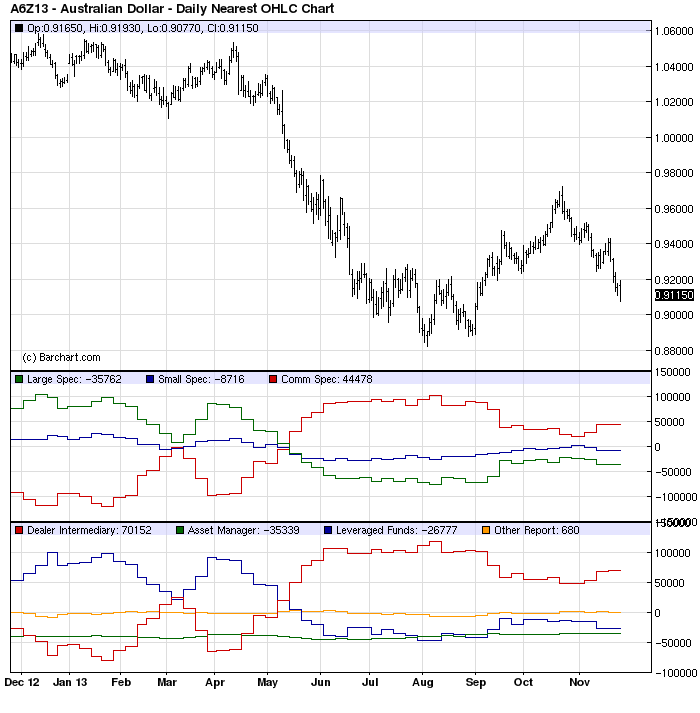

Drivers three and four are also weakening for Aussie bulls. Technicals show a monstrous head and shoulders pattern with a break of support at 92.8 cents:

As well, the Commitment of Traders report is showing large and small speculators getting more short but far from extremes. I would not underestimate the impact of the RBA on sentiment, either. The threat of unorthodox policy intervention and the jawbone are very clearly deployed. We also have a string of very significant reports in the next few days measuring the capex cliff (BREE then ABS) and the indications in advance are that they will not be pretty.

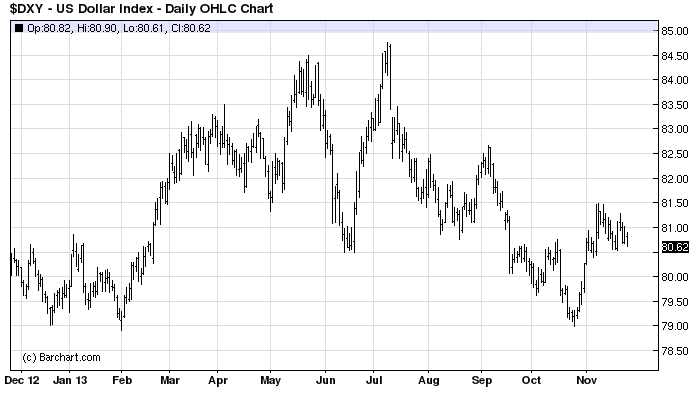

On the fifth driver, the US dollar is looking less strong than it was as taper expectations waver but a messy bottom is still in:

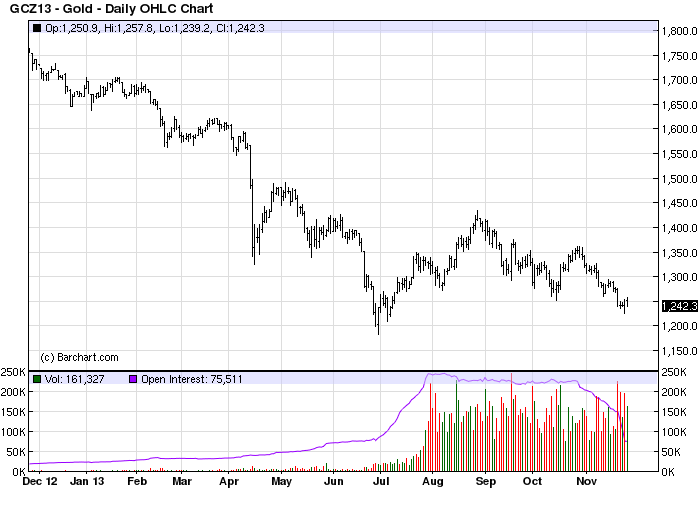

And gold, the undollar, is still weak as well, also with a head shoulders top in place with a downside break:

A test of this year’s low is not a crazy thought on this chart.

On balance, it looks to me like the five drivers for the Australian dollar still point down despite wavering over the taper, hence last night’s going against the ‘risk on’ tide.