Bill Evans wrote a stinging critique of RBA policy late Friday with which I mostly agree:

One of the critical outcomes from the Reserve Bank’s move to lower the overnight cash rate from 4.75% to 2.5% over the last 2 years has been the response of business to these lower rates.

The slowdown in mining investment is mainly a function of the large lumpy projects in the gas sector which are now approaching completion over the next few years. The Access /DL construction monitor lists the value of oil and gas projects currently under construction as $200bn compared to $12bn in iron ore and $14.4bn in coal.

Committed new projects in oil and gas total only $3.7bn compared to only $6.3bn in iron ore and $15.2bn in coal.

We estimate that mining investment will fall as a proportion of GDP over the next 5 years from 8% to 3% (RBA estimates “3 percentage points or more”). Even after adjusting for the imported component of this investment it is still a significant drag on an already fragile economy over the next few years. Reserve Bank Deputy Governor Lowe discussed prospects for non mining

investment in a speech to the CFA Australia Investment Conference on October 24.

He listed the recent boost to business confidence; low interest rates; and the 8% fall in the AUD since April as reasons for optimism (note that following the September RBA Board meeting that depreciation was estimated as 15%).

However on business confidence he did note that “a fair amount depends on international events”.

Governor Lowe also noted “the profile of non mining investment in Australia is not dissimilar to the profile for overall investment in many of the developed economies”.

A key theme supporting our view that interest rates are in need of further reduction revolves around our more downbeat view of the world economy in 2014. We forecast growth in the world economy in 2014 of 2.8% compared to 3.6% for the IMF and the Reserve Bank. Such a weak growth environment is likely to be associated with ongoing weakness in business investment in the developed economies. Our view of domestic non mining investment is likely to be considerably more downbeat than the Reserve Bank and the IMF.

If the global economy is a key determinant of domestic business investment it is also likely to be a key driver of the decision by businesses to raise employment plans.

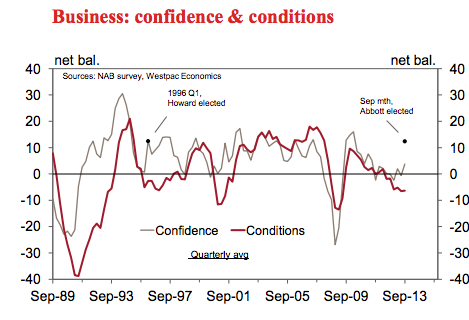

Fig 1 highlights the current challenges facing the Australian economy. It tracks current measures of business confidence and business conditions.

…The Australian economy experienced a similar situation from March 1996. With the Coalition being returned, after 13 years in Opposition, we saw a spike in business confidence from 0.7 to 12.4. Unfortunately business conditions did not follow through with conditions averaging -4.7 over the next 12 months.

Exactly right. The RBA is underestimating the capex cliff and is barking up the wrong tree with its focus on the “power of positive thinking” yoked to cheap money. Where I part from Bill Evans is in his conclusion that lower still interest rates are the answer. Lower interest rates alone will only put more upwards pressure on asset prices via financial repression. A screaming blowoff in Sydney property prices is already underway and the stock market is also beginning to stretch sensible valuations, especially in sectors exposed to a supposed new cyclical consumer boom.

Advertisement

This is not a problem that is unique to Australia. All over the world major economies are struggling with financially repressed interest rates, bubbly asset markets and unresponsive real economies. In China and Brazil, the UK and peripheral Europe and North America the story is the same. A great divergence is developing between the rise of asset prices and unresponsive economic growth. It is a war against the debt-deflation described by Irving Fisher, Hyman Minsky and Richard Koo and is the hallmark of this business cycle, as well as being its ultimate denouement. An entire cycle dedicated to, and driven by, ponzi finance.

It can only end badly.

So how does it end? It is not obvious to me where the next accident will come from. It could be China and its shadow banking system. It could be a bursting of commodity prices as China rebalances. It could be a self-inflicted US fiscal wound or a second bust in its housing or stock market. It could be an unintended fourth arrow to the heart of Abe’s great reflation. It is less likely to be a European sovereign default for now.

Knowing when is no easy matter either. So long as financial repression proceeds, markets remain investable or, more to the point, tradable, given there is no real investment case for any of it. Asset markets are dysfunctionally propped up by liquidity, economies are debt-saturated and on life-support, demand wants to deleverage but is prevented, previously differentiated markets are correlated to one but the whims of monetary support make the timing of any unwind opaque.

Advertisement

That at least provides a clue. As almost happened this year in both the US and China, financial repression will create financial instability risks that are so obvious that monetary authorities will be forced to tighten sooner or later. The prospect of real economy inflation is negligible as over-capacity and paucity of demand keep it in check. But asset prices are something else. This year when Fed and the PBOC toyed with tightening, neither was doing so because of real price inflation. Both did so despite an obvious lack of it. Asset price inflation was their target and when one or both actually does follow through with tightening you will know it is time to duck.

Which brings us back to Australia and Bill Evans’ advice. The RBA has already taken us part way into the same yawning chasm as Sydney house prices rocket yet the construction cycle remains muted and so does retail. From the weekend AFR:

Retailers are bracing for a tough Christmas on signs the sentiment boost delivered by the Coalition’s victory last month has waned and growing fears of a lingering business investment strike.

As economists warned that real-world business conditions have failed to match last month’s confidence spurt, outdoor adventure wear retailer Snowgum was placed in administration after operating since 1926 as Scouting shops.

Snowgum managing director Ross Elliott said the final straw was a recent slump in sales following a short-lived increase immediately after the September 7 election.

“The last few weeks have been pretty flat,’’ he said in an interview.

Wesfarmer chief executive Richard Goyder on Thursday said discretionary spending jumped in the week after the election and quickly reverted to where it started.

Another retail chief, John Pollaers – of workwear maker Pacific Brands – warned this week that retail conditions are “far from ideal” and likely to remain so.

Greg Hywood, chief executive of Fairfax Media, publisher of AFR Weekend, said there had been no post-election pick-up.

“You look at the people reporting [results] at the moment, I was just having a conversation with a retailer just yesterday,” Mr Hywood said on Friday. “I think it’s pretty clear that there hasn’t been a post-election bounce in the economy. It’s pretty clear. We see it, everyone sees it.’’

National Australia Bank chief economist Alan Oster, who publishes a closely-watched gauge of business sentiment, said the remarks from company chiefs supported what he had been saying since the federal poll.

“Confidence went up, but conditions didn’t change,” he said. “There was an element of people saying ‘right we’ve got rid of the government we didn’t like,’ so the animal spirits improved.

Advertisement

My base case is that this will ease but that the soft trend will continue. Households may not understand the detail but they know in their bones what is happening: this cycle is a phoney and asset prices can no longer be trusted to fund future standards of living. Thus I reckon the laudable savings rate will remain high and growth will remain materially below trend to the chagrin of those that have drawn a fallacious correlation between confidence and spending.

In the mean time, the asset price inflation that the RBA has unleashed will have other negative consequences in the real economy. Higher asset prices raise input costs, wages and the dollar. In short they destroy competitiveness. Friday’s Electrolux closure is only the latest casualty in a long line of such accidents with many more to come.

So, when will the cycle end here? There are four possible scenarios that I see. Here they are, listed in order of probability.

Advertisement

If my base case is right then at some stage in the not too distant future, perhaps mid next year, as Sydney house prices shoot towards the moon but the economy only chokes on the vapour trail, the RBA will recognise it has both a weak economy and an asset bubble on its hands. At that point the bank will recognise that it needs to find a new source of growth to bridge the gap and it will turn to the policies now being deployed in New Zealand. The economic cycle in our near neighbour is more heated and mature than here yet my bet is it will not have to raise interest rates because its macroprudential tools will work to suppress credit and hold down the kiwi dollar. The RBA will follow, slowing the Sydney bubble in a repeat of the stagnation of 2003 and preventing any other market from joining the blowoff. Interest rates will be cut further to prevent any ‘hard landing’ and the dollar will fall sharply by year end, boosting all tradable sectors. Growth will still be below trend for years but at least it will be real growth and begin the path of healing competitiveness. This is the most probable path ahead for the simple reason that its the most viable.

The second scenario is less rosy. It is that the bank follows the advice of Bill Evans and pursues further interest rate cuts. In that event, the Sydney bubble will head for the outer solar system and could spread to chronically oversupplied Melbourne or the other stagnant capitals. Yet if households still do not spend, such a cycle ends in a huge bust in a year or so as the real economy falls away beneath asset prices and the capex cliff steepens. This will exhaust the RBA’s monetary ammunition for the following cycle and stoke the kind of fiscal madness we now see in the UK and US in which government becomes the explicit lynch pin in private mortgage markets, seeking to support the unsupportable. This is moderately probable.

The final scenario is that both Bill Evans and I prove to be wrong and consumers plunge into renewed spending, non-mining investment responds as the RBA hopes and the economy sling shots across the mining capex chasm. In that event the cycle will be prolonged and interest rates will begin to rise later next year. The earnings gap in the stock market will be filled and Australia’s develeraging will be postponed for another more severe correction in the future. I see this as the least likely for two more reasons. By definition it will mean an overly high dollar killing the productive economy and thus anything short of boom-level consumption will not be enough to sustain growth. As well, inevitably, it will require the renewal of expansion in the major banks’ foreign borrowing which will take a reckless policy shift at APRA to match that already underway at the RBA, not to mention the acquiescence of global markets to a deepening current account deficit. In other words, there’ll have to be no new normal.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.