We all know these days that the Australian economy is bogged down in over-concentration. In every major sector, duopolists and oligpolists reign. Whether it’s banks, supermarkets, retailing, airlines, utilities, resources, media, packaging, food and beverages, you name it, competition is thin on the ground.

We pay a high price for this in entrenched inflation and lousy productivity but increasingly, it appears, we are also paying a price in our liberal democratic system.

One doesn’t like to be alarmist about such things but there is a pattern of behaviours that is accelerating and the casual observer might join the dots and see a shift in Australian democracy away from sound principle and the rule of law.

Consider. The last three elections have all been unduly influenced by powerful interests. The 2007 result in favour of Kevin Rudd was considerably aided by a union funded advertising campaign against Work Choices. Along with climate change, it was the defining issue of the campaign.

In the 2010 election it was a the mining interest’s turn to distort process via public pressure on the mining tax legislation. After that result, the new Labor Government allowed the three big miners to write their own tax rates that have since been shown to have gutted the attempted tax.

The most remarkable result in the recent election was not that the Labor Government got tossed out but that a mining magnate took just a few weeks to buy the balance of power in the Senate. It is he that will now determine whether or not such legislation as the carbon and mining taxes are abolished altogether, unencumbered by legal or ethical constraint.

It doesn’t stop there. In the post-GFC context, we have also seen a dramatic confusion of interests in the public and private obligations of the banking system. Australian tax-payers now guarantee or fund, explicitly or implicitly, most of the liabilities in our financial system. We do this with almost no quid pro quo, with no control over the companies benefitting and no pecuniary offset. Our regulators , those tasked with governing this melange, exist in a bubble of secrecy. We have no idea what their benchmarks are, whether they are appropriate, what values they represent, nor what their long term goals are.

This has been engineered in crisis but is yet to be examine in the open. And when it is, what hope is there that interests won’t dominate the discussion?

And wider business has learned the lessons of these repeat episodes. We are now daily exposed to vested interests propaganda campaigns in which businesses seek favour via ballot box intimidation and our professional political class seems to have no compass beyond power to see off these attacks.

Now, in the past couple of days, we have also had a series of corruption allegations revealed against the Reserve Bank of Australia, which the Australian Securities and Investments Commission inexplicably failed to investigate, and today a new set of explosive allegations against corporate superstars Leighton Holdings which, again, ASIC has failed to investigate. Our elite police appear compromised in one way or another.

This is not a local problem. Increasingly it is an issue worldwide, in political systems on both the Left and the Right. In China, a fading developmental model is now universally recognised to require revitalisation. But in the way are the interests that benefit from the old ways and the outcome of the struggle is as yet unknown.

We have all marveled at the manner in which the GFC unfolded around the Wall Street coup in Washington. From the capture of financial regulators to the funding of politicians, Wall Street elites blew up the American economy as they feathered their own nests and virtually none have paid any price since. Much the same can be said of the UK.

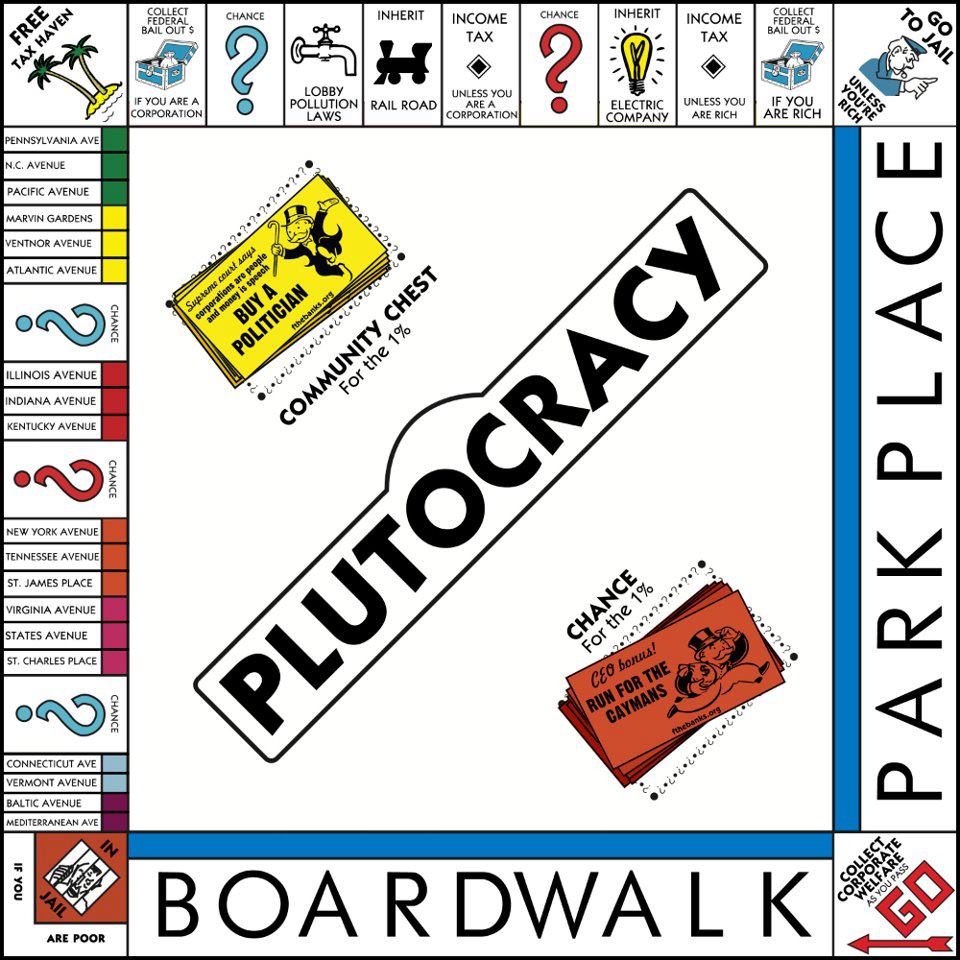

Increasingly, it seems, a globally motivated super-elite come and go as they please, a plutocracy of wealthy individuals that are above the law, indeed they seem able to make the law.

An economist with the International Monetary Fund, Fred Hirsch, has treated these issues. In his book, Social Limits to Growth, Hirsch argued that the modern market economy is successful only to the extent that it stands on the shoulders of a pre-capitalist ideology. He was concerned that the growth and maturation of the market economy undermined the moral and ideological foundations upon which it depended. The market economy depends on respect for rules that cannot be enforced by law alone. It depends on the owners of business being permitted to maximise their own wealth and incomes in certain defined ways, and on others in society foregoing the opportunity to take advantage of their own positions to do likewise.

Hirsch presented a pessimistic prognosis for capitalism: ‘As the foundations weaken’, he concluded, ‘the structure rises ever higher’.

Who can say Australia is immune?