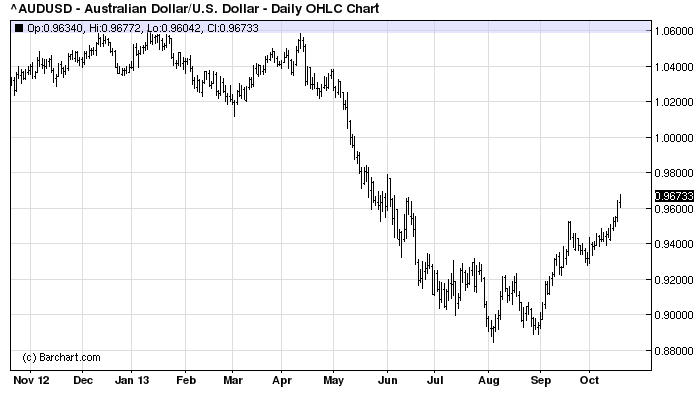

The MSM echo chamber was in full swing over the weekend with the untouchable RBA again taken at face value on questionable statements around the rising Australian dollar, which had another hot night Friday and is now sailing happily towards 97 cents:

The AFR quoted Captain Glenn:

Reserve Bank of Australia governor Glenn Stevens has warned he lacks the power to stem the rise of the dollar as business leaders say they are being forced to cut costs to cope with the higher currency.

…“I personally think a lower currency than this will be helpful in rebalancing the growth sources of the economy. Whether it’s in my gifts to make that happen is another question,” Mr Stevens said at a lunch for the Australian British Chamber of Commerce.

“Fundamentally, I don’t think you could really credibly say that the level of cost and productivity in Australia, on those metrics, would point you to present or higher levels being really sustainable.”

This refrain of impotence is bizarre. The RBA is not at all helpless. It is very obvious what if could do to lower the dollar:

- announce the intention to add macroprudential tools to its monetary toolbox, and

- make it clear that it will keep cutting rates until the dollar reaches whatever target it likes

Not only is the bank not impotent, it is actually pushing the currency up. It’s jawboning around the currency has been weak and it’s failure to act on bubbly house prices has markets thinking that there’s a reasonable prospect of rate rises in the year ahead. Should we really be surprised that the dollar rises when on the same day that Captain Glenn tells markets that he’s currency impotent, his head of financial stability demonstrates total complacency about house prices?

The bank is not entirely to blame. The fiscal regime also encourages a high dollar and the tax and microeconomic reforms needed to reverse this are the responsibility of politicians. But in New Zealand the embrace of macroprudential policy by the central bank has forced politicians to act on such questions as housing supply so, again, the RBA is not powerless.

The excuse that the RBA can’t move towards macroprudential because that is APRA’s job is also thin. The division of regulatory responsibilities proved no impediment to radical and wholesale changes to Australian financial architecture during the GFC. Getting the Council of Financial Regulators together to nut out a macroprudential regime is paltry by comparison.

Some will point to the fact that the rebound in the dollar has coincided with the pushing out the US “taper” as an excuse too. But that’s not the point. As the weekend’s Martin Wolf video made abundantly clear, that’s old news. We aren’t going back to the old normal for a very long time, if ever, and interest rates in the developed world are structurally lower. The carry trade into the Australian dollar based upon interest rate differentials is a hallmark of whatever period we are now in and the longer it isn’t addressed the worse will be the ultimate outcome for the economy.

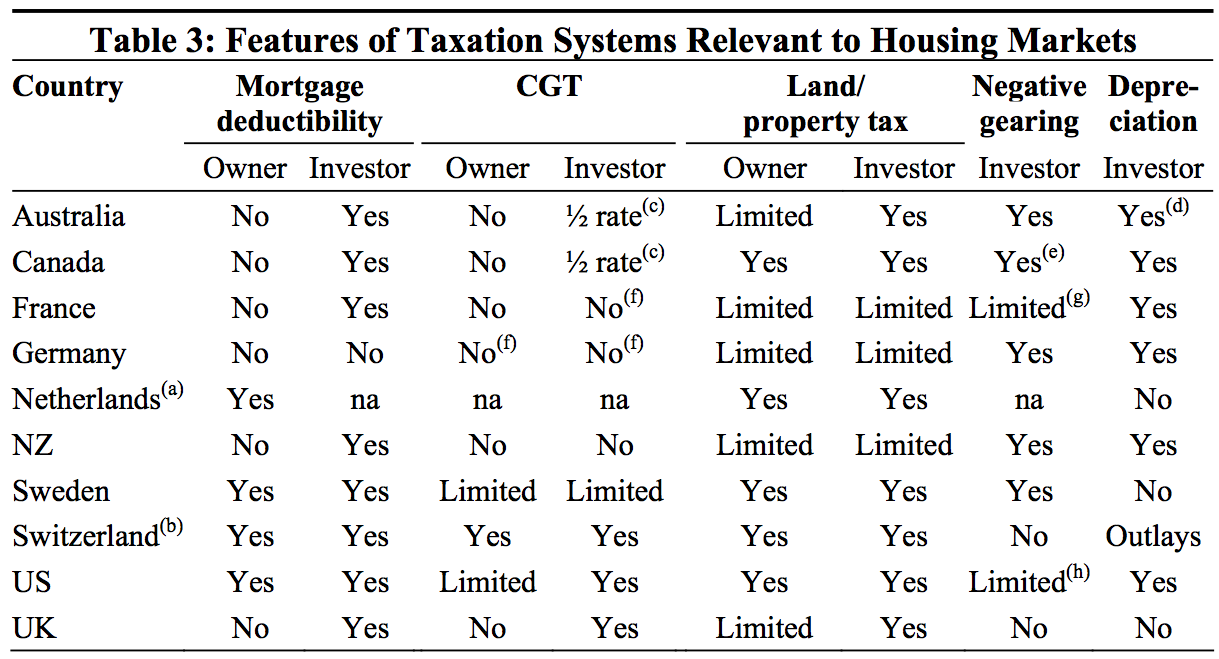

Others will use the paper thin excuse that we can’t interfere in markets. As if the fiscal and monetary settings we already have carry the power of objective truth. Nothing could be more wrong. Our settings are unique to our economy and are causing the high dollar in the first place. Check out the below chart from the RBA on housing tax policies (2006) across differnt countries and see if you can find a pattern of objective truth:

Nope.

For over two years MB has been pushing macroprudential as the solution to the high dollar. It is now recommended as well by a growing phalanx of local economic doyens, and central banks all over are beating us to it.

The RBA doesn’t lack the power to lower the dollar, it lacks the will.