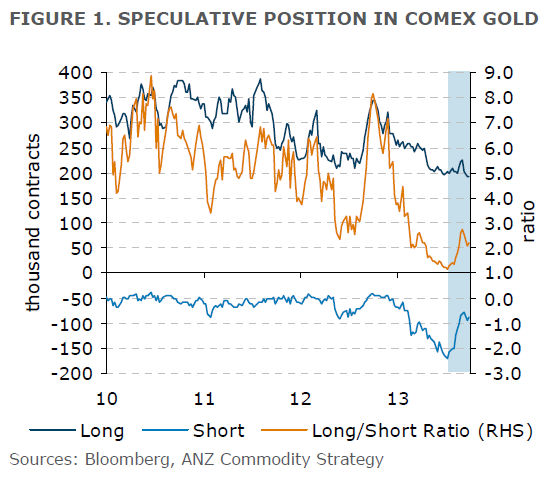

The speculative community is cautious of buying back into gold. Most of the recovery off the 3-year low reached in June can be attributed to short-covering. But while the shorts have been taking profits, we are yet to see an increase in positions from investors who want to own gold. In the same time that speculative shorts have halved from 171k contracts to 86k, longs have barely changed. The ratio between the two (longs/shorts) remains near record lows (Figure 1).

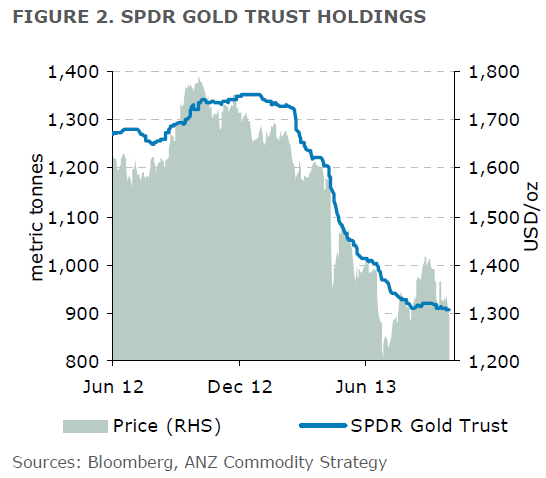

Gold ETF investors, regarded as long-term holders, have also begun selling gold once again. After some stabilisation in the past few weeks, gold holdings in the SPDR Gold Trust have resumed their downward trend and are now making fresh lows. As of yesterday, holdings in the Trust reached 906 metric tonnes, down from 921 metric tonnes at the end of August.

In the Asian physical centres, the price signals are mixed.

In India, the depreciation of the Indian Rupee pushed the local price of gold to a record high of Rs32,900/10g in late August, but traders were largely unable to take advantage of the price differential due to restrictions put in place by the Reserve Bank of India.

However, a positive development is the recent clarification (though not relaxation) of the import rules which have seen imports rise to 7.2 tonnes in the first three weeks of September, from 3.4 tonnes in August. This is supportive, but Indian demand remains substantially lower than the average monthly import volume in 2012 of around 70 tonnes.

The RBI will continue to limit gold imports should activity pick up substantially. Domestic refiners/jewellers are likely to increasingly turn to the scrap market for supply.

…In China, demand in the physical market remains buoyant, but the premium that the market is willing to pay has contracted.

In recent weeks the local gold price fell close to the early August lows and this is proving an attractive entry price for Chinese investors. Deliveries against the Shanghai Gold Exchange’s main gold contract reached 225 metric tonnes in September, the highest monthly deliveries since June, when the domestic price was around 10% lower. The demand side remains supportive of continued strong import volumes.

However, the spread between the Shanghai price and the global price continues to move steadily lower. Last week, the spread over the five trading days averaged USD10/oz from USD25/oz in early-August. Despite local gold prices at roughly the same level (in both USD and CNY terms), the domestic premium over spot gold has halved, suggesting that the financial incentive for traders to import gold for the domestic market is decreasing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.