There is a simple way to understand the Australian economy. It’s not the miracle that outsiders deem it to be. Nor is it the fruits of magisterial management by the RBA or government that some claim.

It is this: we get income by selling our dirt overseas, then we leverage up those earnings with offshore loans and blow it on houses. That’s all there is to it.

Most developed economies do not work this way. Most have sophisticated value-added production sectors that determine their income. Thus, some such countries have suffered as developed economies have encroached on the labour-intensive parts of that production.

Some of these developed economies have responded by adding more value to their exports and moving beyond the reach of developing competitors. But others, accustomed to high standards of living, have been unable to do so. As their export earnings have dwindled they’ve kept borrowing anyway (usually pushing the loans into more expensive houses). They became more indebted and, ultimately, came undone in the GFC when creditors suddenly wondered if such hollowing out economies would ever be able repay them.

Similar dynamics have transpired in Australia too. But the decline of value-added production has been dwarfed by the rise in demand for our raw materials, also driven by the rise of developing economies. That has enabled the leveraging of national income to continue as foreign creditors have been comfortable that we remain solvent.

But things are not what they once were. Even for Australia, despite the huge income rise it enjoyed in the past decade, there has been a rationing of the degree of leveraging allowed, driven by de-globalisation, credit ratings agencies with revitalised missions and the corrections of global imbalances.

For Australia, the pre-GFC binge was so enormous that our creditors did question whether we could repay the debt and wouldn’t give us any more unless the government guaranteed it all in 2008. Following this experience, Australian economic managers had a partial awakening. The prudent among them realised that we couldn’t just keep leveraging up our commodity income and expect the world to never stop and ask if it would get repaid. Hence, the Australian Prudential Regulation Authority (APRA) moved to prevent further leveraging of national income by insisting that banks no longer borrow money offshore (which is largely wholesale) and lend it domestically. Instead APRA demanded that for every dollar loaned in Australia, a deposit must been found first.

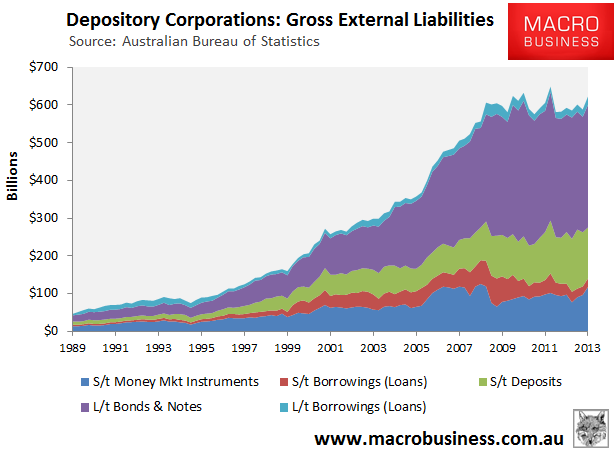

This has forced a profound change to the composition of Australian bank balance sheets. Deposit rates have remained higher relative to the RBA cash rate than in past owing to the competition to attract them, and after the 2010 peak of the GFC stimulus offshore borrowing has not grown in an absolute sense since. To see how stark a change this is, here is a chart from the ABS’s balance of payments data:

Notice the flat line since the GFC and, as well, the creeping uptrend since the current rate cutting cycle began with a spike in the June quarter, driven largely by a rebound in short term borrowings.

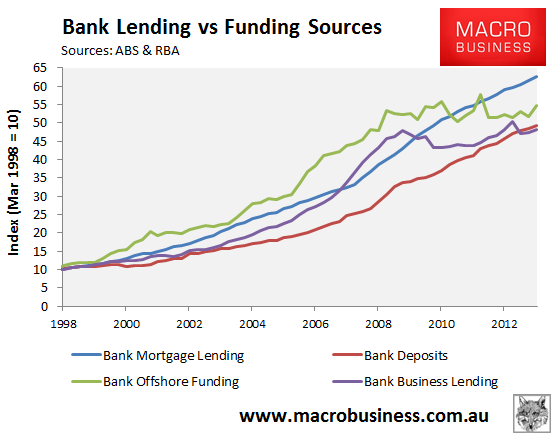

It is too early to tell but my bet is that this is the beginning of a tightening in the availability of locally-sourced liabilities. To underline the point, lets look at some of the other data sources. Late last week the ABS released its little followed National Accounts: Financial Accounts for June. This series measures liabilities a little differently but close enough to compare:

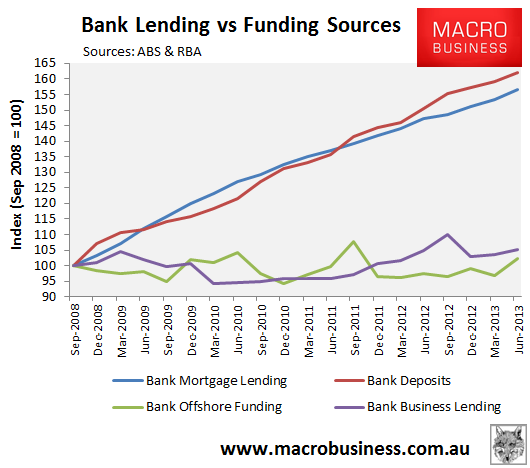

This is an index chart to illustrate growth paths. Notice how the mortgage lending line and bank deposits line diverged significantly post 1998 as banks aggressively used wholesale debt to fund fast mortgage growth. But since 2010, the lines have remained parallel. Here’s a closer look at recent years:

Again, this is an index chart to illustrate growth rates. Notice how mortgage lending and deposits now grow close enough at 1 to 1. Another point to note is how flat business lending has been. This is not coincidental. The great likelihood is that there are not enough deposits to fund strong mortgage and business loan growth. If both fire up then the banks will need to look offshore for wholesale money, just as they did in the past. Either that, or deposit rates will begin to rise, making mortgages less attractive.

Are we there yet? The charts suggest not. But the recent bounce in offshore borrowing has coincided with the rebound in mortgage lending, hinting at a tightening, even if as yet we haven’t seen evidence of that in rising deposit rates.

There is one more data set we can introduce to underline this point. The RBA also tracks the bank’s foreign liabilities. Again, it’s measures are slightly different but close enough to compare:

One advantage of this series is that it is monthly and more timely. And yes, that’s a record high to the end of August.

This should be a line on the sand for regulators. APRA has not given any indication that it is prepared to let banks increase the relative amount of funding they source through offshore markets, let alone the absolute quantities. On the other hand, from time-to-time the RBA has muttered about letting them do so, to its shame.

For those expecting Australia to rebound to strong growth next year driven by a renewed house price and consumption cycle, they are assuming that regulators will let these metrics blow out. They are assuming as well that ratings agencies – which have explicitly warned against it – will let it run without downgrading the banks.

It is possible that both will accede to this outcome. After all, if they don’t, growth will remain straight-jacketed, which will show up in ongoing labour market deterioration. But if they do, Australia will be back on the path to another current account deficit blowout and credit downgrades will be a question only of “when” and not “if”.