What an amazing nation this is. We’re basically in recession, with an historic capex cliff in prospect and steadily rising unemployment, and can you read about it anywhere? Nup! The MSM is determined to boost the stocks of its real estate succubus or its chosen political mates and much of the fringe commentary is either bonkers or inept.

Yet the facts are plain in the nation’s business surveys. The NAB survey has activity consistent with early 2009 levels. The Dunn and Bradstreet survey is the same and is forecasting more to come. The Australian Industry Group manufacturing and construction PMIs are both contracting. The latest, for August, is for services (which constitute 70% of the economy) and it is going from bad to worse:

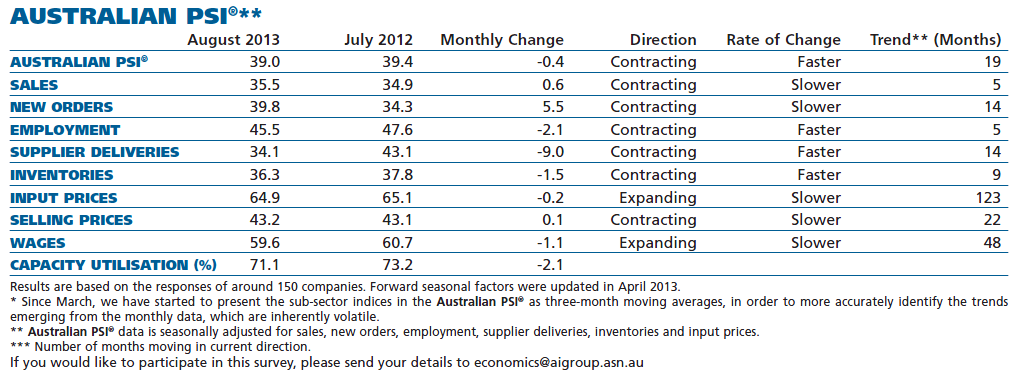

The latest seasonally adjusted Australian Industry Group Australian Performance of Services Index (Australian PSI®) fell 0.4 points to 39.0 in August (readings below 50 points indicate contraction).

The Australian PSI® has declined through 2013 and has now been below the 40 point level for two consecutive months. These are the lowest levels for the Australian PSI® since the GFC-related downturn in 2008-09.

This data points to a further slowing in services sector activity, and therefore in GDP, in the September quarter.

The monthly decline in the Australian PSI® was due to steeper contractions in the employment and delivery sub-indexes, partly offset by a modest rise in the new orders sub-index.

Close to one in five businesses noted that the most important factor affecting activity in August was the “uncertainty” associated with the upcoming federal election.

As a result of a prolonged period of contraction through 2012 and 2013, capacity utilisation recorded its second lowest level since the Australian PSI® series commenced in 2007.

On top of the tough demand conditions facing the sector, the Australian PSI® wages and input prices sub-indexes are both well above the average levels seen over the past three years. This is placing additional pressure on business margins.

The weakness is everywhere:

Advertisement

Sale are stuffed:

New orders were a little better in the second derivative but are still in a deep downtrend:

Advertisement

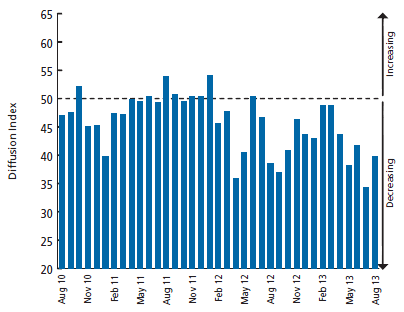

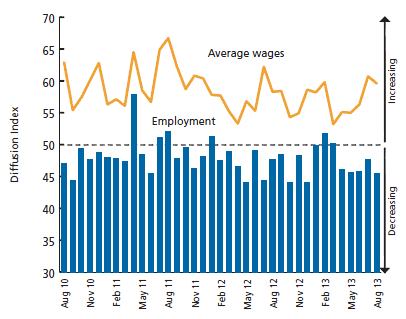

Jobs are contracting consistently:

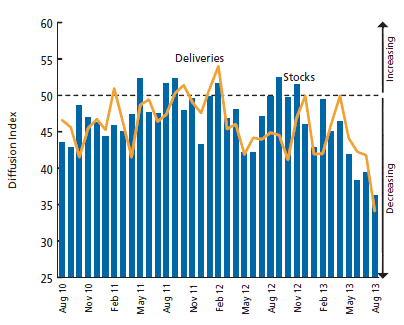

We’re into an inventory rundown cycle absolutely typical of recessions:

Advertisement

And there’s no end in site, though once the inventory cycle turns we’ll see a surge in growth:

The US’s National Bureau of Economic Research (NBER) judges recessions on any number of different metrics, not just the chest thumping two consecutive quarters of falling growth measure. I’d argue we should do the same.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.