Goldman has a note out today examining the where fair value lies for the ASX today:

Higher rates, lower A$ and weak activity; is 14.5x fair?

With the results season wrapping up and the ASX 200 back to its year highs, investors are again focused on valuation. The recent fall in the $A, the sharp rise in long-term interest rates and still weak domestic activity have many investors re-visiting the appropriate multiple.

Traditional valuation models imply 8% upside; caveats exist

Results season completed with EPS down 3% over FY13. Given consensus bottom-up EPS growth of 13.5% in FY14, the ASX 200 is currently trading in line with its 20-year average P/E of 14.5x. Our traditional valuation models suggest 8% upside with a wide range. We are more cautious around valuation given a number of caveats. We expect structurally lower EPS growth, see bonds as more overvalued than equities undervalued, and while yields are supportive, pay-out ratios are at all-time highs.

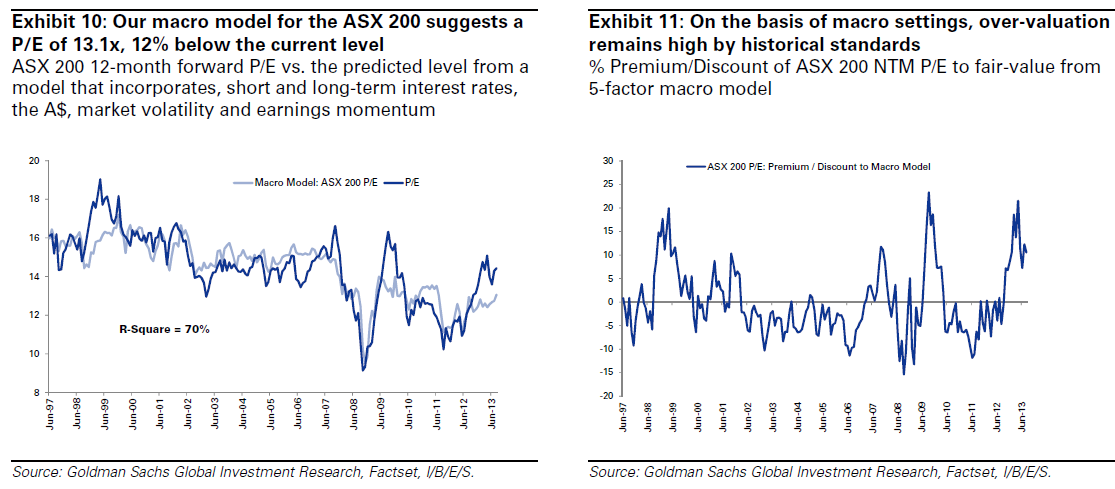

Current macro settings imply a P/E of 13.1x, 12% downside

Given the wide variation in fair-value estimates from our traditional models and our concerns about current fundamentals, we have taken the opportunity to build a more encompassing ‘fair-value’ model. We find that short and long-term interest rates, the A$, market volatility and earnings revision trends are able to explain 70% of the market P/E through time. At present, the model implies a P/E of 13.1x (12% downside) driven by the recent falls in short-term interest rates, a still high A$ and longterm bond rates that remain low by historical standards.

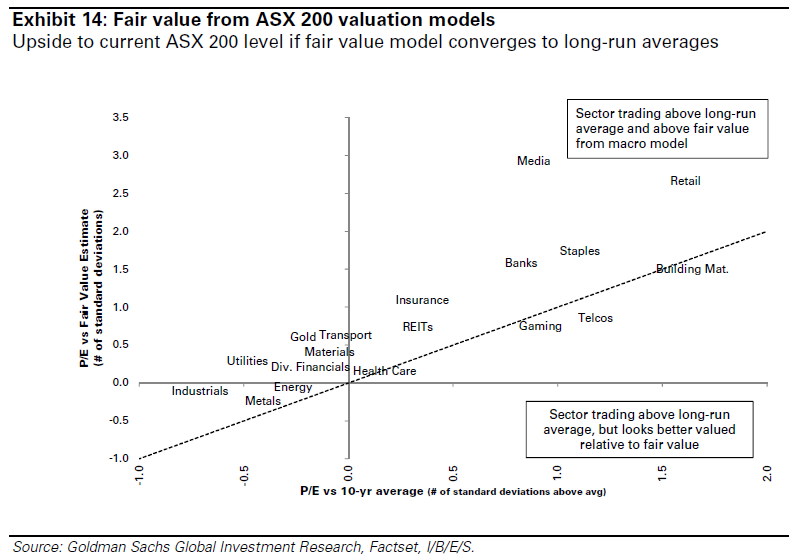

Macro drivers imply Media, Retail & Banks most overvalued

60% of ASX sectors look expensive relative to their 10-year average P/E. This increases to 90% when you consider the current macro backdrop (Energy and Metals the only sectors below fair value). Media, Retail, Banks & Staples screen as most expensive under this framework given macro drivers suggest they should be trading below mid-cycle P/Es. While macro influences can be mitigated by stock-specific factors.

A quick glance at that chart shows you that you’re going to have to pay through the nose to get into local growth stocks. Given the capex cliff, seriously?

I agree the beast is overvalued, especially if rates rise. But given I think that is unlikely, it may be more germane to remember that the one outstanding lesson about financial repressions of the past few years is that asset valuations decouple from traditional metrics. They trade instead on liquidity and hope.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.