A key question for investors right now is how to position the mining/resource sector. The sector has shown signs of life in the last couple of months following a very poor couple of years.

The sector has bounced recently due to improved perceptions toward the Chinese and (to a lesser extent) global growth cycle. However, arguably the dominant performance driver has been the accompanying lift in commodity prices, particularly the key iron ore price (the dominant driver of earnings for the Australian mining sector). Iron ore currently dominates the earnings of the largest three miners (BHP Billiton 50%, Rio Tinto 90%, Fortescue Metals Group 100%) who account for 80% of the Australian mining index (which accounts for 70% of the Resources index).

The majority of forecasters (UBS included) expect the iron ore price to track lower on a 3 and 12 month view, based in particular on expectations of rising supply (and in the short term on slower steel production rates). UBS expects the iron ore price to average US$111 in Q4 2013 and US$102 in Q4 2014 (FOB).

The consensus sits very marginally above these levels.

Can Mining Equities Perform Well If The Iron Ore Price Falls?

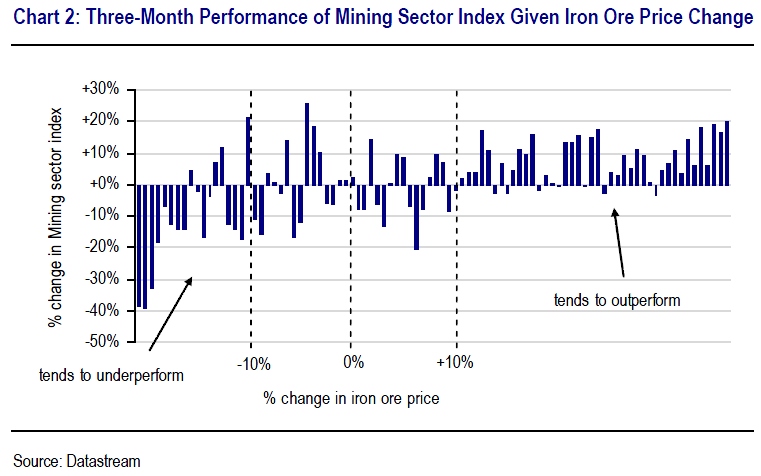

Given this forecast, we examine the historical evidence as to whether there are episodes of a “significant” decline in the iron ore price concurrent with good performance from the mining sector. In essence we are asking the question – if you believe that the iron ore price is set to move lower in coming months, can the mining sector still outperform?

The iron ore market has only a short history of spot pricing (back to 2005) and indeed liquidity is still developing. Nevertheless we observe a strong visual correlation between the iron ore price and the performance of the mining sector (particularly in recent years) (see chart 1).

…Based on this analysis, we found very few instances of the mining sector performing well in the face of a falling iron ore price. The few instances we found occurred in March to May 2009, likely more so reflecting the big recovery rally in equities (see table 1 and chart 2).

This analysis provides solid empirical evidence that significant spot moves matter. Or, in other words, the market has rarely discounted iron ore price moves ahead of time. Certainly not three months ahead of time.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.