Last week was a seminal one for both fiscal and monetary authorities. For the first time since the post-GFC rebound in mining investment we have both levers of macroeconomic policy pushing in the same direction, for growth.

Glenn Stevens will cut interest rates tomorrow. His speech last week swept aside any objections to further rate cuts:

In the third phase of the ‘mining boom’ and post the credit boom, our economic challenges are changing in nature. In the next few years our task will involve supporting, so far as it is in our power, a change in the sources of demand that affect the economy. As resources sector investment declines, other sources of demand need to strengthen, but in a way that is sustainable. The fact that consumption is likely to provide only a modest impetus to any acceleration in domestic demand suggests that other areas will be important. As I noted earlier, at least some of the conditions are in place for stronger trends in dwelling investment and, in time, non-resources business capital expenditure. And exports of resources will continue to pick up strongly.

But successful ‘rotation’ of demand will probably also involve more net foreign demand for other Australian output of various kinds. Given that, the recent decline in the exchange rate seems to make sense from a macroeconomic perspective. It would not be a major surprise if a further decline occurred over time, though of course events elsewhere in the world will also have a bearing on that particular price.

The conduct of monetary policy must, and does, take account of the various features of the environment we face. Calibrations drawn from an earlier part of history can’t be assumed to have the same reliability. Elements of the monetary policy transmission process are probably working somewhat differently than on other occasions. To take one example, the fact that policies in major economies have been at very unusual, or extreme, settings for some time is a complication because of the potential effects on the exchange rate – though, as noted, the exchange rate appears to have been behaving more normally of late.

The fact that the rest of the world has had such low interest rates, that the desire for safe assets has been so strong, that the spreads between the cash rate and the rates that matter most for the economy have widened, and that people have sought to get to a position of lower leverage – all these have been important in explaining why the cash rate has been so low compared with what we had been used to until the mid 2000s. That this has occurred while we have had the peak of the resources investment boom is all the more remarkable.

This has been guided by the flexible inflation targeting framework we have had in place for 20 years now. This framework has prompted appropriate and timely action when needed. It has seen a substantial easing in monetary policy since late 2011. We have been saying recently that the inflation outlook may afford some scope to ease policy further if needed to support demand. The recent inflation data do not appear to have shifted that assessment.

This is a remarkable statement. Although its content is ambiguous about how effective the RBA sees its power to lower the exchange rate, the import of the analysis is that only a lower currency can deliver a ‘sustainable rebalancing’. Truly this is an epic volte-face by the central bank which was, until recently, still encouraging Australians to think of a high exchange rate as a historic boon that was here to stay. It’s not done for the central bank to say it was wrong but it sure is implicit.

As financial markets have rightly interpreted, the statement amounts to a determination to push rates lower.

On the fiscal side, Friday was a stunning day. The Economic Statement was the first Treasury document to seriously contemplate the Chinese adjustment that is underway. It slashed its terms of trade and nominal growth forecasts and thus revenues but importantly didn’t slash spending to offset the revenue declines. As a result, it projected deficits of $12-13 billion for the next two years and actually managed to add modest fiscal stimulus in 2013/14 of $373 million and 1.6 billion in 2014/15.

The net result is that the public sector contribution to growth was rounded up from zero to .75% of GDP in 2013/14 and from 0.5% to 1% of GDP in 2015/16.

The broader economic forecasts remain too aggressive, and further write downs can be expected, but the Budget has moved onto a counter-cyclical footing adding growth rather subtracting from it as the economic outlook deteriorates.

What, then, are the implications? The first question to ask is will the new mix of fiscal and monetary stimulus effect each other? The answer is an unequivocal no. The weakness embedded in Treasury’s new forecasts shows that both levers will need to keep the spigots open as we go over the mining investment cliff and the terms of trade continue to decline.

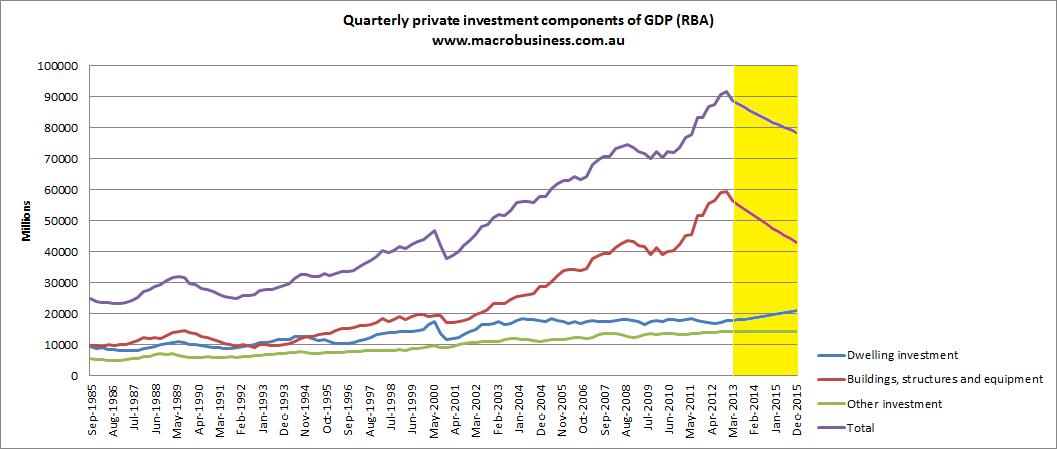

Next, are these changes enough to shift the growth outlook? A little but not enough. As I’ve said many times, predicting GDP is a fool’s errand owing to the limitless variables but the following is intended as a rough guide. At MB we think that the mining investment downdraft will withdraw 1.5-2% of GDP per year for three years. That will return mining investment to a long run average of about 2% of GDP per annum. This is based upon BREE’s current projects underway forecast plus a little more.

In chart form that looks like this:

I’ve averaged the mining investment decline over twelve quarters (it will likely be much more lumpy) and I’ve continued the dwelling investment recovery at an accelerated pace right through the next three years. I expect broader consumer prudence to persist so I do not expect a turnaround in other private investment until the dollar falls much further and then not for a while either. As such, I’ve added a broader slow business investment recovery from the beginning of 2015.

The top line of total private investment is the one to observe. Note how long and steep it is versus 2008 and 1991. Less precipitous but far longer than in 2000. As well, I would argue we have largely exhausted the house price gains that saved the economy in 2000, have fewer options to boost productivity than we did in 1991, and mining is the problem this time not the solution as it was in 2009. We also have less effective interest rates and less capacity to fiscally stimulate.

That’s not to say the recovery won’t come from somewhere. It will. But in the mean time, as you can see, the mining investment cliff represents a pretty awesome headwind for growth.

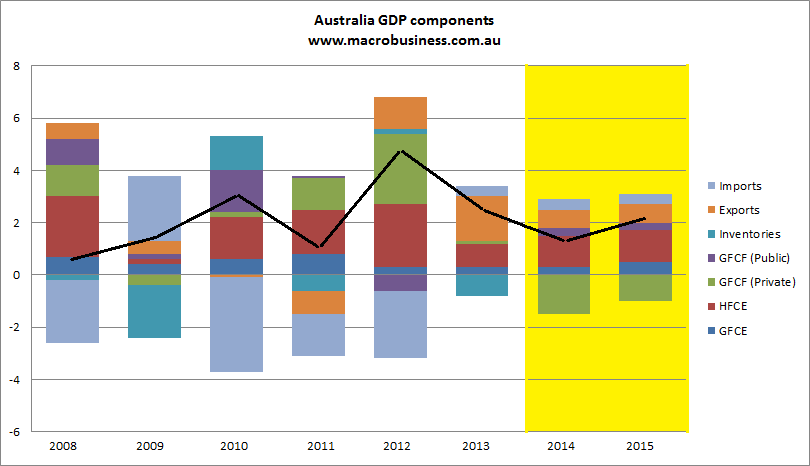

How awesome? Let’s look at it another way. Here are the same speculations charted as percentages of GDP that also includes the offset of growing commodity volumes in net exports:

Note the big subtracting green boxes. That’s private investment with moderate growth in dwelling investment included. It also includes a turnaround in government spending contributing to growth and a modest acceleration in household consumption from this year’s levels. I’ve slowed the contribution from net exports because Chinese demand will flat line this coming year and Indian iron ore volumes will not need to be displaced a second time. The results are GDP growth of 1.4% in 2013/14 and 2.1% in 2014/15.

Please remember, these are not forecasts, they are rough guides. I will be wrong on all fronts. Net exports may be better, consumers may loosen up more, government may get over itself, non-mining investment may recover faster or mining investment hold up better.

The point is it’s an economy operating at stall speed, with rising unemployment and falling business investment. Into this mix we must throw one more probable outcome.

There is a significant risk that the terms of trade will fall further and faster than Treasury forecasts. The iron ore deluge will reach full roar in the first half of next year. Iron ore could very easily spend much of 2014 under $100 and by year end be below $80. Iron ore represents some 25% of the ToT so by itself an $80 price would reduce the ToT by 10%, the same fall Treasury has forecast for the next four years. Coal has further to fall too, in my view, some 10%.

A falling dollar would help but not enough and the income shock would be very large, hitting an already weak economy and threatening recessionary dynamics as mining profits and government receipts tumbled, household demand retrenched and inventories entered liquidation. We’d see fair dinkum stimulus then but monetary policy would be out of bullets.

This is not a scenario that requires China to have an accident. It’s demand need only stall, as China says that it will, and new production pour in. If China actually stumbles in its adjustment then all bets are off.

In short, Australian authorities are right to be manning the pumps. Indeed, if the RBA was not concerned about a house price takeoff I suspect rates would already have a “one” in front of them to get the dollar down to 70 cents and, if our politicians could unshackle themselves from the Howard/Costello legacy, they’d already be in advanced planning for extensive infrastructure expenditure.