Given Tony Abbott has seen sense and will offer bottom line costings for his election budget, I thought I’d have a go at assessing the Libs fiscal outcomes as they currently stand.

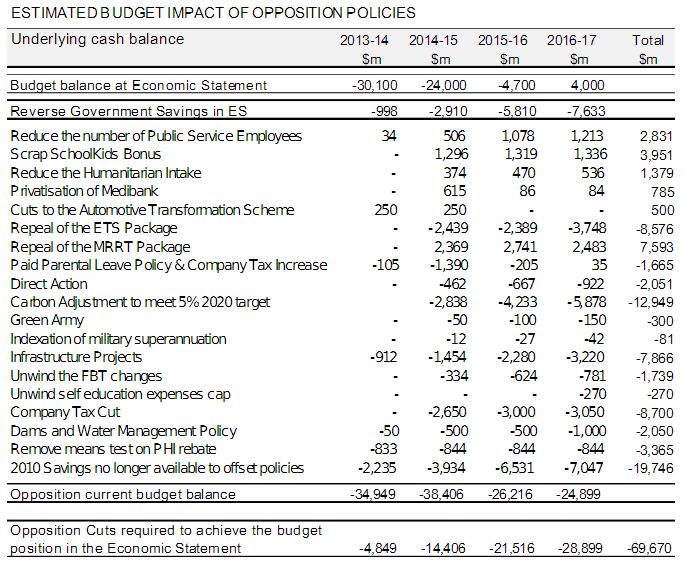

Finance Minister Penny Wong has produced an inventory of the Opposition’s promises and costings (this is an ALP document presumably):

It is the basis to the claim that Mr Abbott currently has a $70 billion black hole that will need to be filled by slashing and burning. Labor has used worst case assumptions it seems:

- the public sector cuts are lower than the PBO estimate

- the real Budget projections for MRRT revenue are lower than those provided. I can only assume that the scrapped mining tax includes gas, which Mr Abbott has committed to keep

- the carbon adjustment is a vague figure so I’ve discounted it based upon assumed ALP bias

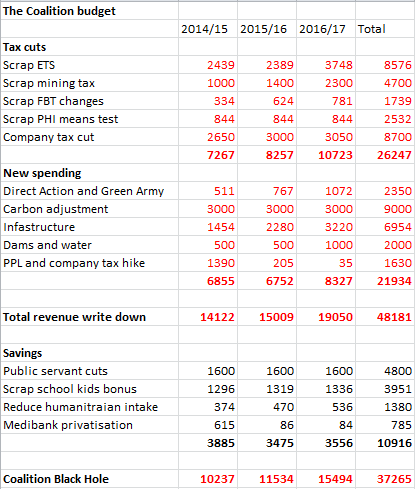

So here are my own estimates with some more balanced assumptions:

A number of points are immediately obvious.

- Tony Abbott is promising almost as much in nominal tax cuts as John Howard did in 2007. $26 billion now versus $34 billion then. Those tax cuts have since been seen as a wild election splash. As we move into the post-miming boom era, what should these be seen as?

- If we remove vague items such as dams and carbon adjustments, the Coalition could plausibly meet a commitment to spend less than Labor without having to make huge further cuts but has little chance of producing a lower deficit than Labor owing to its pledged tax cuts.

- The Coalition has to find a lot or savings if it doesn’t want to blow the budget. If we take out the environment and water policies, it’s still $25 billion in savings needed and that’s before we get to further very likely revenue write downs next year as Treasury forecasts prove optimistic once more.

- Given this last point, this is a budget platform that more resembles a stimulus package.

- In those terms, is it useful? The tax cuts will do little in the short term. If scrapping the carbon price lowers electricity prices then it will be very stimulatory. But I am doubtful. Most of the price rises are unrelated to the carbon price and generators know expensive change is coming anyway so they will keep the fatter margins. I would. The company tax cut is better long term but won’t do much for demand in the short term. The mining tax cut won’t boost mining since they’re not paying it anyway and their problems are more related to commodity prices. On a rough calculation, the FBT change, PHI reform and dams/infrastructure spending are equivalent to about 0.2-0.3% of GDP per annum.

As it currently stands, the Coalition budget is a few good long term supply-side reforms mixed with politically-driven short term cost-of-living and stimulus measures (that will cost more in the long term). It amounts to a recipe for a generously expanding public deficit largely spent upon repeat revenue items instead of the one-off productivity investment that we need to carry us over the mining investment cliff.