CBA is by some distance the most positive of the major banks when it comes to economic research. It is interesting to look at its take on today’s awful capex report:

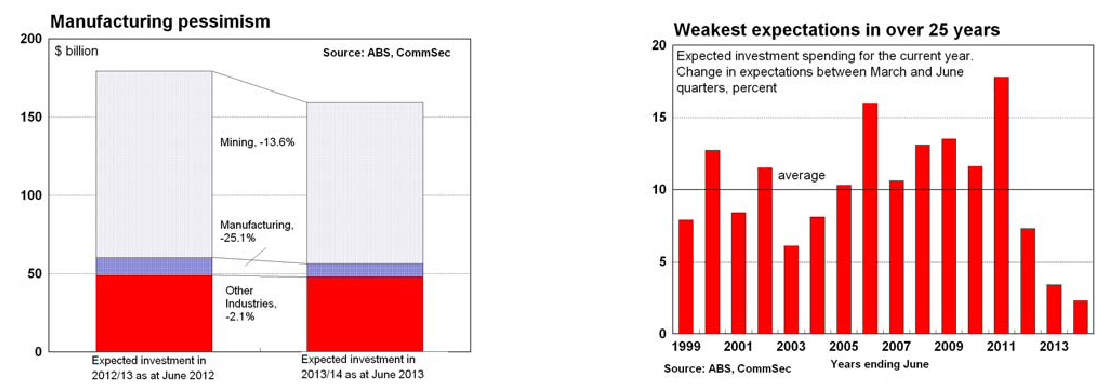

Usually investment plans lift by around 10 per cent at this time of the year. But this time around business investment estimates only lifted by 2.3 per cent, marking the weakest upgrade to investment plans in records going back over 25 years. The resource boom is receding and at the same time more businesses are reassessing medium term spending plans. The tough trading conditions and uncertain global environment have affected business confidence and as such businesses are pushing back investment projects until the outlook improves.

Interestingly when you break down the future investment outlook, the bulk of the pull back in spending was largely across the manufacturing sector (-25.1 per cent), followed by mining (-13.6 per cent) and “other industries” – where investment is expected to fall by just 2.1 per cent. What clearly can be seen is that the Reserve Bank has some work on its hands to disentangle the various parts of the economy. The mining states are pulling back from heady levels of investment but non-mining states and industries aren’t filling the void.

Manufacturing investment contracted for the seventh consecutive quarter. On a positive note the fall in the currency should alleviate some of the pressures on export orientated sectors like manufacturing. While the recent rate cuts and likelihood of another interest cut should ensure that sectors such as residential housing start to gain some traction.

Lower interest rates, strong population growth, healthy employment, and pent up housing demand is starting to see the housing sector shake of the shackles and begin a much needed resurgence.

Activity in the mining sector will remain firm for some time yet despite the recent pull back. No doubt the slowdown in China and lower commodity prices have weighed on investment decisions. But outside of the mining sector, businesses remain cautious and refuse to invest.

The Reserve Bank may have more to do in cutting rates if future investment plans continue to be pared back. However the key is what takes place after the election. If confidence improves, consumers start spending again then businesses may get their mojos back and the Reserve Bank will be able to remain on the interest rate sidelines. Certainly businesses are cashed up and it is likely that commercial vacancy rates will fall in coming years due to the lack of building.

With the cash rate likely to remain at 2.5 per cent or even lower, and with returns on investment properties current running at a 9.7 per cent annual rate, more budding investors are likely to be enticed to shift funds from cash into residential property.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.