From Goldman Sachs today comes a good summary of the earnings season to date:

It is still early days with only 20% (36% by index weight) of companies under our coverage which are expected to report during August having reported. Early trends show fewer headline surprises, but encouragingly an increase in the number of companies providing guidance and surprising on dividends. Despite this our analysts remain more cautious having downgraded earnings for close to half the companies that have reported.

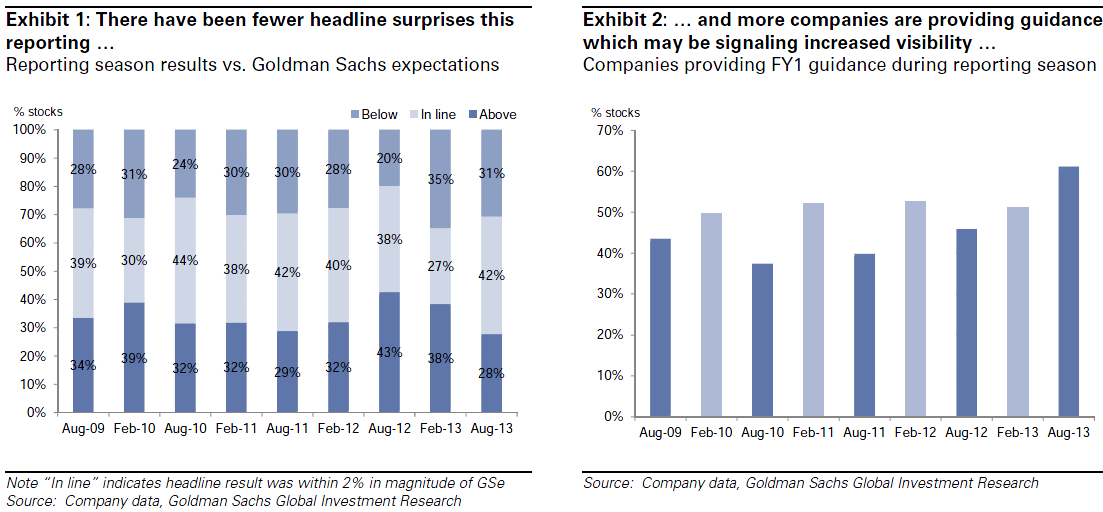

Fewer headline surprises: There have been fewer headline surprises this reporting season relative to recent years. So far, 42% of company results have been in line with our expectations (i.e. less than 2% variation analysts’ estimates), which is higher than the 37% average since August 2009 (Exhibit 2). We attribute this to the higher than normal number of companies that provided trading updates in the lead up to reporting season – 25% of companies that have reported to date provided a trading update in the last 3 months, effectively pre-announcing their result.

More company guidance: Encouragingly, there has been a notable increase in the number of companies providing FY1 guidance. 61% of companies that have reported to date have provided FY1 guidance (Exhibit 3), materially above the historical August average of 42%. This is particularly interesting in light of the recent weak business confidence surveys, raising the question whether cost-out and restructuring initiatives undertaken over the last few years, coupled with the weaker AUD and easing in monetary policy is seeing some growing optimism, or at least degree of confidence, from management around the risks in managing their businesses to a budgeted outcome.

Companies that have provided FY1 guidance this year but did not last year include: BKN, SGP and BWP.

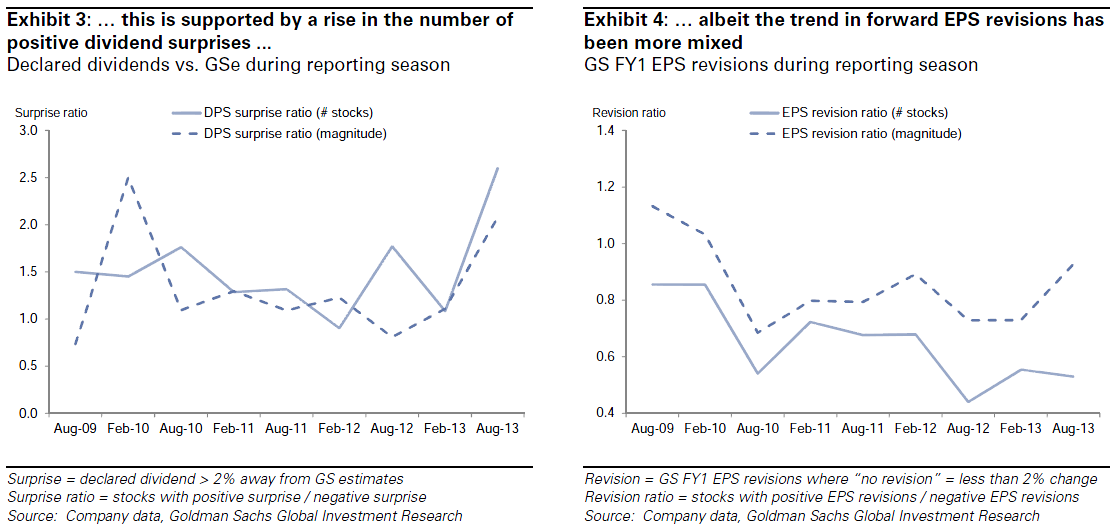

Positive dividend surprise: To date companies have reported 2.6x as many positive dividend surprises versus negative dividend surprises (Exhibit 4) – the highest this ratio has been since we have recorded the data (Aug 2009). It appears that companies are continuing to embrace the chorus of investors demand for yield, but importantly it also tells something about the general shape of corporate balance sheets and strength in underlying cash flow. We have long held the view dividends are the truth serum for gauging management’s confidence in the sustainability of earnings and cash flow growth.

Typically a rise in the number of companies providing guidance and raising dividends is a positive signal – it will be interesting to see whether these trends hold as we progress through reporting season.

Forward EPS revisions have been less encouraging: Interestingly, these positive trends have not been reflected in our analysts’ forward earnings revisions. Close to half the number of stocks have seen EPS downgrades (negative EPS revisions greater than 2%) which is more than twice the number that have seen upgrades. This is not dissimilar to what we saw last August.

Stocks that have reported a strong headline result and seen GS EPS upgrades are: TCL, RMD, HGG, TLS, CBA, JHX.

Stocks that have reported a weak headline result and seen GS EPS downgrades are: NVT, FOX, NCM, DMP, RKN, CSL, GFF.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.