Ben Bernanke appeared last night on Capital Hill and reassured folks of two things. The first, was to distinguish between tapering and low interest rates:

“… we are providing additional policy accommodation through two distinct yet complementary policy tools. The first tool is expanding the Federal Reserve’s portfolio of longer-term Treasury securities and agency mortgage-backed securities (MBS) … The second tool is “forward guidance” about the Committee’s plans for setting the federal funds rate target over the medium term … Within our overall policy framework, we think of these two tools as having somewhat different roles. We are using asset purchases and the resulting expansion of the Federal Reserve’s balance sheet primarily to increase the near-term momentum of the economy … We are relying on near-zero short-term interest rates, together with our forward guidance that rates will continue to be exceptionally low–our second tool–to help maintain a high degree of monetary accommodation for an extended period after asset purchases end, even as the economic recovery strengthens and unemployment

The second, was to underline that tapering is data dependent:

I emphasize that, because our asset purchases depend on economic and financial developments, they are by no means on a preset course. On the one hand, if economic conditions were to improve faster than expected, and inflation appeared to be rising decisively back toward our objective, the pace of asset purchases could be reduced somewhat more quickly. On the other hand, if the outlook for employment were to become relatively less favorable, if inflation did not appear to be moving back toward 2 percent, or if financial conditions–which have tightened recently–were judged to be insufficiently accommodative to allow us to attain our mandated objectives, the current pace of purchases could be maintained for longer. Indeed, if needed, the Committee would be prepared to employ all of its tools, including an increase the pace of purchases for a time, to promote a return to maximum employment in a context of price stability.

Advertisement

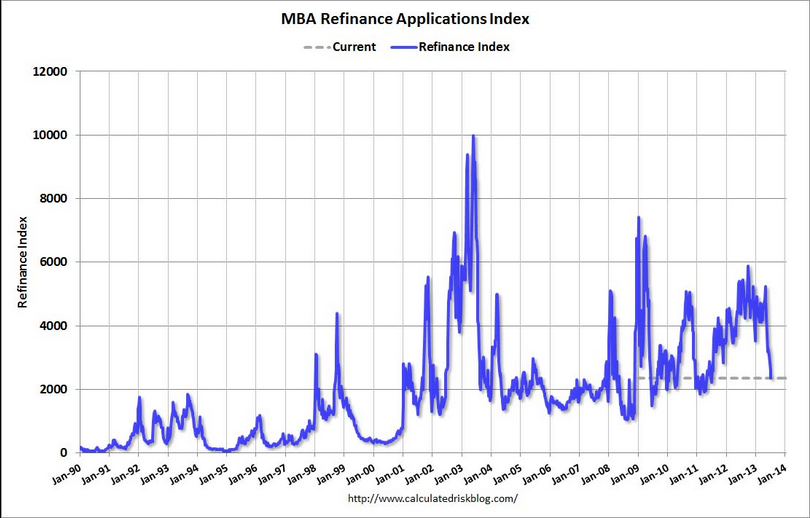

So we need to look at the data then. And more signs of slowing in housing has me still quite doubtful about Septaper. Last night we saw the weekly Mortgage Bankers Association report and the news was more softness:

The Refinance Index decreased 4 percent from the previous week and is at its lowest level since July 2011. The seasonally adjusted Purchase Index increased 1 percent from one week earlier…The refinance share of mortgage activity decreased to 63 percent of total applications from 64 percent the previous week and is at its lowest level since April 2011…The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) was unchanged at 4.68 percent, with points decreasing to 0.42 from 0.46 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

And the chart from Calculated Risk:

Advertisement

Refinancing is back in the GFC bust range with further to fall. New loans were up a bit but look toppy too. As I’ve said before, there is a strange but compelling correlation between US refis and house prices. Worse, mortgage rates haven’t come down this week and if Bernanke tapers you can expect probably another 50bps immediately on top of the equivalent five rate hikes already delivered by the bond market in eight weeks.

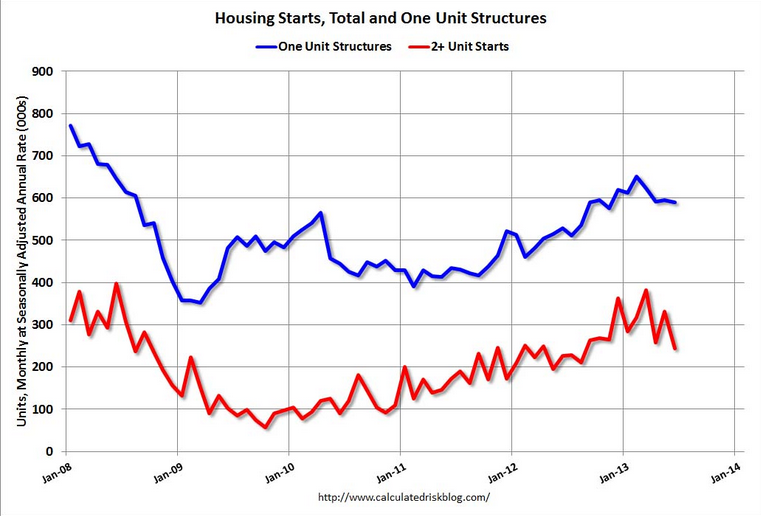

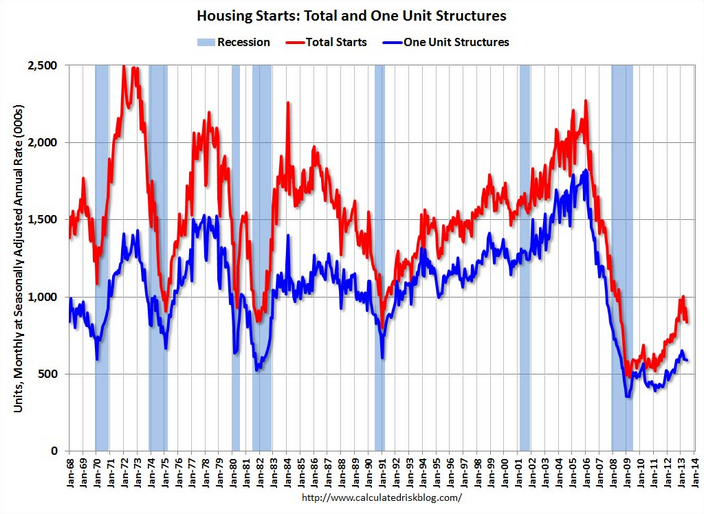

Is it a big surprise that new dwellings are also rolling over and missed an overly bullish consensus last night? Also from Calculated Risk:

Housing Starts:Privately-owned housing starts in June were at a seasonally adjusted annual rate of 836,000. This is 9.9 percent below the revised May estimate of 928,000, but is 10.4 percent above the June 2012 rate of 757,000.Single-family housing starts in June were at a rate of 591,000; this is 0.8 percent below the revised May figure of 596,000. The June rate for units in buildings with five units or more was 236,000.

Building Permits:Privately-owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 911,000. This is 7.5 percent below the revised May rate of 985,000, but is 16.1 percent above the June 2012 estimate of 785,000.Single-family authorizations in June were at a rate of 624,000; this is 0.6 percent above the revised May figure of 620,000. Authorizations of units in buildings with five units or more were at a rate of 261,000 in June.

Advertisement

If the Fed gets to its Septaper I’ll be surprised. And if it does it anyway, I’d be worried about the impact on stocks as growth fades with housing, which does seem to be partly the point

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.