The June NAB survey is out and suggests that right now the Australian economy is flirting with recession as conditions plunge to the worst level since May 2009:

Business conditions and capacity utilisation slump to a four year low. Confidence a little better but still below trend. Conditions very bad in retail, mining and manufacturing, despite low interest rates and falling AUD, though signs a little better for exports. Plenty of spare capacity with little indication of being utilised in the near term; forward orders and employment still very poor.

- The June survey paints a worrying picture of the Australian economy; business conditions slumped in June to their lowest level since May 2009. Weaker trading conditions and profitability combined with still poor employment conditions drove business conditions lower, with each of these indicators remaining well below average levels. Conditions deteriorated heavily in mining, retail and manufacturing (despite a tumbling AUD). Weak forward indicators – including forward orders, stocks, capacity utilisation and employment conditions – remain concerning and suggest little improvement in near-term demand.

- Business confidence lifted marginally in June, but remained lacklustre. The falling AUD appears to have done little to lift spirits, with concerns about global economic conditions likely to be weighing. Overall weakness in domestic economy also likely to be worrying firms. Federal government reshuffle occurred during the final days of survey period, but the survey provides little indication about how sentiment may have been affected.

- Overall, the survey implies underlying demand growth and GDP (6-monthly annualised) of around 2½% in the June quarter. Our wholesale leading indicator suggests a modest improvement in near-term activity, at best.

- Labour costs growth softened in June, consistent with still weak employment conditions. Prices fell for a second consecutive month (but retail rose), while costs grew modestly.

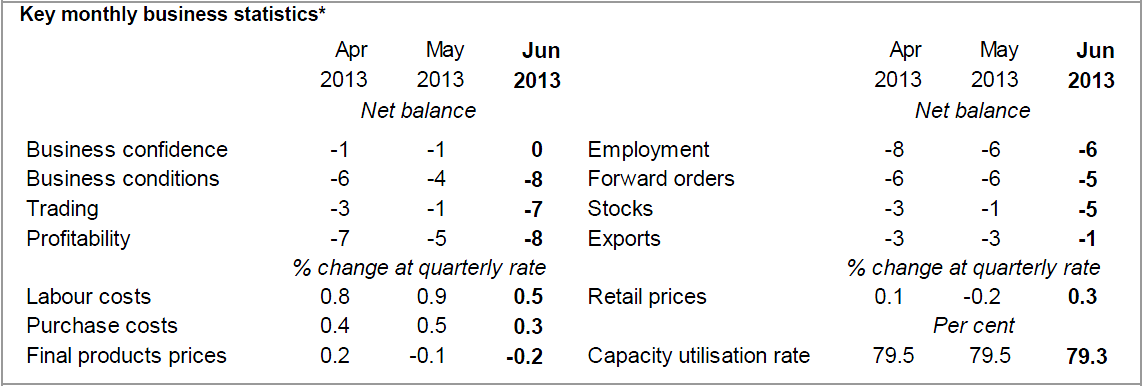

Here are the headline numbers:

The two main movers were current conditions and labour costs, both of which tanked. Everything remains weak.

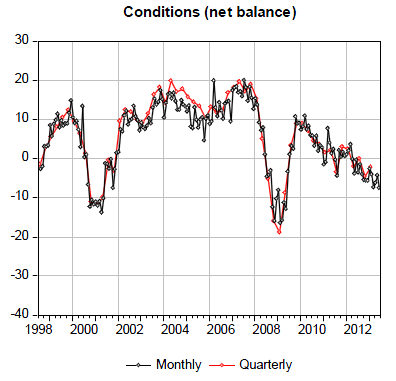

Current conditions are deteriorating:

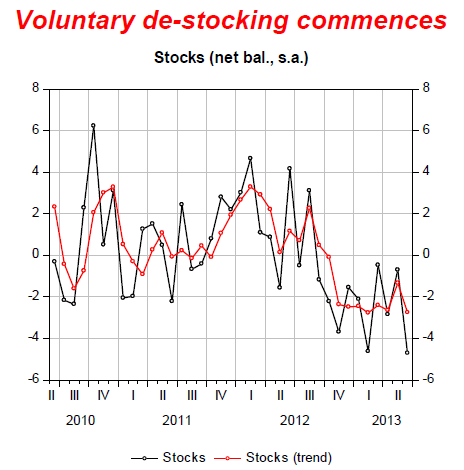

And there is evidence that weak demand is generating recessionary business cycle dynamics with inventories tumbling:

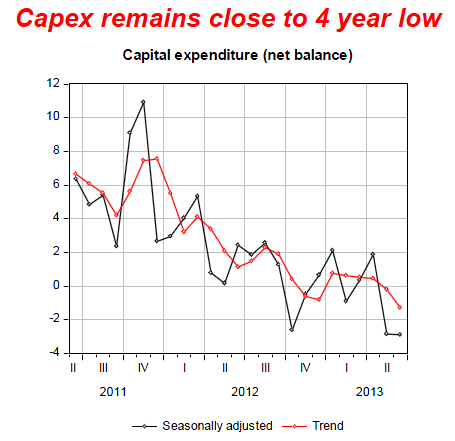

Thankfully capex held up, but is in the basement:

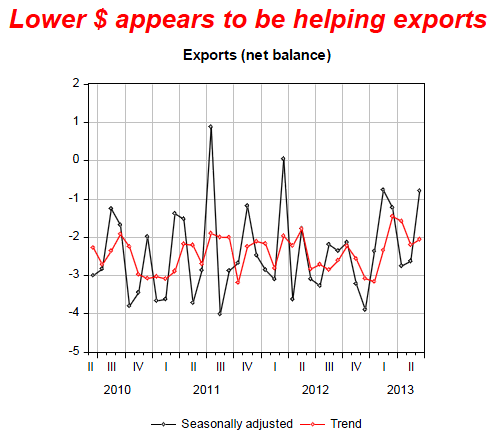

And there is a small upside in better export orders:

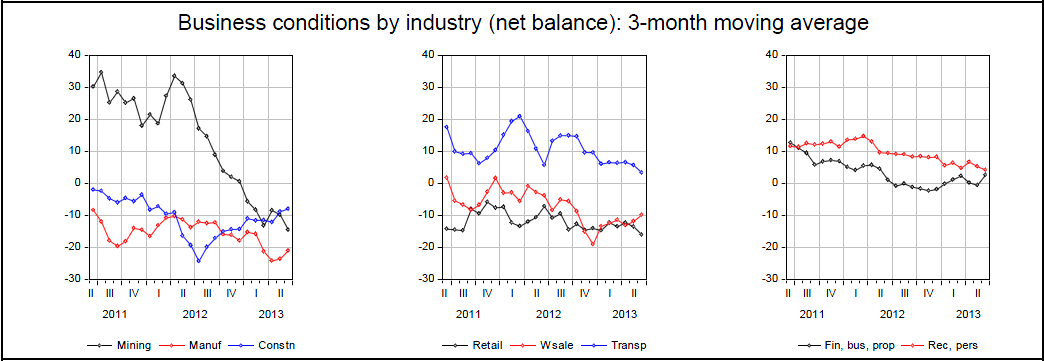

But weakness is widespread across industries:

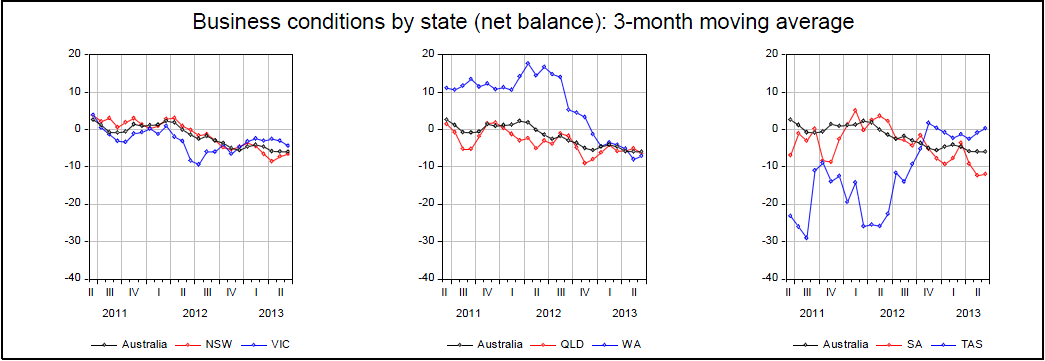

And states:

This report has rate cut written all over it, which is what NAB concluded, in spades:

Domestic weakness implied by this survey, along with softness in China, a weaker terms of trade and financial market volatility, encourages us to bring our next expected rate cut forward to August (previously November), assuming no downside surprises from unemployment or inflation. We expect the bias to easing to continue beyond August. Our inflation forecasts are unchanged at 2.4% in mid-2013 and 2.5% in mid-2014, well within the RBA target band. We have left GDP growth unchanged at 2.3% in 2013 and 2.8% in 2014 but with greater downside risk to the outlook. The unemployment rate is still expected to exceed 6% by the end of this year.

2013m06 Press release.pdf by James Woods