From UBS today comes a gloomy assessment of the forthcoming earnings season:

Weakening A$ Keeping Earnings Respectable

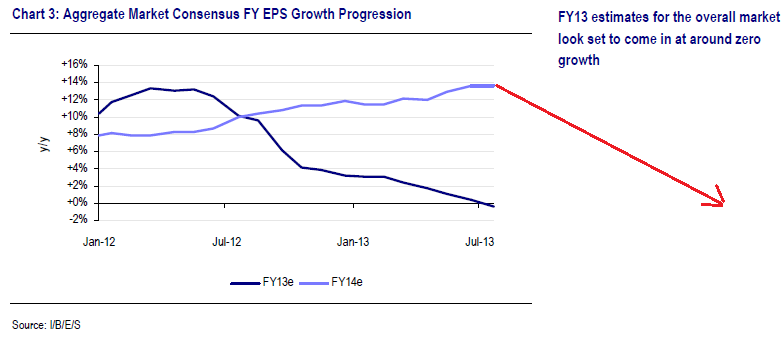

FY13 consensus earnings growth for the aggregate Australian market currently stands at 0% (+5% excluding resources) compared to +3% (+6.5% excluding resources) expected six months ago. While stock-specific profit warnings have picked up, a long tail of passive A$-related upgrades for foreign earners have kept aggregate earnings estimates from deteriorating significantly further.Don’t Count On Another Reporting-Season-Rally From Cyclical/Value

Last reporting season saw a reasonable number of rallies of ‘value’ stocks on better-than-feared results. While investor expectations going into this results season are certainly subdued, the weakening macro backdrop since last reporting season is unlikely to provide as fertile a backdrop for value and cyclical stocks. Our analyst expectations for individual stock upside and downside surprise candidates are skewed to the downside by a ratio of 3 to 1 (see table 2).A$ The Main Support For FY14 At This Stage

Expected FY14 consensus earnings growth for the market excluding resources of +8.8% seems a stretch, in our view particularly given FY13 earnings growth of +5%. We stick with our top-down forecast of 6% given an expectation of further softness in the A$ and an improving corporate efficiency focus. We are not factoring much in the way of economic improvement or deterioration. Top-line growth remains anaemic, with FY13E revenue per share growth of less than 2%.

Very good. But not quite right. The only support will be from the Australian dollar but it won’t help miners. I expect commodity prices to fall further than the dollar (and if they don’t fall the dollar won’t either). Of course there are productivity and volume stories for support but they won’t be enough to offset bulk commodity price falls.

The better play remains selected non-mining dollar exposed stocks.

On value and cyclical stocks, I think UBS is right that both have had their run. The on-again, off-again Fed taper will keep PE’s under pressure as well as the local economy forgetting we’re in a rate cut cycle.

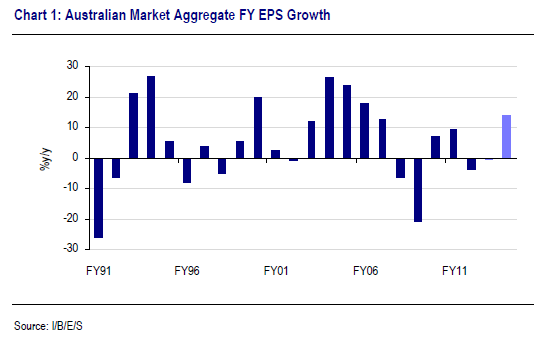

Here’s a few charts on earnings forecasts. First, two years at zero (but next we’ll be back!):

And here’s the progression of how the market came to terms with no growth with my own added line (red) for my forecast of where we’ll be this time next year if a few things go right: