An interesting recent note from Macquarie this morning:

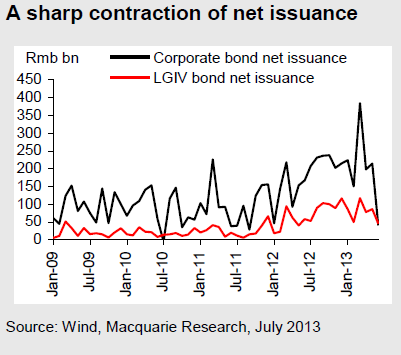

As a consequence of the recent interbank liquidity squeeze, corporate bond issuance fell significantly in June – total net issuance shrank dramatically to Rmb41bn from Rmb214bn (top chart).

- The contraction was particularly prominent for Short-Term Commercial Papers (regulated by the PBC), as the liquidity squeeze had a relatively bigger impact on short-term rates than long-term ones: the outstanding amount of STCPs decreased by Rmb71bn, compared with an increase of Rmb59bn in May.

- So the liquidity squeeze has already had an impact on large companies. It’s thus unsurprising that the 3-month outlook of credit availability, a result of the MNI survey, which covers close to 200 listed companies, fell in June to the lowest level since April 2012.

- In the meantime, the situation also worsened for smaller firms – the discount rate of bank acceptance bills (a major finance tool for SMEs) has gone up significantly in June (bottom chart on the left).

- The LGIVs, though, fared relatively better. The net issuance of LGIV bonds fell less sharply to Rmb45bn from Rmb86bn, and their average issuance yield went up by only 35bps in June to 5.71%.

- Liquidity has an asymmetric impact on the economy. As Milton Friedman put it, monetary easing is like pushing a string, while tightening is like pulling a rope, and is hence much more impactful. Given the existing weaknesses of thevcurrent economy, we’d expect the negative impacts of tighter liquidity to be felt soon.

New yuan loans and total social financing for June is out in the next day or so and will be an important release.