JPMorgan’s Paul Brunker has a little note today that makes plenty of sense to me:

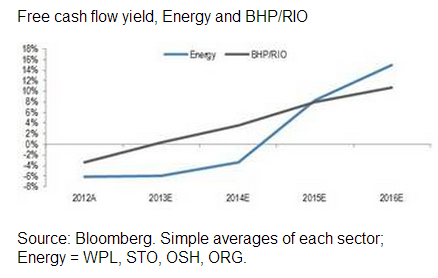

Investors in the Australian market are starting to apply two angles on Resources stocks that are relatively unusual. First, the sector is seen as a way to play a weaker AUD; historically this has not made sense given the correlation between the Aussie and commodities prices, but the relationship shifts if the AUD is falling on a weak domestic economy and RBA easing. Secondly, as we work through the capex cycle there is an argument for looking at the free cash generation of the companies, at least the larger, lower-cost ones. In our view these themes are better played through Energy than Mining. The FCF hockey-stick is sharper, given how big LNG projects are relative to the size of the companies; and the underlying commodity is less volatile than industrial metals and less dependent on the Chinese investment story, which looks challenged in the near term.

There are several more advantages to energy over mining. I’m of the view that a major bust in Pilbara miners is a high risk. As the iron ore price marches down the cost curve on the coming supply deluge and the structural adjustment in China, it may stay lower for longer than most expect – much like coking and thermal coal are now – forcing a lot of consolidation. As this process transpires I’d expect equity values to remain pressured.

Eventually the big low cost producers will buy up their bankrupted small competitors and consolidation will stabilise the price, somewhere around $80 in long term in my view.

Advertisement

Gas on the other hand is exposed to better demand dynamics in Japan (and is not very exposed to China) and is still largely based on oil-linked price contracts. Although they may come under pressure for renegotiation as US supply ramps up, most look solid enough. Moreover the oil price is not likely to fall except in the event of a global growth problem which I do not foresee.

Both have a mix of costs in US and Australian dollar costs and if I had to guess I’d say the US dollar costs in energy are higher than the mining sector owing to the high import component of plants and equipment but that’s a disadvantage I’d overlook at the macro level. It needs to be examined at the company level.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.