Westpac released its July Red Book late Friday and the news is good for Australia with consumer attitudes swinging decisively away from the temptations of low interest rates:

The sub-index tracking views on ‘time to buy a major household item’ declined marginally (–1.7%) in Jul but remained at an elevated level.

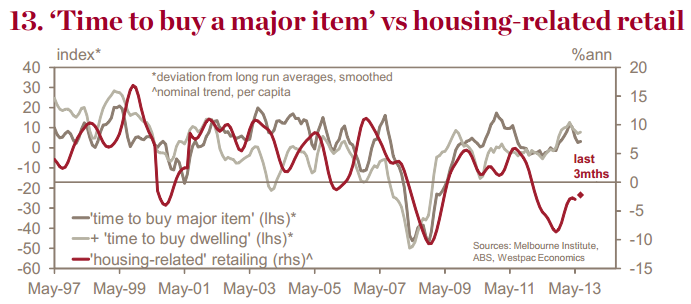

Despite these positive reads, actual spending on durables appears to be weakening again. After a strong burst in Q1, nominal sales have declined 2.1%, –0.2% and –0.3% over the last 3mths. Some of this may be partly due to price falls. However, the detail points to weakness outside the disinflationary ‘electrical & electronic goods’ segment. Indeed, ‘housing-related’ retail sales – furniture, floor coverings, housewares etc – have led the weakening and continue to undershoot sentiment-based indicators.

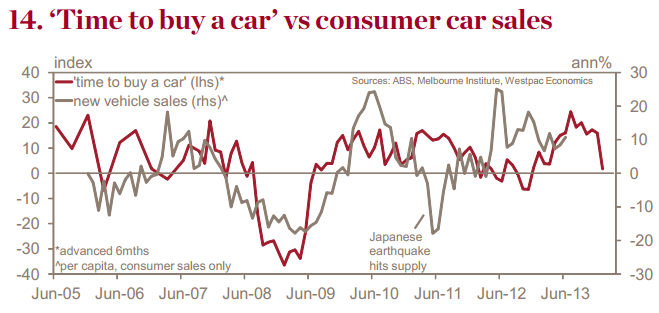

The sub-index tracking views on ‘time to buy a vehicle’ fell heavily in Jul, with the 10% drop the biggest monthly fall since early 2008. Although the index remains a touch above average, the 2008 decline came from a similarly high starting point and resulted in a slump that saw consumer vehicle sales drop 10% by the end of the year and a further 9% over the following 6mths.

There are no indications yet of a sales decline – monthly sales look instead to be up a tidy 4.4% in Jun. However, shifts in time to buy can take up to 6mths to fl ow through to sales. If weak reads continue that suggests car sales may soften more markedly towards year-end.

This is really excellent news. It’s difficult to pinpoint precisely why the consumer has pulled in attitudes in July but the general thrust I’m sure is obvious. It’s some combination of a falling dollar, stock market correction and a spreading consciousness that we’ll need to adjust as China slows. It enables the RBA to cut interest rates again in August to continue to pressure the currency, which should be the main source of the recovery.

Rebounding consumer prudence is born out as well by big falls in the “time to buy houses” index:

Advertisement

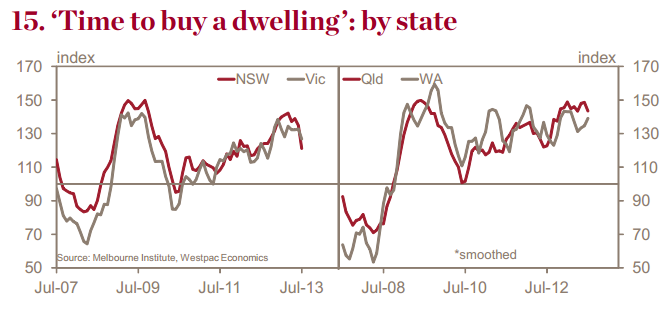

Consumer optimism on ‘time to buy a dwelling’ was shaken in Jul with the index falling 8.4% to 131.3. Although this still leaves the index a comfortable 8pts above its long run average, and a similar pull-back proved to be short-lived in Apr, there are several reasons to be wary of the Jul fall.

The Apr fall appeared to stem from brief speculation at the time that the next move in interest rates could be up rather than down, perhaps as soon as the end of this year. In retrospect that was clearly nonsense but it was enough to rattle some segments – those in key first home buyer groups in particular.

In contrast, the Jul fall comes against a more benign interest rate backdrop with the RBA carrying a clear easing bias and few countenancing the possibility of higher rates. By state, the Jul decline was heaviest in Vic (–13.8%) and NSW (–10.1%). This was the case in Apr suggesting affordability may again be the cause but price rather than interest rate related.

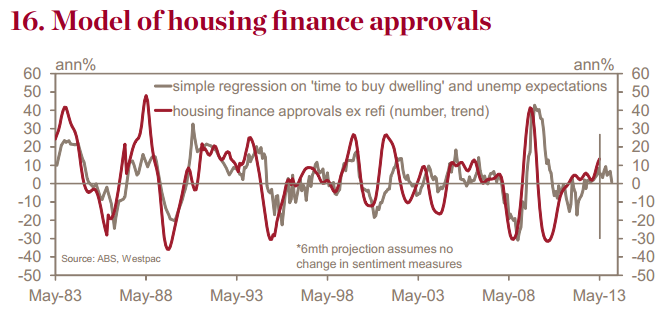

Our sentiment-based model of housing finance approvals shows why the July fall in the ‘time to buy a dwelling’ index is important. With the other driver of the model, unemployment expectations, already weak, the Jul fall could see the finance upturn stall flat, if sustained.

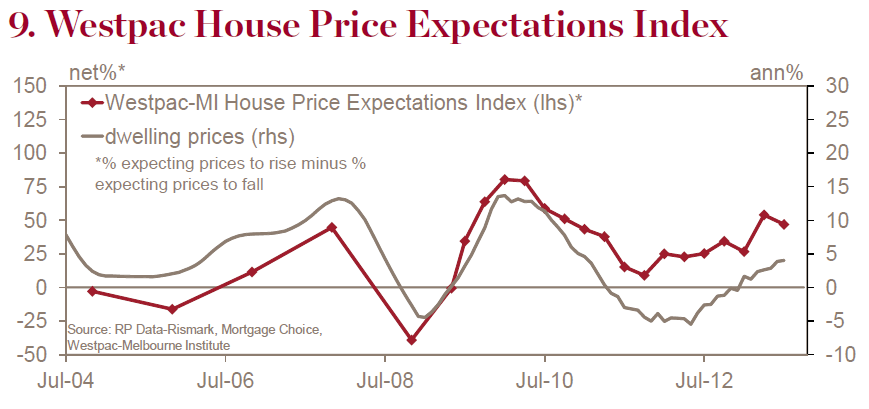

More good news. As house prices have firmed a little in the eastern states and general conditions have declined a bit (see above) the consumer already appears ready to pull back on the cycle. Reinforcing these findings, there were solid falls in house price expectations:

The Westpac-Melbourne Institute Consumer House Price Expectations Index moved lower in Jul from 53.9 in Apr to 46.9. That marks a softening in the upbeat expectation for prices although most Australians still expect house prices to move higher over the next 12mths.

At 58.6%, the proportion of respondents expecting prices to rise remained an outright majority, down marginally on Apr’s 62% . A further 30% expect house prices to remain stable with 12% expecting prices to decline, up from 8% in the April survey. The up:same:down mix is significantly more positive than the 47:32:21 reading averaged in 2012.

Although there is a clear consensus that prices will rise, few expect double-digit price growth with just 8% expecting a 10%+ rise. Dwelling prices often surprise though. Prices rose 3.9% in the year to Jun – a gain over half of consumers did not anticipate. Conversely prices were weaker than expected in 2011-12 with only 22% of consumers correctly picking the 2.6% decline.

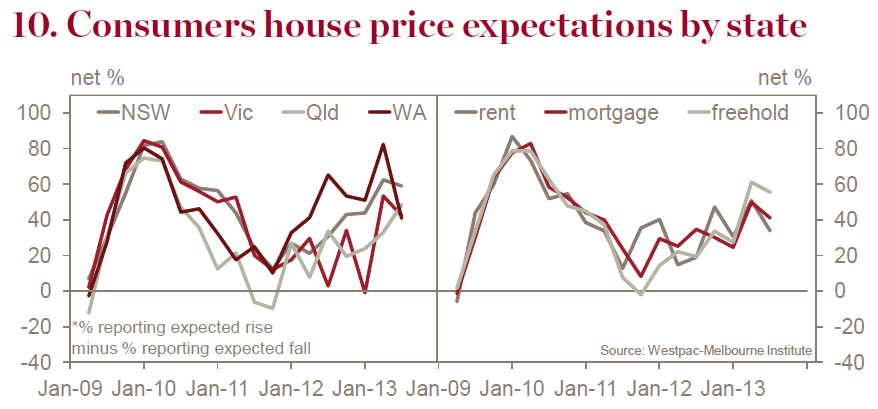

The state split showed some notable shifts. Expectations took a big knock in WA, falling from a very bullish +82 in Apr to a much lower but still positive +41 in Jul. This looks to be morethan just a mining story with expectations in Qld tracking in the opposite direction (+15pts).

Advertisement

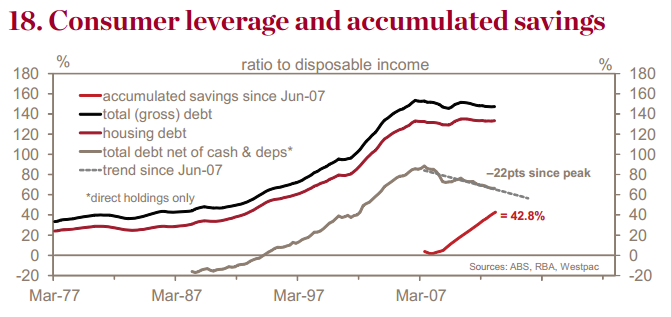

And in conclusion, the upside of resurgent prudence in the consumer is made plain by a fascinating chart provided earlier in the document:

Indeed, the rise in cash and deposit holdings may account for one of the ‘puzzles’ of post GFC Australia: consumer deleveraging that is apparent everywhere except in the figures on leverage. The household debt to income ratio is only 6pts below its pre-GFC peak. Net of these holdings though, the reduction is 22pts.

In short, despite all of the insults thrown at consumers over the past few years for lacking in confidence, they are very confidently deleveraging via increased savings without killing our banks, they’ve helped fund the mining boom, and reduced Australia’s current account deficit to manageable levels.

Advertisement

This is going to get more difficult to do as national income growth stalls (and reverses) through the end of the mining boom but the sensible levels of prudence indicated across this document make me confident that the saving will continue, asset prices will continue their slow melt and that the heavy lifting for out post-mining boom recovery will be done by big falls ahead in interest rates and the currency. I suspect as well that consumer prudence will force our politicians to abandon their dream of surplus and get on with a moderate debt-funded nation-building program post-election.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.