We looked earlier on Thursday at whether the PBoC and other Chinese authorities have engineered the recent squeeze in China’s interbank markets (answer: yes) and why they might be choosing this moment to do so (answer: somewhat more complicated).

Chinese interbank rates according to Shibor are incredibly high — and yet, apart from the report of a special ‘targeted liquidity operation’ for the benefit of one, unnamed bank, the central bank appears to be resisting pleas to ease up on liquidity provision.

So, what gives?

Firstly, some background: the PBoC has been talking about risk since December, when it appeared to add ‘controlling risks’ to its short list of policy objectives. Yet by then, the big Chinese banks had already reined in their lending and much credit growth was coming from the country’s growing shadow banking sector. Around the same time the PBoC along with other key financial authorities, including the Ministry of Finance and the banking regulator, also indicated unease with local government financing vehicles, some of which appeared to be tapping non-bank investment products to cover souring debt.

But it was still unclear this was an attempt to rein in the shadow banking sector and credit more broadly, or just to monitor and control it more carefully.

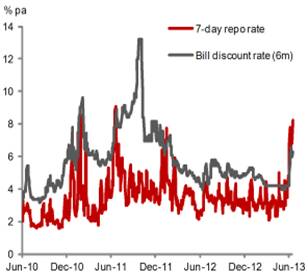

The recent liquidity tightening however is on another level. The seven-day repo rate tripled in two weeks, overnight rates soared more than a third in one day, and intra-day rates were as high as 30 per cent.

These numbers sound terrifying, but Nomura’s Zhiwei Zhang points out that the bill discount rate — a proxy for short-term bank lending to private companies — has risen at a similar pace to the repo rate. In contrast, PBoC tightening in 2011 resulted in a big spike in the bill discount rate. So this tightening seems perhaps more precise, and its effects more deliberate.

And yet this chart also highlights just how steep the increase in interbank rates has been.

Again: what’s going on?

The following, from Hexun News via Chinascope Financial, might be illuminating. It describes an executive meeting of the State Council last night chaired by premier Li Kequiang:

+ The Chinese leaders stressed that financial industry plays a key role in China’s stable economic growth, economic restructuring, and social benefits. In order to overcome the difficulties seen in the Chinese economy, the regulators called for fiscal and monetary policy consistency and gradual financial system reform which aims at efficiently allocating credit in the industries with promising growth outlook.

+ The Chinese regulators highlighted at the meeting that new credit granted to small companies, farmers, rural areas, and agriculture industry must maintain at the level in year-ago period; in addition, private capital is encouraged to participate in the reorganization of financial institutions, and the regulators will give green lights to the establishment of privately-owned banks and finance leasing companies.

Fascinating, right? Because it all suggests this is a very deliberate move to direct China’s credit into more effective investments — things that will actually make some kind of return, rather than requiring debt rollovers and the like.

Yet there might be even more to it. Are the PBoC’s efforts part of a broader political shift?

Bankers had been calling for the central bank to ease the pressure and a few investors had even predicted that it might cut interest rates. Instead, the People’s Bank of China ordered a thorough implementation of the new “mass line education” campaign launched this week by President Xi Jinping – a campaign that in its propaganda-style and potential scope carries echoes of the Mao era.

“It is quite possible that the central bank’s policies have some connection to Xi’s campaign,” said Willy Lam, an expert on Chinese politics at the Chinese University of Hong Kong.

Here’s another interesting quote from a China pundit — this time an economist:

“There are definitely political calculations,” said Ken Peng, an economist with BNP Paribas. “The senior leadership is much more worried about ‘correcting behaviour’ and political considerations than just protecting their 7.5 per cent growth target.”

The true inner workings of China’s political system can be elusive even to experts, and are certainly well beyond this blog, but the new-Maoist theme is further explored today by another of our FT colleagues in Beijing, Kathrin Hille. China’s new leadership is heavily promoting a year-long campaign, the “mass line”, apparently as a way of reaffirming its power in the face of internal fighting, public outcries over corruption and pollution, political scandals, minor outbreaks of democracy and other recent, possible threats to the Communist party’s hold.

And don’t forget the rather intriguing NYT report last week on the accelerated urbanisation of some 250m rural Chinese in 12 years. Details are still thin — it’sreportedly on the agenda for the Standing Committee of the People’s National Congress next week — but the implications of such a big and rapid move could be huge, both economically and politically.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.