FTAlphaville offers a novel explanation for the crunch underway China’s interbank markets today:

The popular explanation for the rise in Chinese repo rates is being linked to the government’s desire to rein in the shadow banking sector. That is to say the tightness is intentional.

But what if it isn’t. What if it has more to do with the unwind of yet another carry trade?

Deutsche Bank’s Bilal Hafeez made a strong case for this interpretation last week. We think it’s worth revisiting the argument.

There are three main factors that need to be considered, he argued:

Adjusted for volatility China now offers the highest FX carry in the world. This, he says, has led to a surge in flows into the CNY (and CNH) by both onshore and offshore entities over the last few years.

The performance of the carry was reaching breaking point last week.

Any combination of higher US yields, regulatory clampdown or higher FX volatility or CNY appreciation could trigger an unwind.

And as he warned, the demise of the carry trade would then remove an important channel of cheap funding for the Chinese economy.

Above all it would also diminish the amount of dollars flowing into the system. Dollars, we should add, that play a vital part in the PBOC’s liquidity distribution mechanism. No dollars, the harder it is to inject CNY liquidity into the Chinese economy. Or more accurately, liquidity injections have to become more dependent on Chinese bond repo.

It’s worth noting that a similar dollar shortage issues arose about the same time last year as well.

One should also consider that China has always been a direct beneficiary of QE programmes (or victim, if you look at it from an FX point of view) in that a lot of the dollars pumped in via the QE programme end up flowing in that direction regardless of what anyone does. Any expected Fed tapering thus has the potential to reduce these inflows.

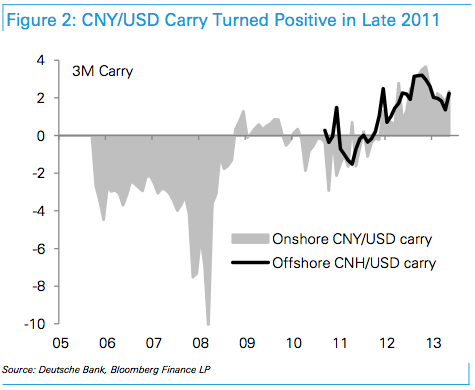

This is encouraged by the Chinese carry trade opportunity, which as Hafeez noted, was looking pretty frothy about this time last week:

Hafeez estimates the carry turned positive about the end of December 2011:

(This was about the time the dollar shortage issue first became notable, and when flows into CNY became notably less unilateral in nature. Since that time it’s worth noting the Chinese government has also widened the trading CNY/USD trading band, allowing for greater two-way flexibility).

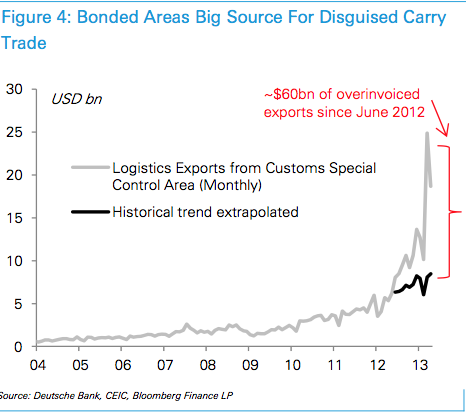

So when things got tight in the Chinese dollar markets last year, the market responded in innovative ways. Remember, the key was attracting fresh cheap dollars into the system, which could be transformed into higher-yielding RMB assets instead.

According to Hafeez a big source for the disguised carry trade was the practice of over-invoicing exports in bonded areas:

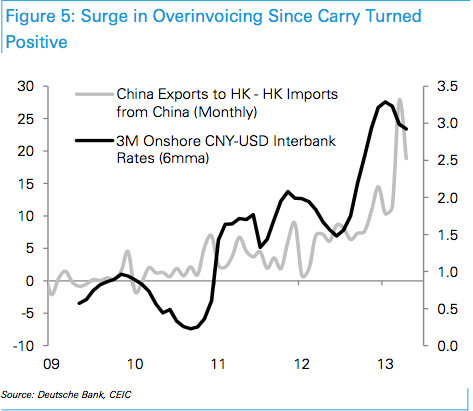

It’s worth noting there has been a veritable surge in invoicing ever since the carry trade became positive:

In short, rather than earning dollars on real exports, China may have turned to borrowing cheap dollars against export collateral instead. First as a means to compensate for lagged export demand and compensatory income, but later because it was incentivised to keep borrowing due to unique opportunity to benefit from one of the best carry-trades in the world — which effectively pays Chinese onshore entities to borrow dollars, exchange into RMB, and sit-back and collect the yield.

In short, China has secretly been borrowing a lot of money offshore by collateralising assets such as metal stockpiles and hiding it in the trade accounts not capital accounts.

This is not unlike the explanation offered by Phat Dragon, who sees a similar scramble for dollars but as a consequence of regulatory shifts that will be temporary:

The interbank liquidity squeeze continues. Phat Dragon noted in this chronicle a week ago that a number of regulatory initiatives were combining to crowd a high proportion of banks onto the bid side of the market. With data up to March, Phat Dragon estimated that around $US90bn of foreign currency would have to be purchased by the Chinese banking system to meet the new SAFE regulations by July 1. At the beginning of June there was still a major dollar purchasing task ahead – about $US63bn – the sudden urgency of which has been reflected in the disruptive moves in interbank rates and in the FX market. Within the last week SAFE has shown some forbearance towards foreign bank branches by softening their targets, but has shown no sign of letting up on domestic banks.

The People’s Bank has refrained from injecting abnormal amounts of liquidity to alleviate the squeeze, even with reports surfacing of a default by a medium sized local bank. With data on open market operations up to the current week, while there has been a net injection of funds in the month to date, it has been delivered passively via bill and repo maturities. Active liquidity boosting operations, i.e. the initiation of reverse repos, have been absent, while small bill and repo issuance has mildly diluted the gross passive injection. Indeed, the weekly net injection has got progressively smaller week by week since June began, which is hardly indicative of concern on the behalf of the monetary arbiter. Phat Dragon has been at pains to emphasize that the Chinese banking system’s current liquidity scramble is a regulatory/policy choice. A squeeze by fiat, if you will. The loan to deposit ratio for commercial banks if around 65%, 19.5% of the deposit pool sits latent as required reserves, RMB lending growth is running below deposit growth and the country remains a huge net international lender. This is not some tin pot frontier market being cast back upon an insufficient internal savings pool by a sudden withdrawal of external financing. The twin spikes in the SHIBOR and NDF curves should recede without fuss once the regulatory distortions work through the system.

Fair enough, but let’s not get too comfortable here. Naked Capitalism explains the law of unintended consequences in banking:

Given that accommodating central bank in economies with pretty good reporting was unable to forestall a meltdown, the Chinese central bank’s tough guy stance isn’t looking like the best reflex. The underlying concern isn’t just that there’s been a short term crunch, but that it comes against a backdrop of massive and increasingly low-productivity debt financed investment. And in another worrisome parallel to the crisis just past, it’s pretty doubtful that the authorities have any better handle of the size and interdependence in their shadow banking system than ours did in 2007. A sampling of alarmed commentary.

…And as [Patrick]Chovanec also points out, “all the liquidity injections in the world won’t save bad investments from being bad.” But disorderly failures can have knock-on effects to otherwise good but not terribly liquid holdings. That’s the logic of the Bagehot rule: in a crisis, lend freely against good collateral at penalty rates. The PBoC is playing Russian roulette by ignoring this principle. It may come out of this staredown fine, but this is a fraught exercise.

Let’s hope the PBOC has a better handle on the shadow banking system than anyone else seems to.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.