Late last week, Society Generale published a succinct note explaining its view of why China’s credit growth is accelerating but its growth is not.

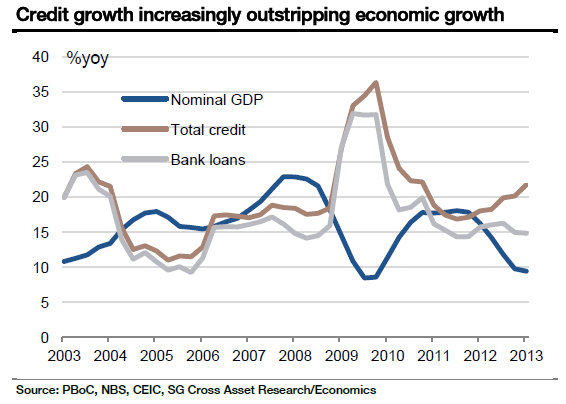

In the first quarter, China’s total credit growth – bank loans, shadow banking credit and corporate bond together – accelerated to the north of 20% yoy, more than twice the pace of nominal GDP growth. This gap has been widening since early 2012.

True, the gap was once close to 30ppt in 2009 and credit growth looked like leading economic growth most of the time in the past ten years. However, we still think the recent divergence is particularly worrying.

Since 2009, China’s credit growth has outpaced nominal GDP growth in every quarter except one (Q4 11), whereas, in previous years, economic growth managed to better credit growth more than half of the time. The excess borrowing that occurred in 2009 has never been absorbed by the real economy and now more borrowing is being piled on top of this.

In addition, the credit binge in 2009 was a result of the exogenous policy shock engineered by Beijing. Authorities were quick to boost credit supply within months of the breakout of the Great Recession, long before generic credit demand from corporates picked up. However, this time, the economic slowdown as well as the credit pick-up is largely endogenous…

Another big difference between the current situation and that which occurred in 2009 is the greater and increasing presence of non-bank credit…Borrowing from shadow channels like trusts are hardly a voluntary choice, as costs are often stiflingly high and duration unpleasantly short. Hence, there is an issue of adverse selection. It is those who are unable to roll over bank loans that have to tap the shadow banking system and refinance at more demanding terms…

Debt snowball

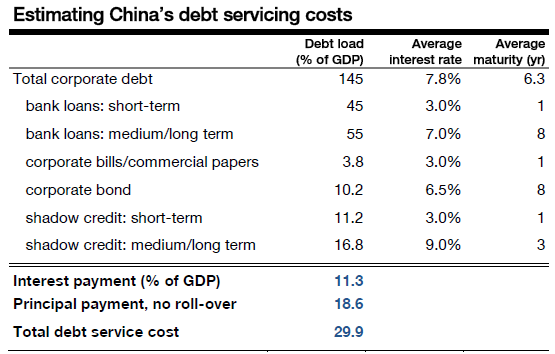

A fast rising debt load of an economy suggests either deteriorating growth efficiency or high and rising debt service cost, or in many cases both. There is clear evidence that China is suffering from both of these. We have written extensively on the point of declining growth and summarised the causes as: 1) excess capacity resulting from inefficient investment in the past and 2) increasingly marginalised private sector.

Here, we focus on the debt problem. Adopting the methodology from a 2012 BIS paper 1 , we manage to estimate China’s debt service ratio (DSR) at the macro level, and the result is very alarming…

A Minsky moment?

As a reference, the BIS paper estimated that a number of economies had similar or moderately lower debt service ratios (DSRs) when they were headed towards serious financial and economic crises. Examples include Finland (early 1990s), Korea (1997), the UK (2009), and the US (2009). This is one more data point in China that evokes the troubling thought of a hard landing.

However, we also agree that the actual DSR is probably lower. The assumption of an instalment-loan schedule implies that roll-over is not an option and all debt is fully repaid at maturity. This is clearly not the case in China…Hence, the logical conclusion has to be that a non-negligible share of the corporate sector is not able to repay either principal or interest, which qualifies as Ponzi financing in a Minsky framework…some degree of credit crunch will still be unavoidable in the next three years, which lends weight to our below-consensus medium-term growth forecast.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.