There are a raft of libertarian think tanks in Australia that do the country good. Given Australia’s basic entitlement nature, born of being spoiled by the resources endowment and the fair go culture, right wing think tanks are like electrodes applied to parts of the body politic when we get overly sleepy.

The Centre for Independent Studies in Sydney has housed some great minds over the years including foreign policy legend Owen Harries and some solid thinkers these days as well like John Lee. Most its output is thorough even if its assumptions are more libertarian than my tastes.

The Sydney Institute is another good operator. Though not quite libertarian, its lecture series are usually timely and what Gerard Henderson lacks in intellectual heft he usually makes up for in chutzpah and balance of delivery.

But Melbourne’s equivalent think tank, the Institute of Public Affairs, does not cover itself in glory today with its the boss, John Roskam, calling for radical cuts to the budget:

Tony Abbott and Joe Hockey must burn the boats. The Coalition must promise to not increase taxes and not impose any new taxes if elected. That means no increase in the GST, no new levies like the one Julia Gillard wants to impose to pay for part of the National Disability Insurance Scheme (NDIS), and no changes to the tax deductions taxpayers can claim.

The only way Abbott and Hockey should return the federal budget to surplus is by cutting government spending.

The story goes that when Alexander the Great landed in Persia he burned the boats his army arrived in. Retreat was thus ruled out. There was no Plan B. Either Alexander and his troops succeeded or they died. Alexander succeeded.

This is high rhetoric. But as the piece continues, there is a conspicuous absence of argument. Just the old libertarian platitudes:

A promise of no tax increases and no new taxes will do a few things. For a start it will prove the Coalition is serious about reducing the size of government. It will also impose discipline on ministers and their departments. Abbott points out that 16 of his current front bench were ministers in the Howard government. That’s a mixed blessing. The last experience those 16 had of ministerial office was in 2007 at the height of the mining boom and before the financial crisis, when money was no object.

Now, don’t get me wrong. I am in favour of lower taxes and reckon that capital is generally deployed better in private hands than public, if only by sheer weight of numbers. But as we slog through a terms of trade adjustment as well as jump off the mining investment cliff, insisting that budget surpluses must be achieved only through spending cuts will only grow the government share of the economy. How so?

Private sector growth is already weak on fiscal consolidation, falling national income via a terms of trade correction, a high dollar and tepid credit growth. As mining investment falls, withdrawing some 1.5 to 2% of GDP per annum for the nest three years, the dollar will dropbut we have very successfully hollowed out much of our non-mining tradable sectors so the investment rebound will be muted. Falling interest rates are not rebounding credit growth anything like fast enough to fill the gap (and it would be unwise to try).

So, cutting public spending further, by the $30 billion or so needed to ensure a decent surplus, will have one effect only, weakening an already soft labour market. No doubt the libertarian riposte would be that the Ricardian confidence fairy will sprinkle his magic dust as the government does the nation’s saving and private sector risk appetite returns. But the more likely outcome in today’s risk averse times is that the job cuts will further retard credit growth and risk a shift by the private sector back into deep saving mode. At that point we will be staring straight into the maw of a 2014 recession.

Now, libertarians may argue that that is not such a bad outcome. We need to reset the economy on a lower cost base to begin attracting capital once more.

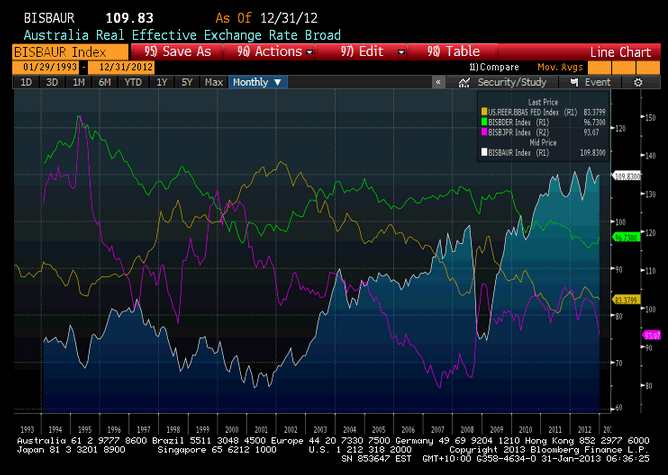

And it’s true. The problem is that we have a long way to fall before we’re competitive enough. Australia’s real exchange rate is extraordinarily high, miles above the US, Japan or Germany:

Long before you find the a level of competitiveness that boosts investment, the labour market will implode and a feedback loop of bad debts into the banking system will form. That will very quickly turn into a housing bust and, let’s be honest, if that happens our recession will become a mini depression with unemployment at least doubling.

As this process transpires, government tax revenue is going to tank even as the automatic stabilisers raise spending. The targeted surplus will evaporate. If the government reacts by cutting further, then the bad debt feedback loop will get stronger and we’ll unravel much more quickly.

At the end of this process the upshot is that the banks will require a bailout, probably via nationalisation of the LMIs. Government debt will explode and its proportion of the economy will likely reach post war highs.

During the coming adjustment, it is far better to let modest public deficits support aggregate demand. Aim everything you’ve got at productivity gains. Slash interest rates as low as they need to be to get the dollar down and prevent a credit explosion through macroprudential measures. Put your head down and hope global markets don’t notice the current account deficit until the LNG export boom kicks in between 2015 and 2017. Then cut your deficits.