Goldman Sachs yesterday released an uber-bullish forecast for US equities:

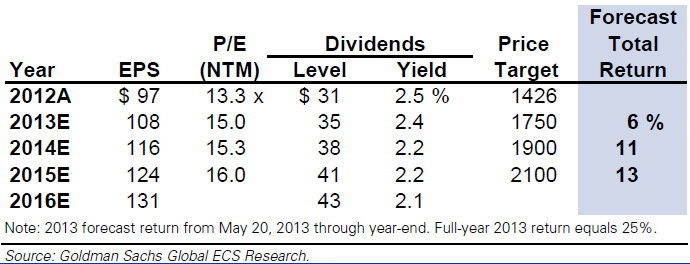

End of US economic stagnation suggests S&P 500 P/E expansion In advanced economies, P/E multiples expanded by an average of 15% during the year before GDP growth returned to trend. Our year-end 2013 implied forward P/E of 15x would represent a 13% increase vs. 2012.

Our S&P 500 forecast reflects a one P/E multiple point premium

Reasons for P/E expansion include confidence in the medium-term outlook for US economic growth and the wide gap between equity and persistently low bond yields that we assume will be closed more by stocks than bonds.

We expect dividends will rise by 30% between 2013 and 2015

We forecast dividend growth of 11% in both 2013 and 2014 and 9% in 2015. Our EPS forecasts remain unchanged but we have lifted our payout ratio assumptions after surprisingly large 1Q year/year dividend growth of 12%.

Further multiple expansion possible if rates stay low, growth improves

If interest rates stay low despite better growth then upside to S&P 500 may be greater than we currently forecast. Monetary easing by Fed, BOJ, and ECB keeps sovereign yields low and would support this potential outcome.

The assumptions that underpin this forecast are the fly in the ointment:

Advertisement

We forecast the US economy will achieve above-trend real GDP growth in 2014, ending a six-year period of economic “stagnation”. Since 2009, the economy has been expanding, but at a below-trend pace. Equity markets have typically re-rated by 15% in anticipation of the end of multi-year sub-trend growth. Combined with better equity flows and stronger employment and housing data we believe the S&P 500 P/E multiple will continue to rise, reaching 15x at year-end 2013 and 16x by the end of 2015.

GS sees no problems in dealing with fiscal retrenchment, no chance of withdrawn monetary stimulus and no issues for growth if bond yields normalise and the report doesn’t once mention the US dollar. If the US is going to grow above trend then employment is going to grow above trend (unless productivity does which is unlikely given it is slowing). And monetary stimulus is going to be at least tapered as the labour market bounces. GS does address this in arguing 8 million more jobs will be needed before the Fed tightens. I agree that the Fed is a dove. But if the labour market bounces so strongly, I’m confident it will taper.

But that is really besides the point. I see little chance of above trend growth in the US next year. The steady grind will go on, held back by fiscal retrenchment, weak external conditions emanating from Europe and increasingly Asia, and a rising dollar.

Advertisement

But don’t despair! The kicker in the GS forecasts is that this would result in higher still equities prices:

Under ideal conditions, where US yields remain low (and real yields remain negative) despite improving domestic GDP growth, there could be substantial upside to S&P 500 valuation. The most plausible way for that combination of events to occur is weak growth in Europe and some emerging market economies alongside aggressive easing by developed market central banks which would keep US rates low even as domestic economic activity improves. Under that scenario the S&P 500 P/E could rise above 17x.

A much more likely scenario and who’s to say the S&P500 wouldn’t keep rising to such levels in this event? Inflation would be non-existent as commodities fall, there’d be no threat to housing from rising bond yields, the Fed would stay easy longer preventing the dollar from taking off and fiscal consolidation would be paced against below trend growth. It’s simply a continuation of the financial repression we have now. Equities could march to any height.

Advertisement

But there is a key difference in the two scenarios. Goldman’s dividend driven bull market would have become instead a financial repression equities bubble waiting for a penny to drop.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.