The ABS has released the much awaited March quarter Private New Capital Expenditure and Expected Expenditure report and the news is better than feared.

The sixth estimate for 12/13 expected expenditure is $163,018 million. This is down 2% in the quarter, which is a normal reduction. The second estimate for 13/14 was also solid at $156,467 million. This is 3.4% higher than Estimate 1 for 2013-14, again a pretty normal pattern:

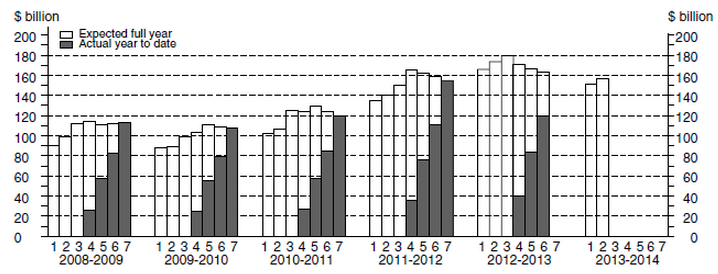

However, like the last estimate, the internals didn’t show much in terms of rebalancing. Mining held up well despite the circumstantial evidence to the contrary, coming in at $101,897 million, suggesting at this stage a plateau for investment over the next year, not a decline:

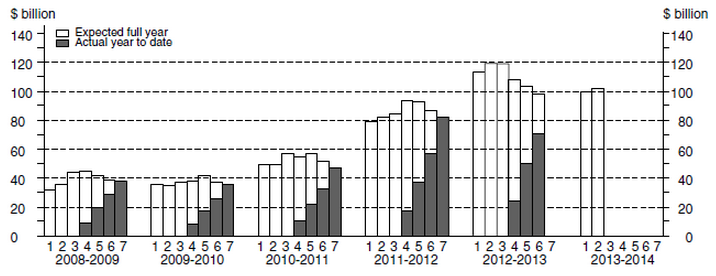

Manufacturing remained on the nose:

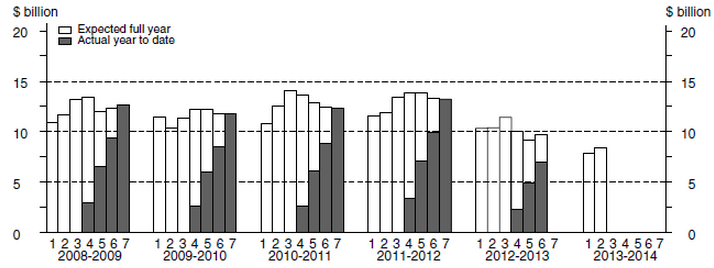

And other came in at $46,204 million. This is 5.6% higher than the corresponding estimate for 2012-13. The main contributors to this increase were Rental, Hiring and Real Estate Services (28.1%) and Transport, Postal and Warehousing (8.9%). Estimate 2 is 4.5% higher than Estimate 1 for 2013-14. Buildings and structures is 5.2% higher and equipment, plant and machinery is 3.9% higher than the corresponding first estimates for 2013-14:

This level of growth is consistent with past surveys but may hint at a little rebalancing.

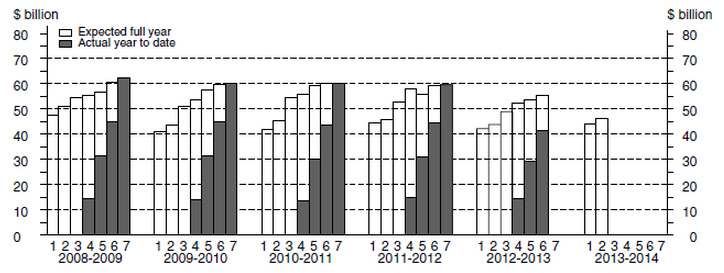

So, in sum, one for the bulls with the pipeline holding up, though as the RBA has observed, this survey has routinely overestimated future spending in mining as you can see in the above chart of the recent history second estimates versus final spend (that is the second clear bar in each yearly series versus the final shaded result). We saw it again today in the result for the first quarter which seriously undershot (see other post). The opposite is traditionally the case for “Other” and manufacturing is in between.

The dollar plunged when it saw the headline result but has now rebounded as the future spending component filters through markets (or on better building approvals).

There is some comfort here. Perhaps enough to hold further rate cuts at bay for the time being unless iron ore keeps plunging.