So you take a 2 week holiday, and when you return you find the IMF have switched sides!

“Fiscal policy should be appropriately calibrated to be as growth-friendly as possible,” the International Monetary and Financial Committee said in a communique.

The statement came after days of back and forth between those — led by Germany — urging no let-up from belt-tightening and those arguing for a loosening of the grip of austerity.

International Monetary Fund Managing Director Christine Lagarde said on Thursday she was happy for Greece — struggling under the weight of cuts demanded by international creditors — to have two more years to meet its deficit reduction targets.

So has the IMF suddenly woken up the fact that demanding every government slash spending and raise taxes is, in many cases, counter productive because they have underestimated the fiscal multiplier in government spending ? No this isn’t new. As I noted back in August 2011, the IMF along with its new President have been well aware for some time that their theories on expansionary fiscal contraction have underestimated the negative effects of attempting government sector austerity at a time of private sector de-leveraging, specifically in a fixed currency environment.

Germany’s finance minister said Friday there is “no alternative” to cutting debt in European countries, a day after the head of the IMF called for Greece to be given more time to pare its deficit.

“There’s no alternative to reduce in the medium term too high sovereign debts, especially and of course for… the eurozone as a whole,” Wolfgang Schauble said in a debate with IMF managing director Christine Lagarde in Tokyo.

Lagarde on Thursday appeared to soften slightly on the need for heavily indebted countries to trim their fiscal cloth, when she said: “Instead of frontloading heavily it is sometimes better… to have a bit more time.”

She said the IMF was happy for debt-addled Greece to have another two years to get its fiscal house in order and bring budget deficits down to levels agreed with international creditors.

Schauble is correct, there is no alternative to cutting debts across the Eurozone, but that isn’t actually the point of Lagarde’s comments. The real point is whether the current strategy is actually working in doing just that and if we look at the trajectory of debt in much of the European periphery the answer appears to be no. Greece is the leading example:

Euro zone officials are considering new ways to reduce Greece’s huge debts because delays to reforms by Athens and continued recession have put the target of a debt to GDP ratio of 120 percent in 2020 out of reach, euro zone officials said.

A Greek debt sustainability analysis prepared by the International Monetary Fund, the European Central Bank and the European Commission in March forecast Greek debt would rise to 164 percent of GDP in 2013 from around 160 percent in 2012 under a baseline scenario assuming the Greek economy would stop contracting next year.

But Greece now expects its economy to shrink by 3.8 percent in 2013, its sixth consecutive year of contraction, boosting its debt ratio to 179.3 percent.

“At the moment it looks like Greece’s debt level will rise to well above the target of 120 percent of GDP by 2020,” ECB Executive Board member Joerg Asmussen told the Sueddeutsche Zeitung newspaper.

Schauble went on to say that it does not build confidence when policy is changed midway through its political course, which I agree with, but given the solid backtracking from northern creditors, including Germany, on pledges made at the July summit its a fairly ironic statement in my opinion. Schauble went on to use this example to demonstrate his point:

When you want to climb a mountain and you start by going down, the mountain gets higher

The black hole in Spain’s budget has expanded faster than Prime Minister Mariano Rajoy’s attempt to shrink it, portending the same unrest roiling Greece.

The harshest austerity since the return to democracy in 1978 has failed to contain the deficit as the economy sinks deeper into recession. The shortfall increased in the first half of the year, as it did in the previous 12 months. Even after a sales-tax increase and health-care cuts kick in this quarter, it may still approach last year’s 9.4 percent of gross domestic product, said Ignacio Conde-Ruiz, an economist at the independent applied Economic Research Foundation in Madrid.

And like other periphery countries before it, this sliding further down the mountain is met with lower ratings:

S&P warned that rising unemployment and harsh austerity measures are likely to intensify social unrest and cause further friction between Spain’s central and regional governments.

“The downgrade reflects our view of mounting risks to Spain’s public finances, due to rising economic and political pressures,” said the rating agency in a statement.

“In our view, the capacity of Spain’s political institutions (both domestic and multilateral) to deal with the severe challenges posed by the current economic and financial crisis is declining, and therefore, in accordance with our rating methodology (see “Sovereign Government Rating Methodology And Assumptions,” published June 30, 2011), we have lowered the rating by two notches.”

The downgrade to BBB- from BBB+ late on Wednesday leaves Spain one notch above “junk” status. S&P also attached a “negative outlook”, which warns of a possible downgrade in the medium term.

This should come as little surprise to MB readers, as I stated back in July this was all just a matter of time as the existing policy responses are ultimately counter-productive to debtors and creditors alike. Of course the ECB is waiting in the wings with its OMT and this latest ratings downgrade could be the trigger that finally forces Rajoy to seek external help. This is exactly the dynamic that is keeping Spanish bond yields suppressed even though the economy is worsening. However, it should be noted that a further downgrade to “junk” will force up margins on Spanish bonds at clearing houses and also remove them from investment grade indexes. This what we saw in the case of Portugal which is why their bonds deteriorated so rapidly.

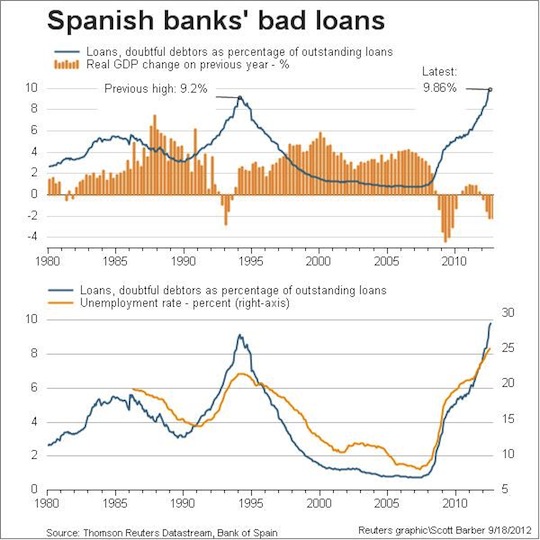

In the meantime the Spanish housing market continues to deteriorate with cumulative declines in the Tinsa housing index increasing to 32.9% from peak in September. Once again Catalonia is leading the pack with the “Mediterranean Coast” falling 39.2% followed by 36% for “Capitals and Major Cities”, 33.2% for “Metropolitan Areas”, 28.6% for the “Balearic and Canary Islands” and 28.5% for “Other Municipalities”. Given the circumstances I can only assume that this means a further increase in the already record high bad debts in the banking system which will again apply more pressure to the government.

{kind=link}

As I stated above the current response isn’t helping anyone long term. The bailouts and the monetary policy responses are buying time for the creditors at further expense of the debtors, but the creditors certainly aren’t climbing any mountains either. Unsound credit and bad loans are being masked by these monetary operations but as part of their implementation the real economy of the Eurozone is weakening while social tensions rise. As we’ve seen with Greece this ultimately means the creditors are forced to wear the costs anyway.

The IMF has signaled once again that it believes the current plan is failing and, as I stated nearly a year ago would eventually occur, are slowly pushing back against the fiscal framework. It’s early days but given the developing weakness across the zone I wouldn’t be surprised to see some more side-switching on fiscal policy in the coming months, even from the supposedly stringently fiscal responsible (even though most of them are not).