The Commonwealth Treasury released a consultation paper last month on propose reforms to Fringe Benefits Tax (FBT), particularly, the tax treatment of Living Away From Home Allowances (LAFHA).

Apparently there are two major concerns leading to this reform. The first, but unstated reason, is to increase tax revenue – which is more clearly articulated in the Treasurer’s statement:

LAHFA tax-free increased from $162 million in 2004-05 to $740 million in 2010-11. The reform will raise taxes by $683.3million over the forward estimates.

The second reason is described as follows:

A particular concern is the growing use of the concession by employers (including through labour hire and contract management companies) to allow temporary resident workers coming to Australia to convert their taxable salary into a tax‐free allowance. This provides them with an unfair advantage over local Australian workers.

… An area of growing concern is the use of LAFHA by employers (including through labour hire and contract management companies) to attract temporary resident workers to Australia by including tax‐free LAFHA payments as part of their remuneration. These payments are effectively a re‐characterisation of taxable salary or wage income

…The changes will ensure a level playing field exists between hiring an Australian worker or a temporary resident worker living at home in Australia, in the same place, doing the same job.

Indeed, as the paper suggests,

The living‐away‐from‐home allowance is one of the most popular searched terms for workers on the 457 Visa.

So what are the changes?

Put simply, to claim accommodation costs and food expenses as a fringe benefits tax exempt LAFHA allowance, the employee must maintain a home in Australia they are living away from for work. This is a change from the current treatment whereby there needs to be no evidence of actually living away from an Australian home for temporary visa holders (who, by definition, are living away from home, although not required to actually maintain a home). They, and their employer, are simply enjoying a tax advantage compared to a local worker.

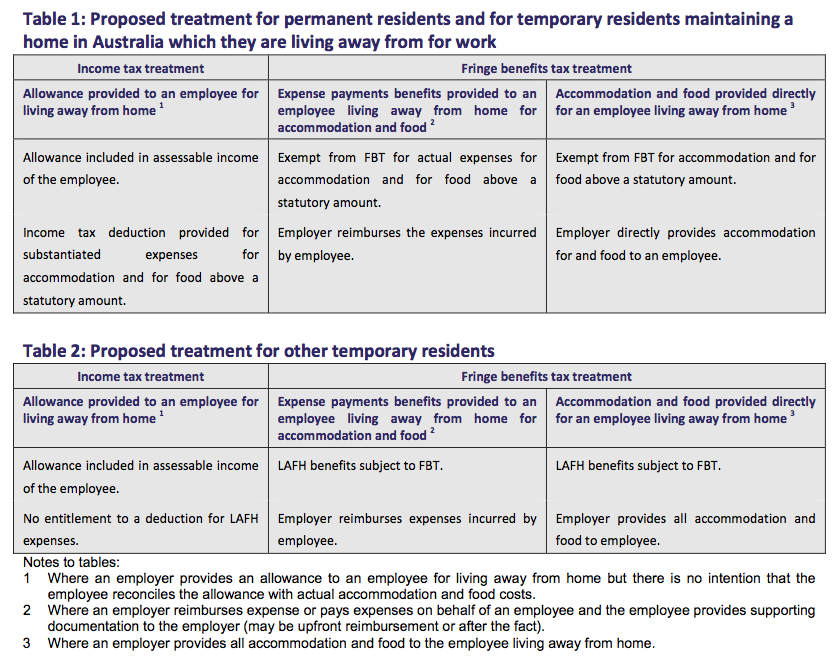

The second change involves tightening the qualifying criteria to ensure that any FBT exempt LAFHA reflects the actual costs incurred. The below table summarises the proposed new tax treatment.

We know that this will turn off a $683million tax loophole. But just how many people could have their working conditions affected by the change? And what flow-on effects can be expected?

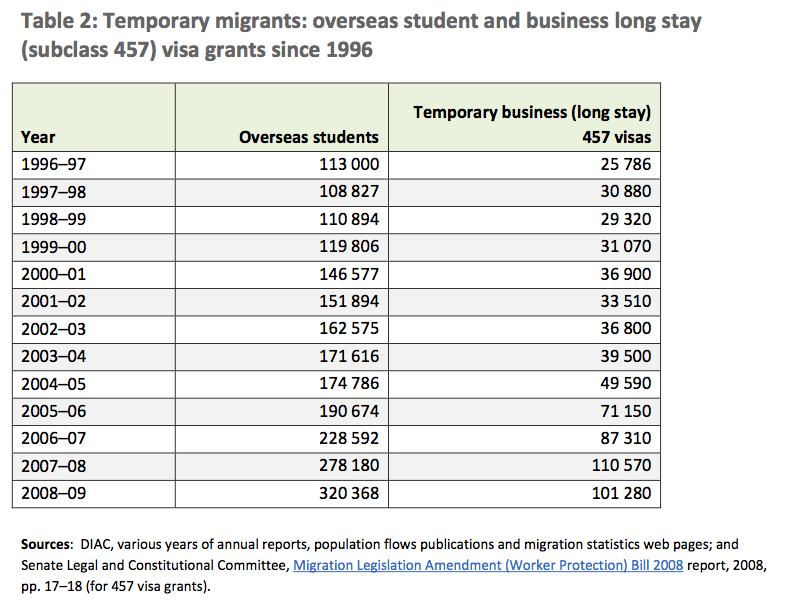

First, temporary residents on 457 visas are they key group able to access LAFHA tax advantages, and will be the main group affected by the reforms. We can see in the table below that there has been a significant boom, and tapering in 457 visa numbers since the mid 2000s.

Currently, around 1% of the workforce is made up of the approximately 110,000 457 visa holders, but this is expected to grow over the coming years, as reforms implemented in November allow for a more streamlined visa approval process, and longer stays of six years.

I imagine the likely flow-on effects to be most acute in the real estate markets of mining-boom towns. The new incentive means that domestic and foreign workers may prefer fly-in fly-out arrangements, as relocating becomes less attractive in after-tax terms, even if the cost of employment to the company is the same.

In terms of rental markets nationally, this will take tiny slice off demand at the margins, as this foreign workforce, occupying around 3% of rental homes, will be less enthusiastically spending tax-free income on accommodation. The top end of the city markets will see much of this change.

The big question politically is whether this will have much of an impact on the demand for overseas skilled workers, and whether it will encourage the education and training of local workers by industry groups for their own future benefit. I can’t say there being a major impact, but the uproar from the employment agent industry seems to suggest that the impact on the ease of attracting foreign workers may be significant. At any rate, these reforms will provide a better set of incentives for local skill development.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin