Recently American billionaire investor Warren Buffet wrote this article in the opinion pages of the New York Times arguing that the super-rich (top 400 personal incomes) have been molly-coddled by tax reforms of the past three decades. Buffett noted that he only paid an average tax rate of 17.4%, while the tax burdens of his office staff averaged 36%.

Buffett made the following suggestions

…for those making more than $1 million — there were 236,883 such households in 2009 — I would raise rates immediately on taxable income in excess of $1 million, including, of course, dividends and capital gains. And for those who make $10 million or more — there were 8,274 in 2009 — I would suggest an additional increase in rate.

Buffett’s opinion is not taken lightly, and as a result of his musings President Obama has included the Buffett Rule in his budget plan being pushed through Congress. Put simply, the rule aims to ensure that people with incomes greater than $1million will pay at least the average tax rates of the income earning middle class.

Like all grand promises, the devil is in the detail. The rule may require different types of income to be taxed differently (that was Buffett’s reason the super-wealthy pay less tax on average), which could increase average tax rates for some middle-income earners. Buffett himself is reserved about the application of ‘his’ rule, choosing to note that his main point was that the super-rich – the top 400 incomes – should be the target of reforms due to their astronomical ability to pay (and low relative impact on their wellbeing), rather than the normal-rich.

To my mind Buffet’s point is sound – the average rate of income tax paid should increase with income (progressive income taxation). And with income inequality also increasing in Australia we should expect much more focus on this redistributive aspect of income taxation as the trend continues.

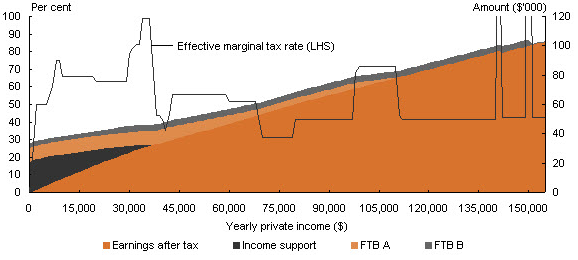

But the most important debate regarding income taxation is not the degree of progressiveness of income taxation, which is important due to perceptions of fairness (remember income is simply the incidence of a tax, and money not taxed by income tax continues to circulate in the economy to be taxed at other transactions). The important debate, regarding the way income taxes change behaviour, is over the effective marginal tax rate (EMTR) for low-income individuals and families. A well considered topic in the Henry Tax Review, and likely to be a topic of interest this week at Wayne Swan’s somewhat redundant Tax Forum.

EMTR is the reduction in take-home income from earning an extra dollar after due to the combined effects of income tax and reduced welfare payments. So while marginal income tax rates may be lower at low incomes, as any welfare benefits are being phased out (which typically reduce by 20c for every extra dollar you earn) there is often the perverse situation in practice that low income earners have a higher effecting marginal tax rates than the highest income earners. Economists call this perverse outcome a welfare trap.

There is clear evidence of high EMTRs, especially for families in Australia.

…families with children are more likely to face an EMTR of 50 to 70 per cent than other types of households, due to the accumulation of withdrawal rates for family related payments on top of income support withdrawal and income tax. This is observed even without including the withdrawal of childcare subsidies. On average, the EMTR is highest for couples with dependent children. (here)

In the Henry Review the below graph was shown to demonstrate the point, while many submissions from stakeholders also noting that this should be a key focus of reform.

Recommendations 99 and 100 from the Henry Tax Review did note the impact of childcare payments on the EMTR of working families (apologies for the use of Rudd’s favourite phrase). 80%+ EMTRs for families earning $35,000pa is not providing any incentive for these families to get ahead.

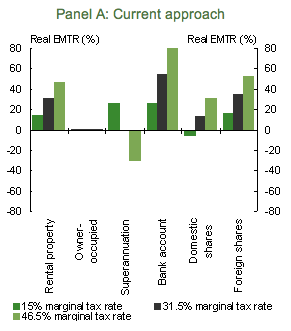

The variation between marginal tax rates of different types of income also distorts investment behaviour.

Very different effective tax rates on savings placed in bank deposits, owner occupied homes, other real estate, shares and superannuation distort the mix of investment and reduce the aggregate return to the nation’s scarce aggregate savings.

As the Henry Tax Review shows, bank deposits are the worst place to put savings in Australia. This might explain the trend in savings rates observed prior to 2006. It also explains why the wealthy, who earn most of their income from investment, can pay lower tax rates and lower marginal tax rates, than job-income earners.

After examining the Buffet Rule alongside the genuine problems of current income tax regimes, I am going to suggest an improvement on both Henry’s recommendations and the Buffet Rule itself. Implement a ‘Rumple Rule’ that equalises marginal tax rates for different sources of income (as suggest in the Henry review), AND ensures that EMTRs are flat or rising with household income. There are suggestions by some on this matter which warrant further investigation, but the focus probably needs to be on simplifying the welfare system first, and simplifying income taxation second (but keeping income taxes to ensure at least flat marginal tax rates).

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin