Westpac and the ACCI today released the 200th edition (started in Dec 1961) of their quarterly joint survey of Australian industry and it does not make comfortable reading.

Westpac says in the summary conclusion that:

This is a survey which is sending a very clear message. It is time for the authorities to ease financial conditions. Inflation pressures are weak; labour markets are soft; and investment and export plans have softened. Westpac predicted that the Reserve Bank would cut rates in December back in mid July. The case for lower rates is now strong. This survey enforces that case.

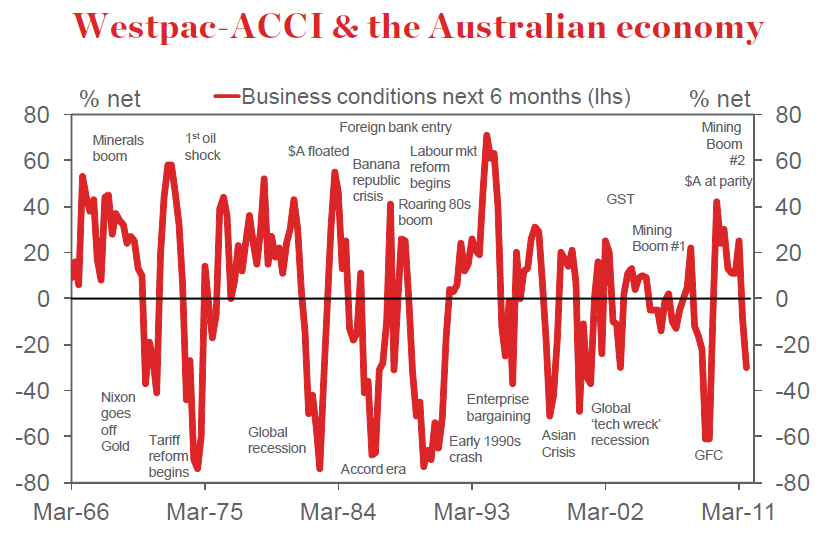

The chart that says it all from the front page is below and you can the combination of a mining boom and a high Australian Dollar on the survey:

Here is the rest of the high level summary and the full report is attached below.

- The Westpac–ACCI Actual Composite Index fell 1.2 points from 48.9 in June to 47.7 in September. Responses were collected between August 2 and September 9. The Index remains firmly in the contractionary zone in the second consecutive quarter.

- The Expected Composite fell from 53.1 in June to 49.8 in September. Over the last six months the Expected Composite has fallen by a stunning 15.3 points.

- The outlook for general business conditions fell to a net balance of –30 from –9 in June and +25 in March. That six month deterioration is sharper than in 2008/09 when the net balance bottomed out at –60.

- Labour demand softened further with the Labour Market Composite falling from –0.2 to –1.9. More disturbingly the availability of labour increased appreciably. The availability indicator fell from +14 to –8. In December 2008 the net balance shifted by 35 points. This print stands as the sharpest turnaround in labour availability since that period.

- Consistent with this evidence of a freeing up of labour, firms have become much more confident about their ability to contain wages. Price and cost pressures also fell sharply.

- Expectations around exports slumped significantly. The net balance for export expectations fell from 2 in June to –9. That is the lowest net balance since the time of the Asian Crisis.

- Firms’ profit expectations slumped further. After tumbling from a net balance of 22 in March to 0 in June expectations fell further to –4 – the weakest read since 2009.

So not something to be read before bed time or without an adult beverage, as John Mauldin likes to say. Time our friends at the RBA took these indicators a bit more seriously.