DXY faded with safe havens:

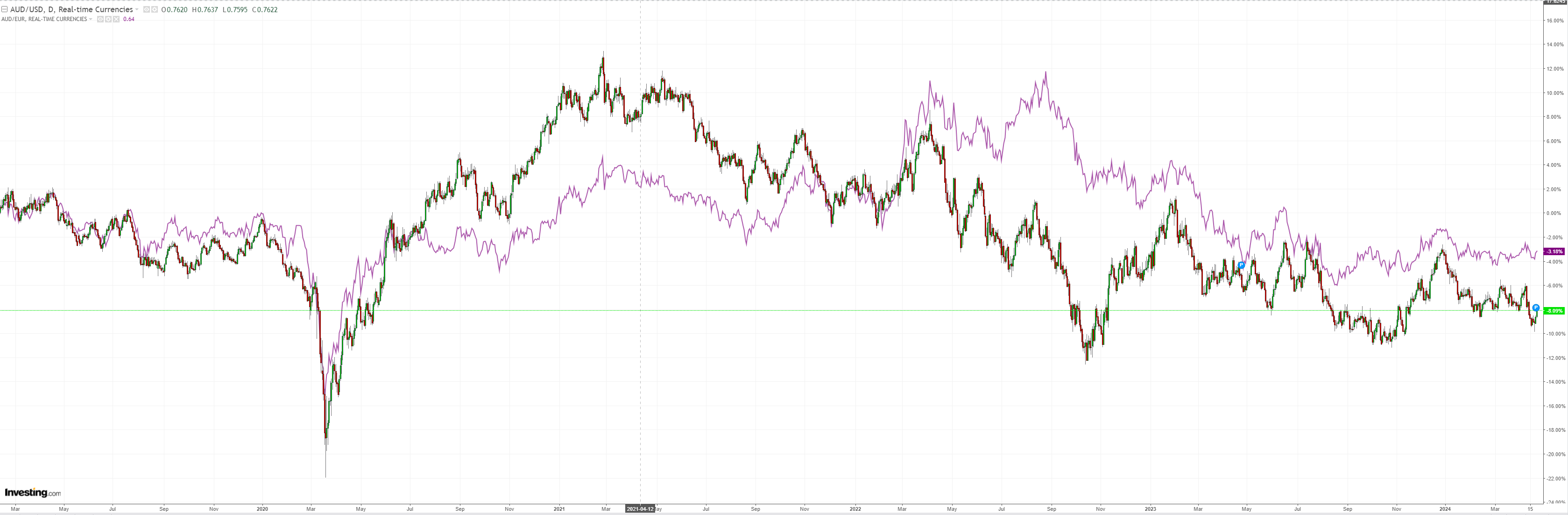

AUD powered out of the Israel/Iran phony war:

It won’t get far without North Asia:

Oil firmed, and the golden whale was harpooned:

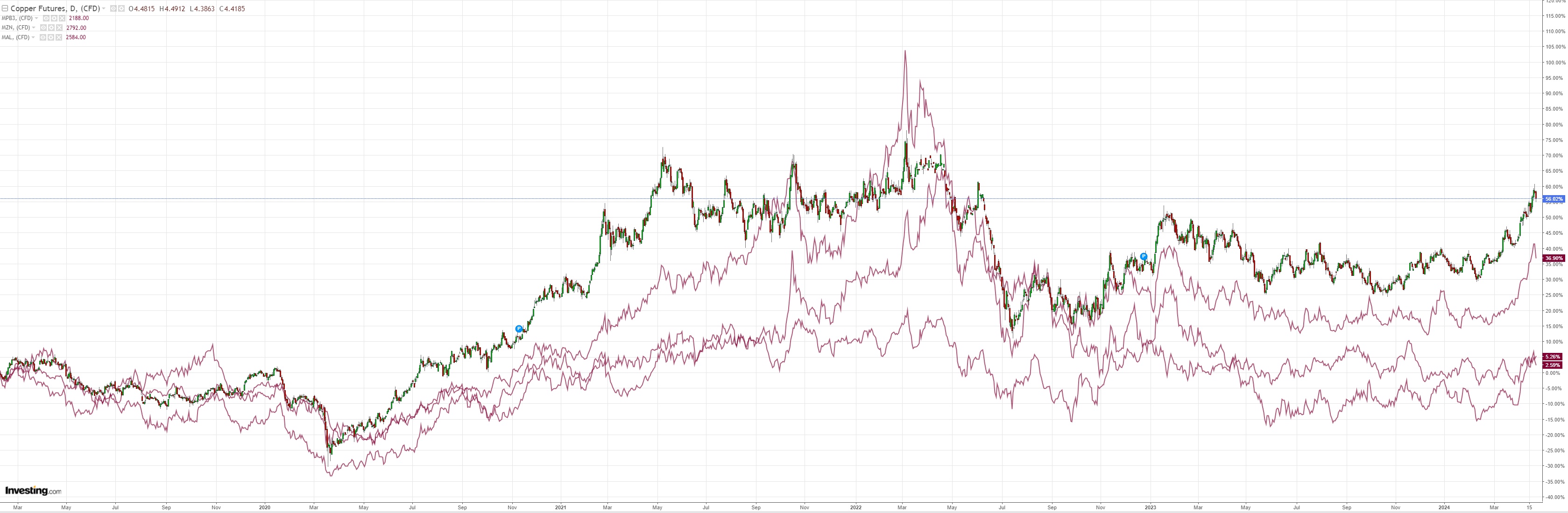

No landing metals puked:

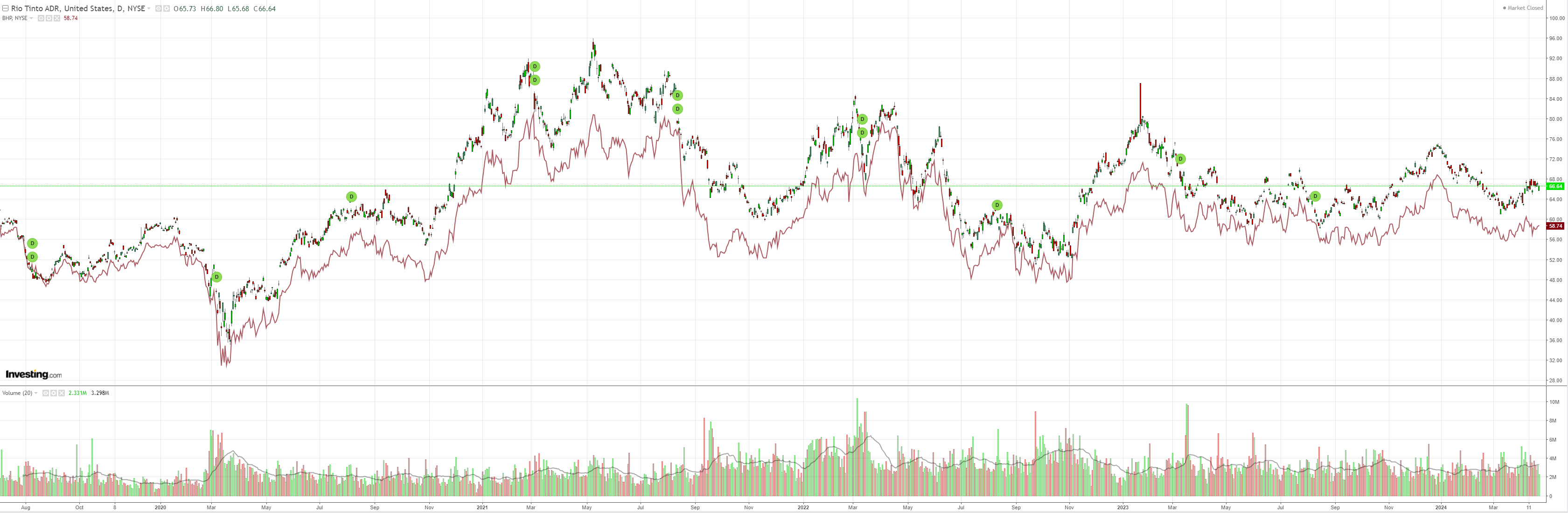

Miners meh:

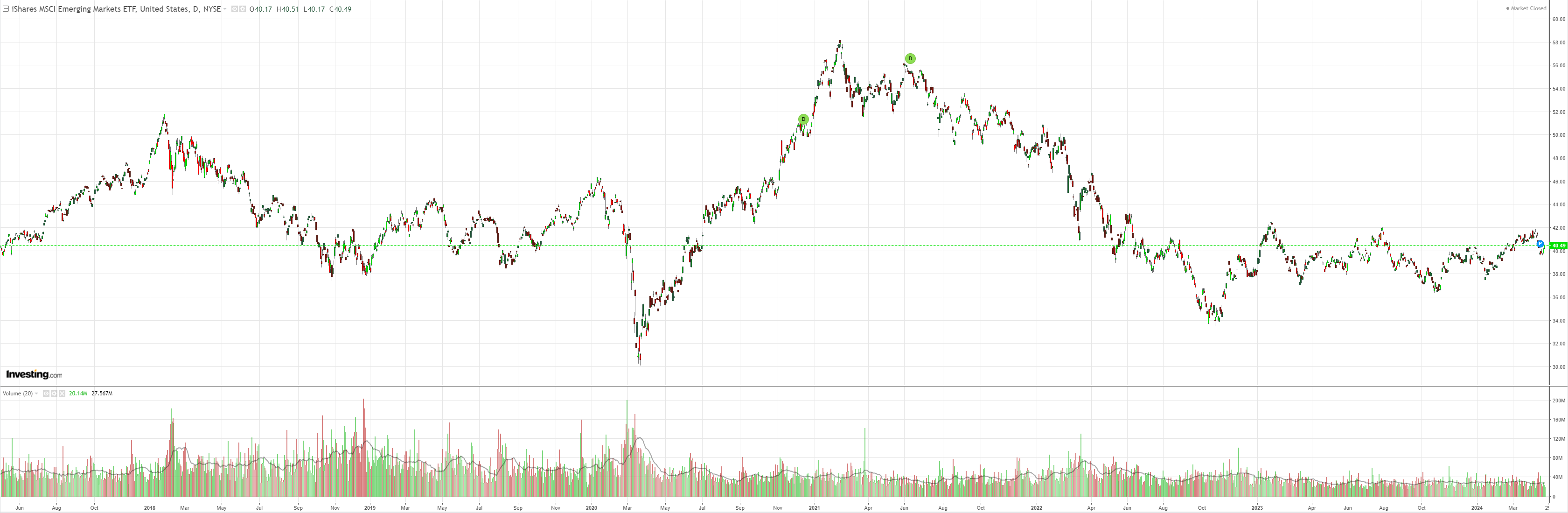

EM meh:

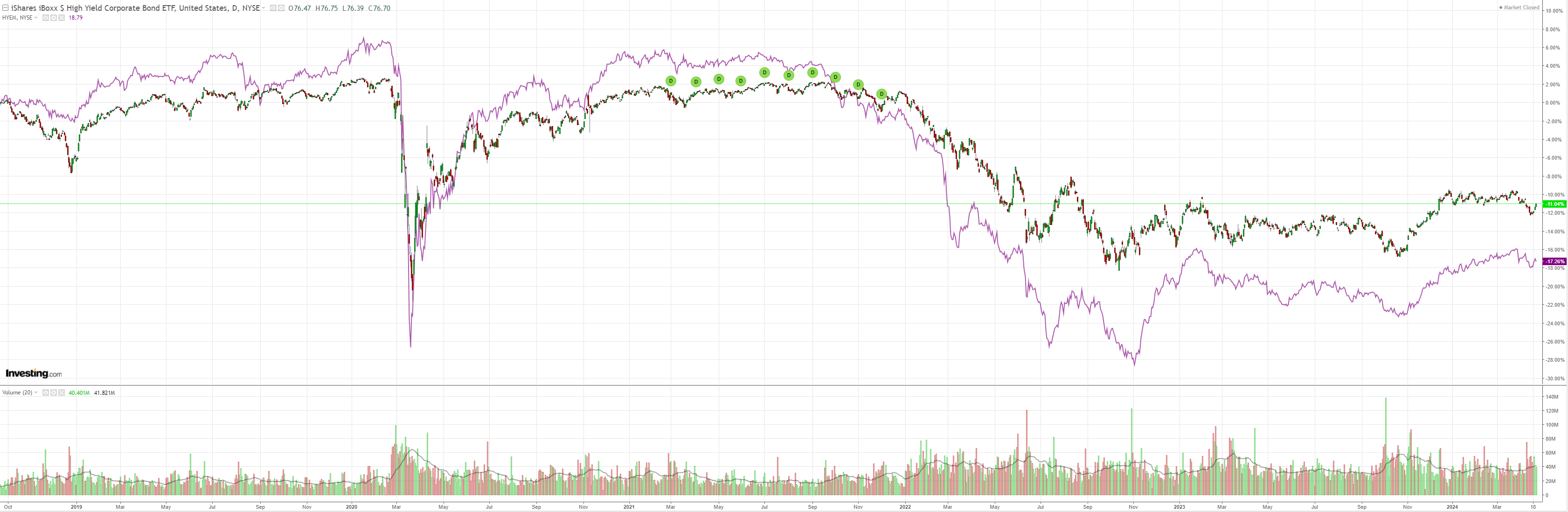

Junk was mixed:

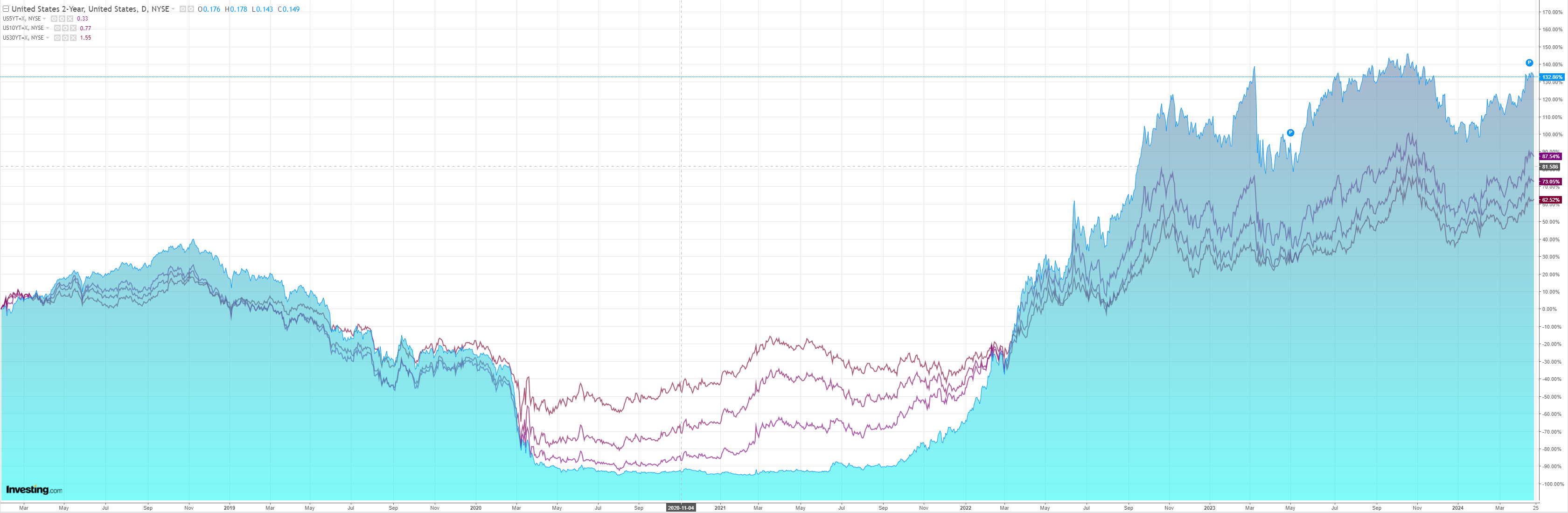

Yields are waiting:

Stocks loved the phony war:

We are off to see the Wizard of Oz again. The phony Middle East war is pretty much cooked for markets. We’re into earnings now.

This is not a “no landing”. It is a classic soft version. BofA:

6%EPS beat(3% ex-Fins), 1% sales beat (in line ex-Fins) 72 S&P 500 companies (21% of index earnings) have reported so far.

Reported EPS beat by 6%, driven by Financials (+3% ex. Fins), while reported sales beat by 1%, driven by Financials. 69%/56%/46% beat on EPS/sales/both, all weaker than last quarter’s73%/65%/51%.

The proportion of sales beats is also weaker than the historical average (59%), suggesting a continued sluggish demand backdrop.

1Q consensus EPS is down 2% (flat ex-BMY acquisition costs). Our 1-mo. guidance ratio is tracking at 0.7x, the highest level since October 2023, but weaker than the average April ratio (1.1x).

Despite signs of a reversing trend between services and goods, earnings indicate continued strength in services and weakness in goods.

While we believe the de-stocking cycle is over, truckers’ earnings indicate a re-stocking cycle hasn’t taken place yet. TSMC also cited weakness in autos and hardware (seeTSMC).Butleadingindicators(pg.5), capex trends (pg. 6,Mega projects, and CSX comments on pg. 2), and recent pricing dynamics) all suggest the manufacturing cycle should be inflecting higher.

Pockets of companies and consumers are benefiting from higher interest income.

80% of S&P debt is long-term fixed, and even if rates stay at current levels over the next five years, the cumulative EPS hit is estimated to be just 5% (but 32% for the Russell 2000-see SMID impact).45% of non-Fins companies also saw net interest expense fall vs.2021,and 40% have lower net debt.

Similarly, Baby Boomers who own 50%+of total household wealthof $150T(5.5x nominal GDP) are enjoying the 5% return on cash savings ($8T) with locked in mortgage rates.

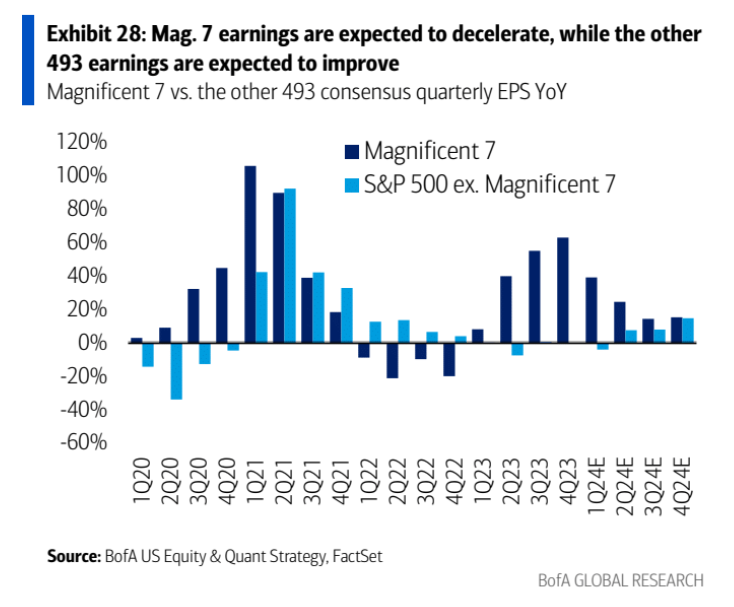

This is classic soft-landing stuff, as the Mag7 gives way to a broadening recovery after five straight quarters of mildly falling earnings in the 493. Also note how all of US private debt is termed out, leaving equity as the price maker for the economy.

So long as oil is kept in a box, this can be disinflationary and run.

‘Tis a tailwind for AUD while it does.