Albert Edwards of Societe General with a few recessionary inputs after my own heart.

—

One of the biggest surprises in recent weeks has been some of the profit disappointments coming out of the big US retailers who had, until now, generally been considered pretty immune to an economic slowdown. This news increased concern about recession – but not necessarily for the right reasons. Excessive stocks, or inventories, seem to be a big issue among retailers and cutbacks will now occur along the supply chain. Could it be that US demand for Chinese imports gets hit hard just when the Chinese authorities are struggling to revive their moribund economy?

The FT’s Robert Armstrong, in his excellent daily note last Friday, really made me think. Robert wrote, “First-quarter earnings from two big American retailers scared the daylights out of markets this week. Walmart and Target are down 20 per cent and 29 per cent, respectively, since they reported. These two companies are very important for investors because — as nation-spanning sellers of food, clothes, home goods and much else —they provide a window into the health of the American consumer, who drives the American economy and the world’s. So it is not totally illogical that in the wake of the box stores’ poor results, all sorts of consumer staples companies, usually a safe haven in a storm, took a whipping.”

It wasn’t revenues that were the primary cause of the profit disappointment. Rather it was sharply declining margins that many then attributed to rising costs – especially labour costs. However, Armstrong points out that in fact it was the cost of dealing with unwanted inventories that had squeezed margins. He wrote “At Walmart, sales were up 2% from last year’s first quarter. Inventories were up 32%. That is to say: there was $15bn in extra inventory sitting around at Walmart at the end of the quarter. At Target, it was 4% and 43% — $5bn in extra inventory. And what happens when you’ve ordered several billions worth more stuff than your customers want? You mark prices down to get rid of it all. And down go margins.”

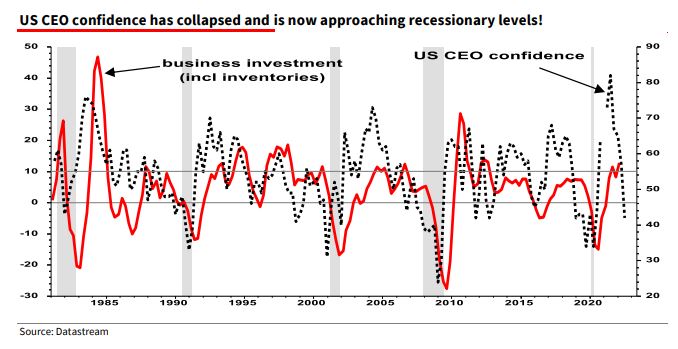

Although inventory liquidation might be good news for taking the heat out of rampant inflation, it certainly isn’t good for future GDP growth as orders will need to be slashed. It got me thinking, if this is a more general problem maybe it helps explain why US CEO confidence has collapsed recently – something which normally precedes an investment downturn. Swings in inventories often dominate the business investment cycle and invariably cause recessions.

Although the title on my business card is “Global Strategist”, my background is as an economist. I was trained in the econ-arts some 40 years ago while working as an applied econometrician at the Bank of England on their economic model. I survived that experience but vowed never to run a regression ever again – and what a release that was!

Despite this close shave with nerd’dum, my economics apprenticeship gave me a good grasp of national accounts and flows of funds (as well as some lifelong friends) so I must thank them for that. But that’s also why I get excited by geeky economics things like inventory data – how sad!

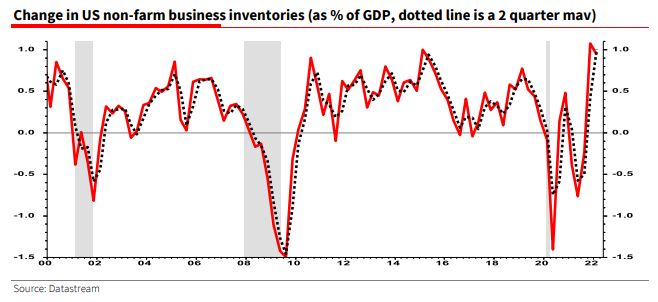

Hence after reading Robert’s note on Walmart and Target’s excess inventory problem, I decided to sniff around the macro data. Going back to the advance Q1 US GDP release, I noted that after business inventories declined in Q3 of last year (by $46bn), they surged in both Q4 of last year (by $212bn) and again in Q1 of this year (by $185bn) – which is around 1% of GDP (see chart below).

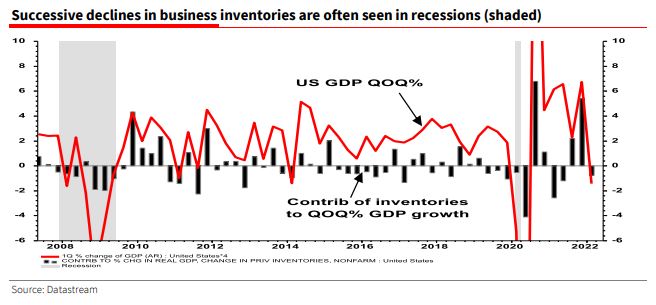

But as you may know, inventories contributed to the surprise 1.4% decline in the advance measure of Q1 GDP – contributing fully minus 0.75% (see chart below). That is because, as was drilled into me at the BoE, it is the change in the change in inventories that contributes to GDP growth (ie changes in production relate to changes in the rise or fall of inventories). Hence despite inventories still piling up at an almost record $185bn rate in Q1, they still knocked 0.75% off GDP growth because that was lower than the $212bn rise in Q4 2021.

If you haven’t lost the will to live and have hit the delete button already you may well be asking yourselves, why am I boring you with this geeky econ-trivia? It is because unanticipated excess inventory build-ups, especially during a Fed tightening cycle, can help to trigger a recession. And although inventories deducted 0.75% from Q1 advance GDP growth, they had still risen unusually quickly. The inventory elephant is still filling the room.

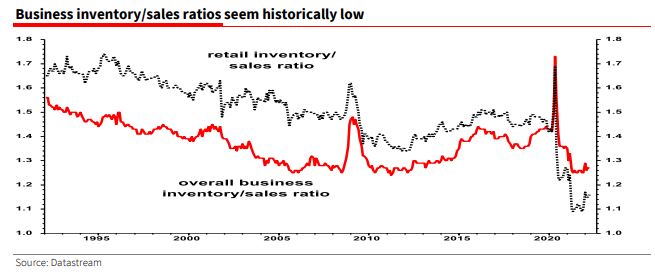

At first sight it seems odd to hear reports of excess inventory in the US when there are so many reports about supply interruptions. And indeed, overall inventory/sales (I/S) ratios look exceedingly low both for the retail sector and businesses overall (see chart below).

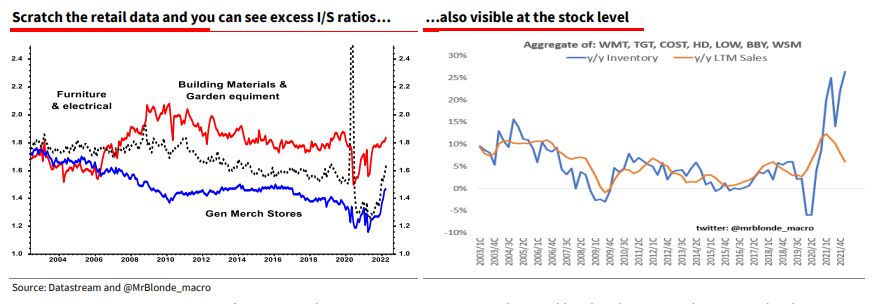

The very depressed retail I/S ratio is though almost entirely due to the shortage of auto inventories. Looking elsewhere in retail you can see a surge in I/S ratios in some of the key retail categories (see left-hand chart). And just to ram the point home, @MrBlonde_macro tweeted the chart below right with the comment, “Remember late last year when the majority was talking about supply chain bottlenecks and inventory shortages? They couldn’t have been more wrong.”

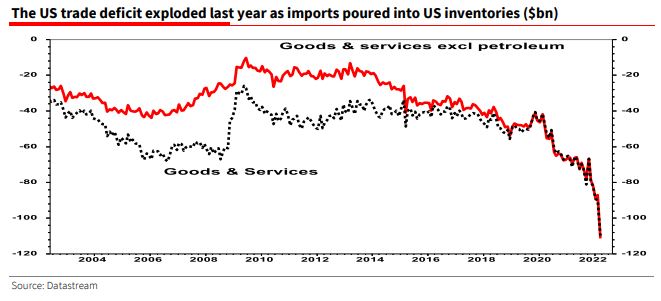

If we accept there is an inventory issue at the retail level in the US, producers are clearly going to see orders cut. This chart below gives you a clue that the pain might be felt most keenly outside of the US. China is likely to be especially hard hit – just at a time when the authorities there are desperately trying to revive growth. While I think it is only a matter of time before the Fed capitulates, maybe it will actually be China that is forced to (re-)open the liquidity floodgates first.