Well, we have our answer. It’s lying our way to prosperity with our ears pinned back. This year’s Budget outlook assumptions have a veneer of credibility but scratch the surface and it becomes troublesome. Go deeper and it turns completely and catastrophically laughable.

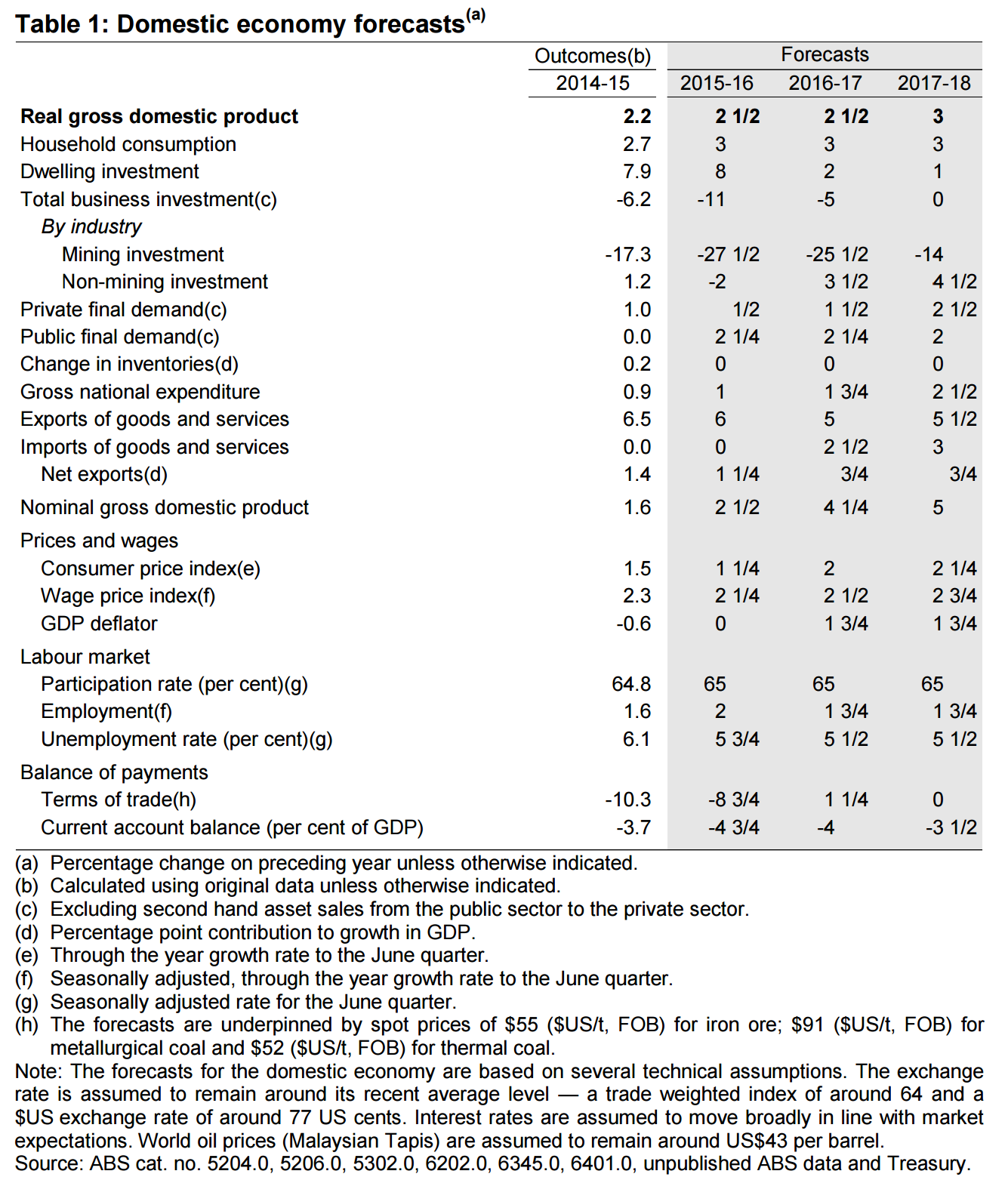

Here are the headline numbers:

From the top down:

GDP outlook could be seen as cautious;

household consumption is fair enough given it assumes a further savings run down, so long as you accept households are happy to do it (a big if);

we already know that dwelling investment has peaked so it won’t be growing next year and will be tumbling the year after;

business investment is far too high. The ongoing mining capex collapse is right but non-mining is currently projecting -18% in the ABS capex survey for 2016/17 not plus 3.5%;

net exports looks conservative;

income growth is too high and the assumed rate of productivity growth is 1.6% versus it actually falling over the past year;

nominal growth is far too high for reasons I will come to;

all of the inflation numbers are too high for reasons I will come to;

the unemployment rate and employment growth are reasonable all things being equal;

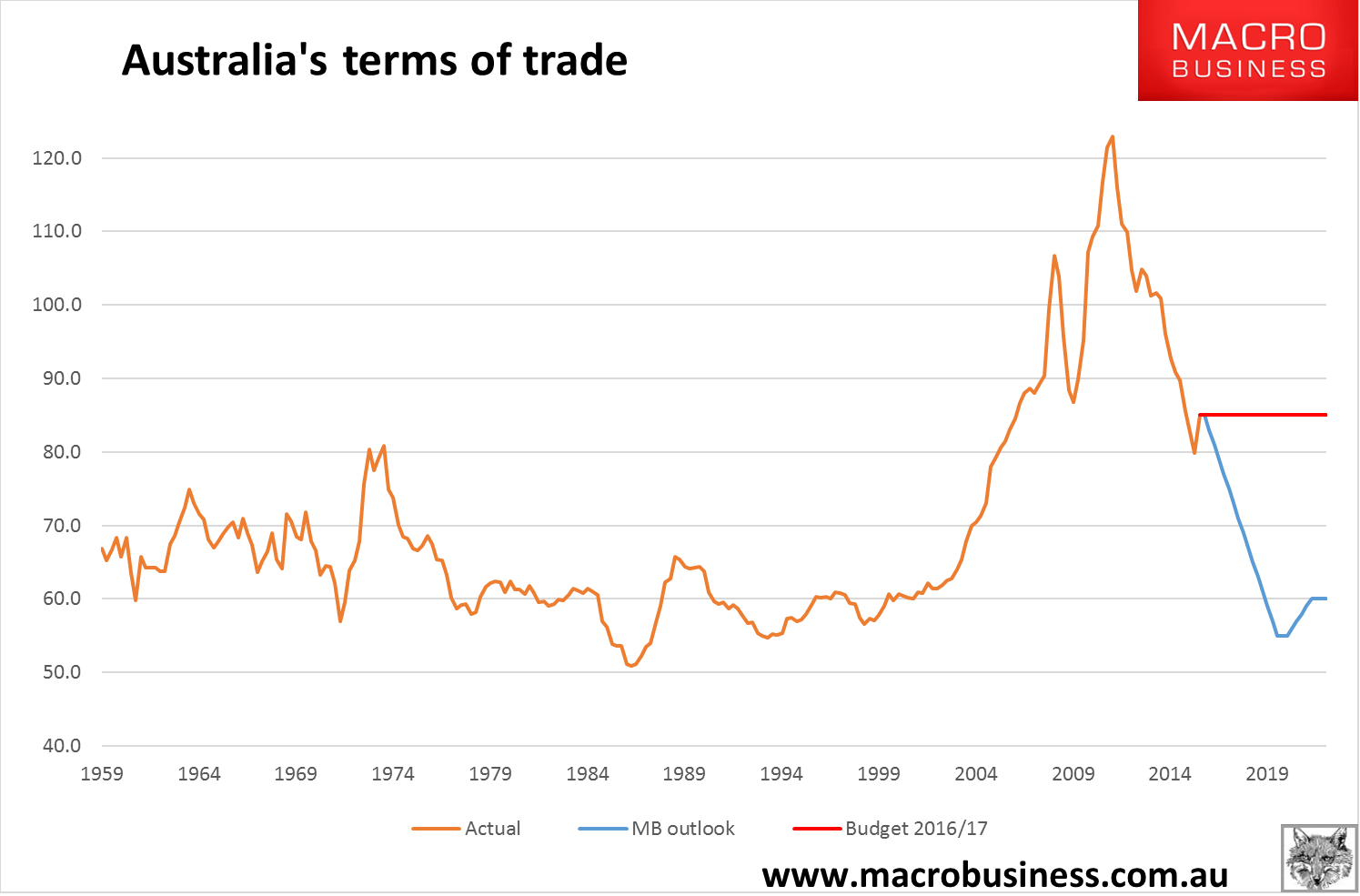

the terms of trade is farcical and looks like this:

Advertisement

According to Treasury, Australia’s terms of trade are going to settle at a gentlemanly plateau far higher than they have even been in history outside of the China boom.

That may boggle the mind but when one marries it up with other assumptions it runs to comedy. China is going to continue to successfully rebalance away from the very investment that drives demand for the commodities that underpin Australia’s terms of trade. And it will slow consistently too:

A period of extraordinary growth has made China one of the largest economies in the world. Australia benefited significantly as demand for Australia’s commodities surged, leading to a record increase in mining investment in order to expand capacity. Australia is now benefiting from increasing commodity exports. China is entering a new stage of development, which the authorities have characterised as the ‘new normal’. The Chinese economy now faces the task of transitioning to a more balanced growth model. Unlike recent decades, growth will increasingly be driven by consumption and services, and be less reliant on investment.

Advertisement

Yet that outcome is going to result in the following for iron ore and coking coal which represent half of the terms of trade:

Continuing the approach taken at the 2015-16 Budget, the price of oil and key commodity export prices that underpin the forecasts are based on a recent average.

Iron ore prices have risen recently in US dollar terms. The iron ore price underpinning the forecasts is $US55 per tonne Free on Board (FOB), compared with $US39 per tonne FOB at the 2015-16 MYEFO. Metallurgical coal is also a key input into steel production. The metallurgical coal price is $US91 per tonne FOB compared with $US73 per tonne at the 2015-16 MYEFO. The price of thermal coal remains unchanged in US dollar terms since the 2015-16 MYEFO.

Although prices for some key commodities have increased in US dollar terms since the 2015-16 MYEFO, the overall impact on nominal GDP has been partly offset by an appreciation in the Australian dollar. Australia’s key commodities are traded in US dollars and a higher exchange rate has reduced the price exporters receive in Australian dollar terms. The exchange rate is now assumed to be 77 cents against the US dollar compared with 72 cents at the 2015-16 MYEFO.

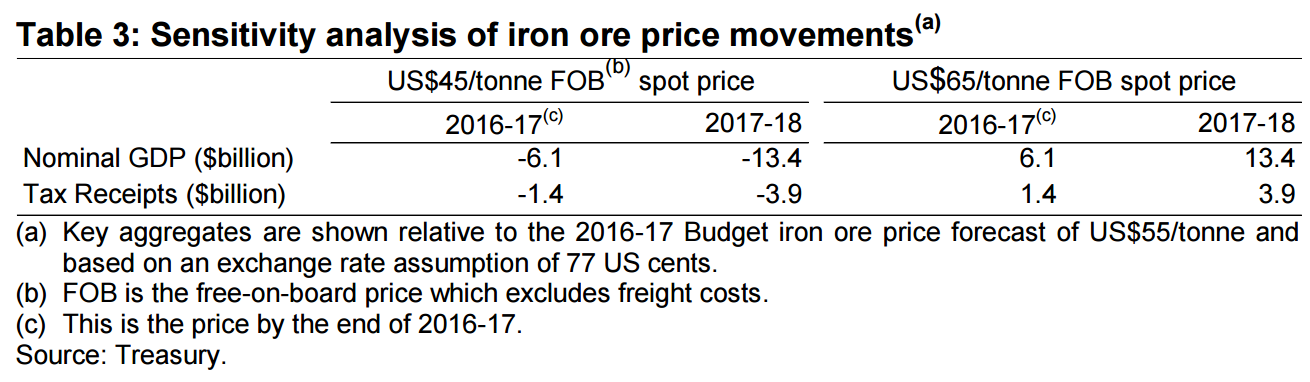

A key risk to the nominal GDP forecast is the volatility and uncertainty around movements in commodity prices. The inherent uncertainty around both supply and demand factors means the outlook for the price of iron ore is subject to considerable risk.

The impact of iron ore prices being US$10 per tonne lower/higher, based on the sensitivity analysis presented in Statement 7 is set out in Table 3. A US$10 per tonne reduction/increase in the iron ore price results in just over a $6 billion reduction/increase in nominal GDP in 2016-17. These illustrative impacts differ from those presented in the 2015-16 Budget due to a more comprehensive analysis presented in this year’s Statement 7. In particular, the sensitivity analysis now assumes that export commodity prices fall/rise over the course of a year rather than an immediate movement. The effect of this is to reduce the impact in the first year of the analysis. The effect in the second year is in line with the earlier sensitivity analysis. For purposes of comparison an immediate fall/rise in the iron ore price would have a direct effect in the first year of around an $11 billion reduction/increase in nominal GDP in that year.

And here we come to it. The Budget assumes an iron ore price of $60 spot ($55 FOB) across the forward estimates. It hasn’t used Singapore futures as a guide, which would give it a price of $43. It hasn’t used Chinese futures which would give it a price of $48. It hasn’t used sell side research which would give it a price around $40.

Advertisement

It has used a recent average price during the most spectacular mini-bubble in spot pricing in living memory.

One can only view this as a deliberate lie. When you plug in the the falls that are actually ahead, a price of $35FOB for 2016/17, $30FOB for 2017/18 and $25FOB for 2018/19 then you need to subtract more than -1.5% in nominal GDP from the year ahead and much more further out. For tax receipts its -$8bn next year and much more further out. These figures will be mitigated by the use of the 77 cent dollar forecast which offers some insurance as it will fall much further than that over the forecasting period but it is an offset not trend changer.

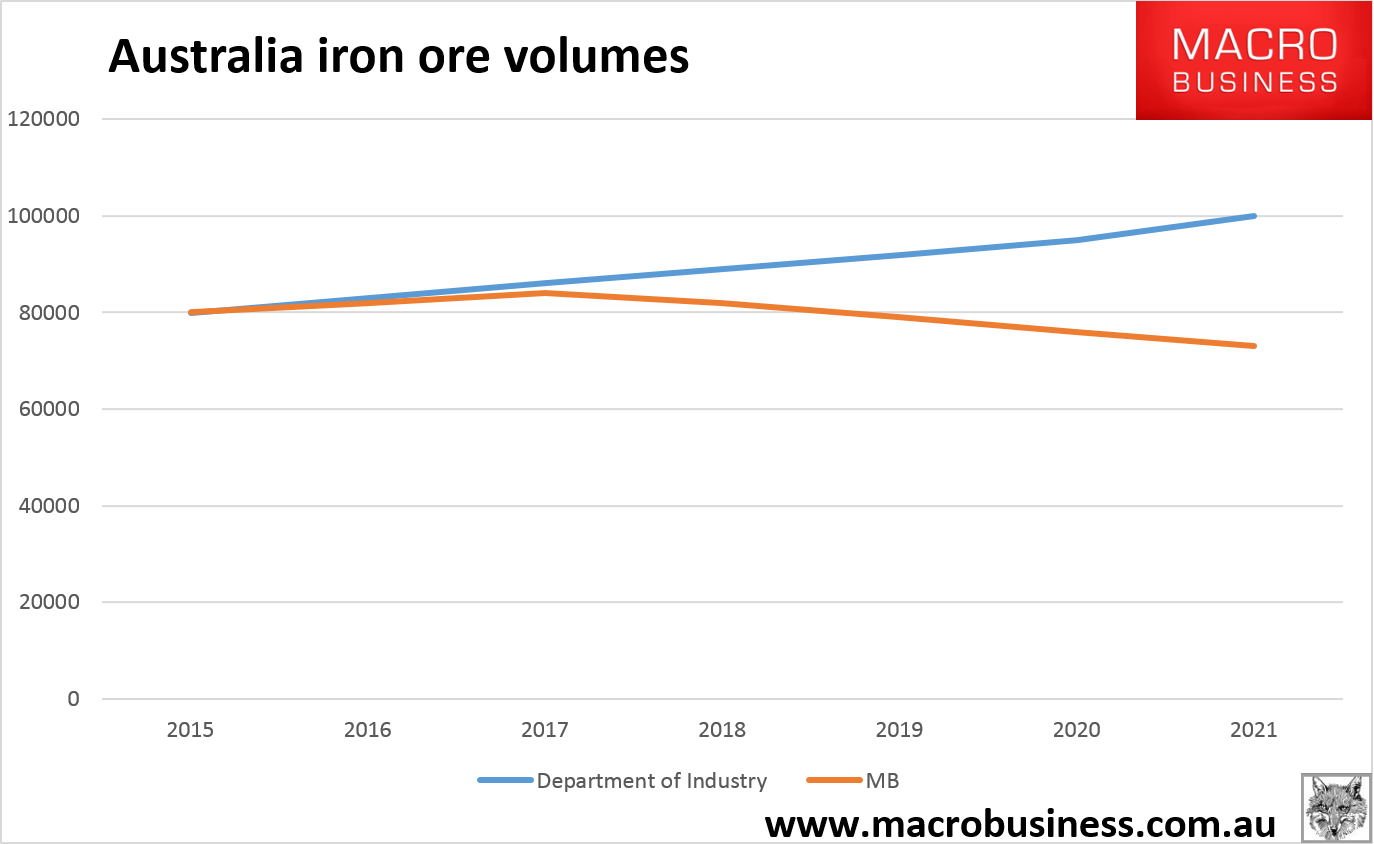

Moreover, it appears Treasury has relied upon the outright fantasies of the Department of Industry’s Office of the Chief Economist which sees ceaseless volume growth with stable prices:

Advertisement

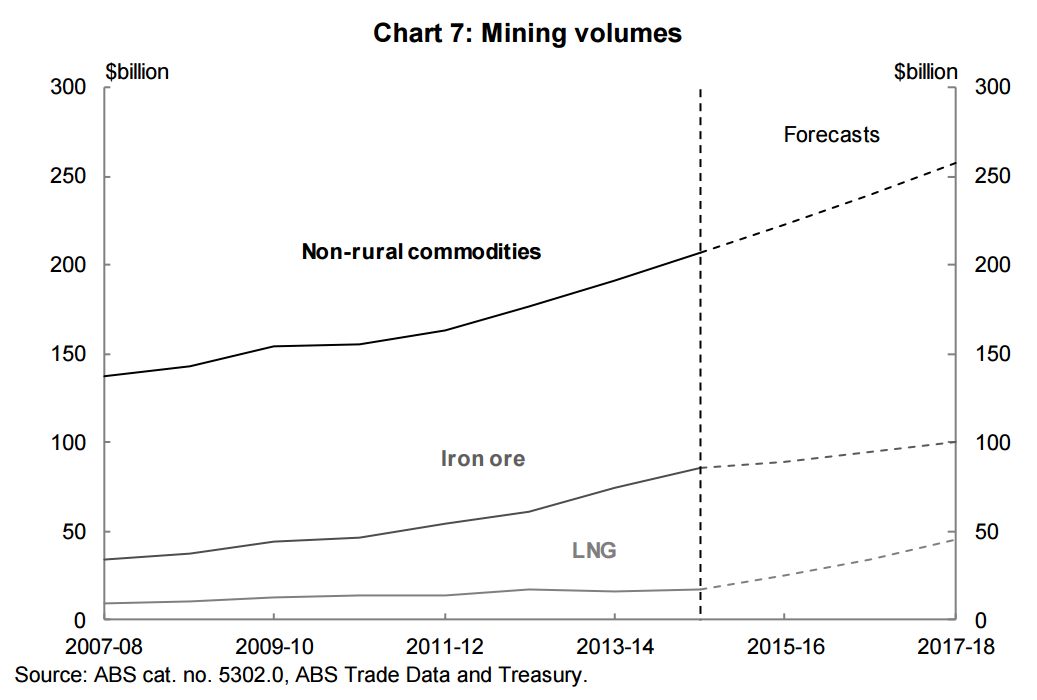

That said, the resource sector continues to underpin growth in total exports with iron ore and LNG production continuing to ramp up after the investment phase of the mining boom. Mining exports are expected to increase by 7 per cent in 2016-17 and 7½ per cent in 2017-18. In 2015, Australia exported over 760 million tonnes of iron ore, with 625 million tonnes exported to China. This compares with 240 million tonnes of iron ore exported in 2005, with almost 120 million tonnes exported to China. In 2015, China’s imports of Australian iron ore increased by around 11 per cent with Australia increasing its share of the Chinese iron ore market. Over the forecast period iron ore exports are expected to increase by around 16 per cent, while LNG exports are expected to continue to grow strongly, with the Department of Industry, Innovation and Science forecasting exports to triple between 2014-15 and 2020-21 (Chart 7). 1

These are the fantasies of a corrupt (consciously or otherwise) Banana Republic institution that is unable for whatever reason to imagine anything other than endlessly rising dirt exports and prices to underpin local demand. The truth is that a few years out iron ore volumes are going to fall not rise and begin detracting from GDP even as prices keep falling as well, as first the juniors go bust and then the higher cost major’s production is shut-in:

Advertisement

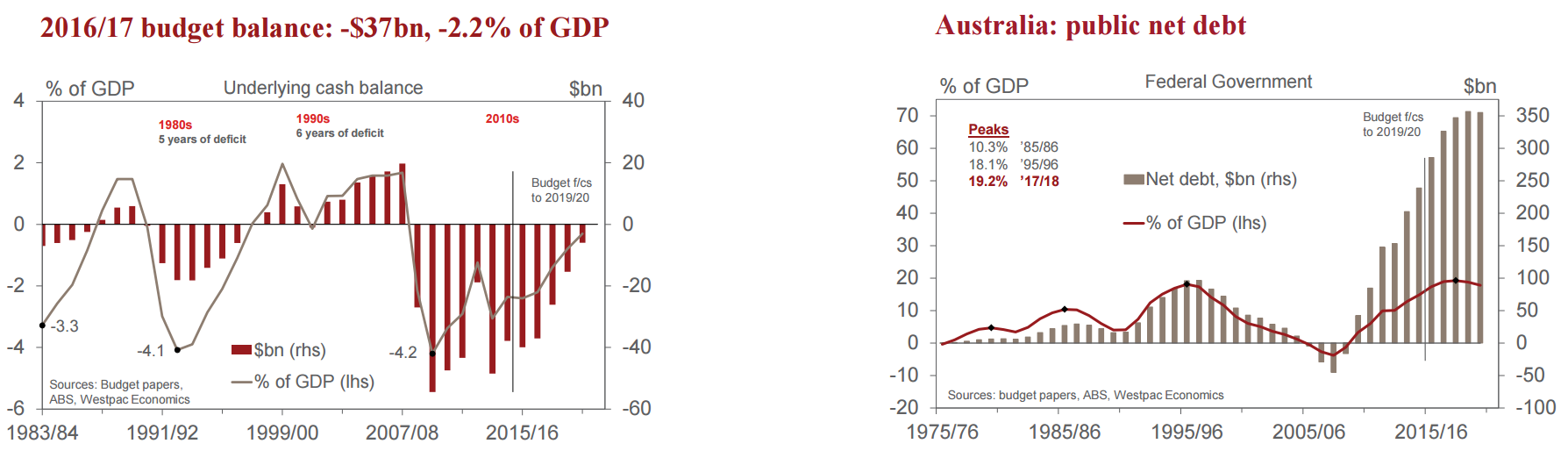

None of this is to say that the nominal GDP targets can’t still be reached. What makes no sense is how they will be achieved. Once you plug in realistic terms of trade forecasts the only way that nominal growth can accelerate and labour markets be maintained is via more borrowing, both public and private, that in turn means the deficit forecasts are more comedy, from Westpac:

The Commonwealth Government’s net debt position remains manageable, well below other AAA-rated sovereigns. From a starting point of 14.8% of GDP in 2014/15, net debt is expected to rise to 17.3% in 2015/16 (versus 16.8% at MYEFO); 18.9% in 2016/17; and a peak of 19.2% in 2017/18 (compared to 17.9%in MYEFO). Thereafter, it is expected to edge lower, ending the forecast period at 17.8% in 2019/20 – only marginally higher than its 2015/16 level. The stock of Commonwealth Government Securities on issue at June 2016 is expected to be $427bn; it is expected to rise to $584bn by June 2020, little changed in scale relative to GDP, circa 29%.

Finally, this all means that the current account deficit will continue to widen not contract as forecast. It is pure Banana Republic economics, lying about dirt exports to disguise a mushrooming external debt problem so that the government of that day need not enact reform and can protect entrenched rent-seekers.

Advertisement

Anyway, there you have it. This was the easiest to destroy set of Budget assumptions that I have seen in a decade of covering them. The reason why is simple: the iron ore assumptions that flow into nominal growth and sustained tax receipts are a fairy tale. Every bit as bad as the WA budget at its worst.

This Budget has guaranteed the loss of the Government’s credibility in the next term, guaranteed an ongoing confidence shock to households to go with it and guaranteed the loss of the AAA rating within 12 months.

Frankly, on this evidence, we deserve nothing less.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.