Society Generale uber-bear Albert Edwards holds a special place in markets. Anyone else making his dire predictions would long-ago have been flushed-away as a crack-pot. But it was Edwards who very successfully described the GFC in advance and coined some of its terminology, most pointedly the “Ice Age” thesis that Western economies were going to follow Japan into a long and destructive deflationary cycle. Well, he’s back:

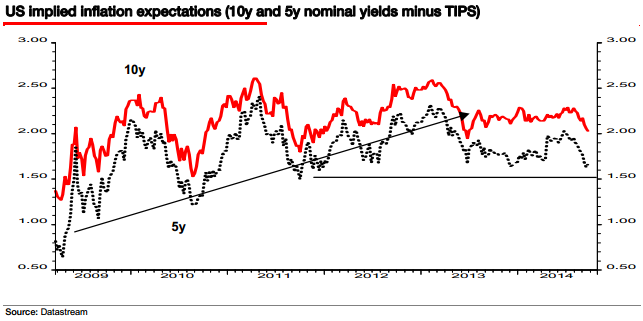

Inflation expectations in the US have just followed the eurozone by plunging lower. Until very recently, the Fed and the ECB had been quite successful at keeping inflation expectations in their normal range – this despite their clear failure to control actual inflation itself, which has consistently undershot expectations. Investors are beginning to realise that contrary to their confident actions and assurances, the Fed and the ECB have failed to prevent a dreaded replay of Japan’s deflationary template a decade earlier in the West. The Ice Age is once again about to exert its frosty embrace on markets as investors wake up to a new and colder reality.

Ive had a lot of requests of late to resend our Ice Age thesis. This is usually a good indication that we have again reached that point in the cycle where investors are willing to start valuing risk properly again. I will update readers with my full Ice Age thesis shortly…

There were two key parts to our Ice Age thesis. First, that the West would drift ever closer to outright deflation, following Japan’s template a decade earlier. And second, financial markets would adjust in the same way as in Japan. Government bonds would re-rate in absolute and relative terms compared to equities, which would also de-rate in absolute terms. This would take many economic cycles to play out. Previous US equity valuation bear markets have taken 4-6 recessions to complete weve only had two thus far.

Another associated element of the Ice Age we also saw in Japan is that with each cyclical upturn, equity investors have assumed with child-like innocence, that central banks have somehow fixed the problem and we were back in a self-sustaining recovery. Those hopes would only be crushed as the next cyclical downturn took inflation, bond yields and equity valuations to new destructive lows. In the Ice Age, hope is the biggest enemy.

Investors must pay close attention to the (second most important) chart below. Investors are beginning to see how impotent the Fed and ECBs efforts are to prevent deflation. And as the scales lift from their eyes, equity, credit and other risk assets trading at extraordinary high valuations will take their next giant Ice Age stride towards the final denouement.

In broad terms I agree, though it could well be thirty years in the making…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.