Some time ago I wrote a piece on why the US Treasury “no brainer trade” doesn’t work. That trade is the unwind of the US bull market in Treasuries, which has run for three decades, as inflation rebounds on money printing.

Over the last few decades, many have promoted a similar trade in Japan following its bubble, bust and huge accumulation of public debt. But it has become known as the “widow maker”trade because the bear market and blowout in yields never eventuated.

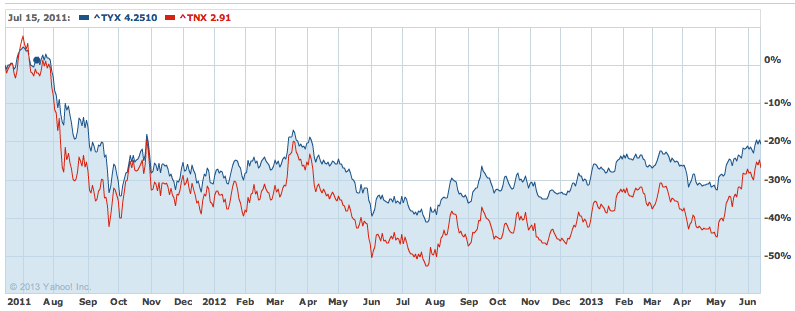

The US equivalent trade has been working fine over the past month as the Fed’s discussion of “tapering” has taken hold and bond yields have surged (remember that yields rise as investors abandon bonds so those that are short are in the money) . Here is a two year chart of the 10 year and 30 year bond yield with recent spikes and steady up trends since mid last year:

Advertisement

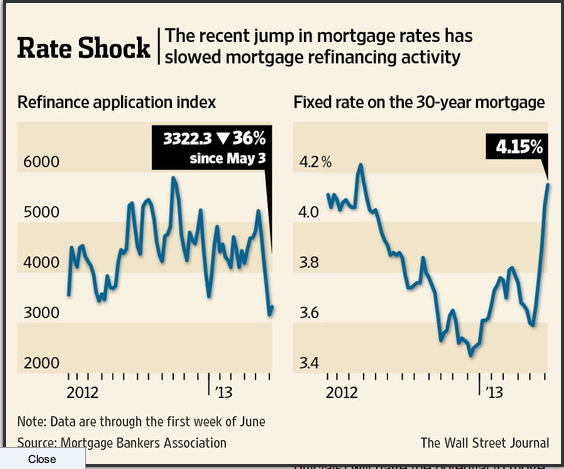

The problem with the US version of the “widow maker” trade is this. Most US mortgages are fixed rate and attached to the 30 year bond yield. So, the recent spike has done the following to new US mortgage rates:

Advertisement

Rates are now at their highest since early 2011. Obviously this is the equivalent of two rate hikes for anyone considering entering the US housing market. Moreover, it cuts off one of the prime sources of financial and real economic activity in the US: refinancing. Holders of US mortgages can only enjoy lower interest rates by refinancing their fixed rate loans. This leads to great stampedes to do so when rates fall and equally large collapses when rates rise. The WSJ has more:

A surprise spike in mortgage rates threatens to halt a refinancing boom that has delivered strong profits for U.S. banks over the past two years. The average rate on a 30-year mortgage rose to 4.15% last week, a 14-month high and up sharply from 3.59% in early May, according to the Mortgage Bankers Association. A separate survey released Thursday by Freddie Mac FMCC -15.88%said the rate this week was at 3.98%, up from 3.35% last month. Refinancing applications last week were down 36% from the first week of May, before rates began climbing, according to the bankers association. Lenders have been predicting that refinancing would taper off, “what wasn’t anticipated was that this move in rates would happen so quickly,” said Bose George, a mortgage-finance company analyst with Keefe, Bruyette & Woods.

I guess business and business media are the same the world over. This was eminently predictable. It happens every time US long bond rates rise. It’s supposed to happen, if not quite so suddenly. Refi application rates are now in the 2009 range.

Advertisement

Moreover, in the US economy there is a strong correlation between refinancing activity, pending home sales and house prices. It’s not obvious why. Perhaps many of those refi clients are clearing the decks before selling their properties, which is odd. Most likely, it’s a coincident not causal relationship. When mortgage rates rise, they choke off refis and new mortgages.

Other dimensions of the US housing recovery remain on track. Inventories are still improving (though the shadow inventories are still there) and for construction there is still promise of a recovery as household formation firms up.

But the historic relationships suggest that declines in refinancing activity of this magnitude foreshadow a slowing US housing market. That recovery is one leg in a three legged US economic recovery: the gas revolution, the manufacturing rebirth and the housing recovery. The second is already under pressure via weak external demand. The Fed cannot let housing slip back now as well.

A key Bank of England policymaker has warned of the risks to global financial stability when “the biggest bond bubble in history” bursts.

In a wide-ranging testimony to MPs, Andy Haldane, Bank of England director of financial stability, admitted the central bank’s new financial policy committee is taking too long to force banks to hold more capital and appeared to criticise the bank’s culture under outgoing governor Sir Mervyn King.Haldane told the Treasury select committee that the bursting of the bond bubble – created by central banks forcing down bond yields by pumping electronic money into the economy – was a risk “I feel acutely right now”.

…”If I were to single out what for me would be biggest risk to global financial stability right now it would be a disorderly reversion in the yields of government bonds globally.” he said. There had been “shades of that” in recent weeks as government bond yields have edged higher amid talk that central banks, particularly the US Federal Reserve, will start to reduce its stimulus.

“Let’s be clear. We’ve intentionally blown the biggest government bond bubble in history,” Haldane said. “We need to be vigilant to the consequences of that bubble deflating more quickly than [we] might otherwise have wanted.”

The IMF also warned the Fed on Friday while cutting its US growth forecast to 1.9% this year and 2.7% next year:

Advertisement

…a long period of exceptionally low interest rates may entail potential unintended consequences for domestic financial stability and has complicated the macro-policy environment in some emerging markets. While the Fed has a range of tools to help manage the exit from its current highly accommodative policy stance—including adjusting interest on excess reserves and conducting reserve-draining operations with an expanded list of counterparties—unwinding monetary policy accommodation is likely to present challenges. The large volume of excess reserves and the segmented nature of U.S. money markets could affect the pass-through of policy rates to short-term market rates. At the same time, effective communication on the exit strategy and a careful calibration of its timing will be critical for reducing the risk of abrupt and sustained moves in long-term interest rates and excessive interest rate volatility as the exit nears, which could have adverse global implications, including a reversal of capital flows to emerging markets and higher international financial market volatility.

Exactly right. The problem for the Fed is that the inflation that the widow maker trade enthusiasts always expect may not have appeared in the real economy but it certainly has in asset markets. So the Fed needs to keep QE running for US housing but in so doing it only feeds the bubbles in global government bonds, junk bonds, global equities and everything in emerging markets. Even a hint of withdrawal sends an earth tremor through the lot.

Once it rolled the dice on QE, the Fed inherently limited its ability to withdraw stimulus. The alternative path of low but not negative interest rates would have meant a much longer, more painful and more real recovery.

Advertisement

But that’s history, it chose the path of boom and bust and so the widow maker trade will roll on. If the Fed tapers, bond yields will lurch higher as global hot money runs, the recovery will be hit and yields will tumble again on economic weakness (and more QE). Or, the Fed won’t taper and bond yields will fall.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.