CBA’s shares hit a record high of A$74.18 Monday and are up almost 50% over the past year. That means its stock is trading at 10.2 times its profits before accounting for provisions to cover bad debts, UBS says.

CBA’s tangible book value of 3.6 times is also the highest in the world, according to UBS analyst Jonathan Mott.

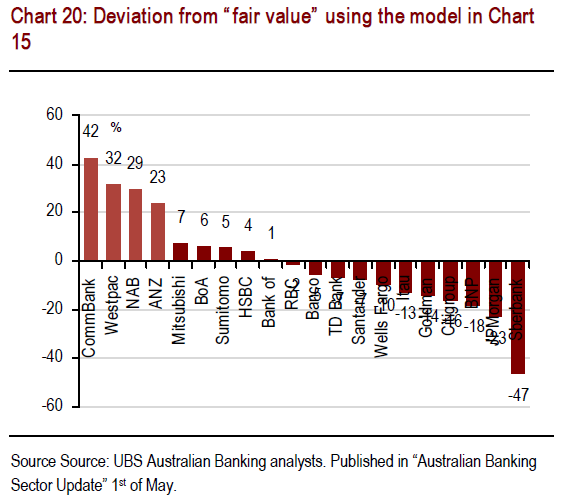

“This makes CBA the most expensive large bank in the world by nearly every measure,” Mr. Mott, who is based in Sydney, said in a note to clients. He rates the bank a sell with a price target of A$60.

…Behind the strong headline results, however, Australia’s banks are struggling to maintain profit growth as the country’s resources boom starts to fade. Investment in resources, such as natural gas or iron ore for export to Asia, has been an engine for the economy over the past decade.

Much of the boost to bank profits has come from cost-cutting and falling bad debt charges, which analysts say will lose momentum in the coming year. Revenue growth and demand for credit have remained weak.

“The optimization of bank earnings is reaching its limit, with bad debt charges as feasibly low as they can get, margin expansion and the pace of productivity improvements fading,” said Credit SuisseCSGN.VX +1.74% analyst James Ellis.

From the perspective of UBS,it is actually a little worse than this. In a recent note, it went looking for global asset bubbles and found five:

Advertisement

Where are the asset bubbles?

A guide on how NOT to invest

Most of the pieces you will read provide investment advice, but this one is about how not to invest: we look at potential bubbles. Arguably there are a number of asset classes that are “rich”, this does not necessarily make them candidates for being “bubbles”. We take a restrictive definition of an asset bubble: the asset has (1) to be valued beyond the reasonable bounds of fundamentals and (2) could correct rapidly. This leaves us with only five candidates.

Five “suspects”

On the above definition of “bubble”, we find five markets that fit our bubble criteria: (1) Risk free rates as we think Treasuries and bunds have departed from fundamental value, we also believe that a large sell-off in JGBs is a distinct possibility, (2) in credit space valuations do not look unreasonably stretched but the lack of liquidity in the market could engineer an adjustment that looks like a bubble bursting, (3) physical real estate in Asia although we acknowledge that the pricing of listed real estate is more justifiable on fundamental grounds, (4) a number of EM equity markets, namely Indonesia, the Philippines, Thailand and Mexico, (5) Australian banks.

Mainly a consequence of ultra-loose monetary policy

A common theme that emerges from this piece is that the main driver for the bubbles we have identified is ultra-loose monetary policy. By pushing risk free rates to an unprecedented low level, central banks run the risk of creating a disorderly return to normal in this space. Hence we believe that the real danger zone will come when central banks start to normalise their policy.

The out-performance of banks is also cast in an interesting relief by an interesting observation from Phil Baker at the AFR today:

While the hunt for yield has made sure this bull market is different to others, with the major banks and Telstra leading the way, on Wall Street the rally so far this year is very broad.

According to Bloomberg, 90 per cent of companies in the small cap index, known officially as the Russell 1000, have risen in 2013, the most in at least 18 years.

Gains this year in the Russell index mirror very closely the gains made by the broader S&P 500 index – both are around 17 per cent.

Indeed, Goldman Sachs and Bloomberg took a look at companies with huge debts, the lowest working capital and smallest earnings and despite those drawbacks discovered they are still shooting the lights out with a 27 per cent gain this year.

Advertisement

Meanwhile, in Australia:

The small cap index without dividends is still 90 per cent from its 2007 record high while if dividends are included it’s still 60 per cent from its high. There’s a good reason why the performance of small caps here and in the US are so different.

There are a lot of mining stocks in the major index and also the small cap index, and these names haven’t been in favour for the past few years as China’s economy has cooled.

That’s a reason but it’s not a good one.

Let’s be fair. CBA is a money printing machine with its dominant market share, its free government guarantees and its huge pricing power. But it is only as good as the economy that underpins it. With this rate cycle so far having produced one of the lowest responses in history as well as with the rapid approach of the mining investment cliff, which is very likely to result in an at best bumpy rebalancing for the economy, CBA is not appropriately discounted for the risks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.