As the world of investment spruiking clears its throat for another roar on the back of the latest interest rate cut, the two obvious Australian plays are once more buy banks and/or property. But which one?

JPMorgan has a nice note out this morning summarising the variables in answering this question. Focused on the banks, which are a themselves a pivot between property and shares.

Renewed Monetary Policy Easing Will Test The Appetite For Yield Banks

Ongoing improvements in the pricing of long term wholesale funding (even compared to one month ago!) has given Australian banks increased confidence relating to future margin run rates. Accordingly, CBA, NAB, WBC and BOQ have today announced that they will be passing on the RBA rate cut reduction in full.

However, the broader question is whether a lower cash rate (and likely deposit rates) will continue to support the yield gap argument and allow banks to continue to trade expensive relative to fundamental valuations, or will evidence of further support being required for the domestic economy start to bring the sustainability of bank earnings into question? All eyes now turn to the unemployment rate.

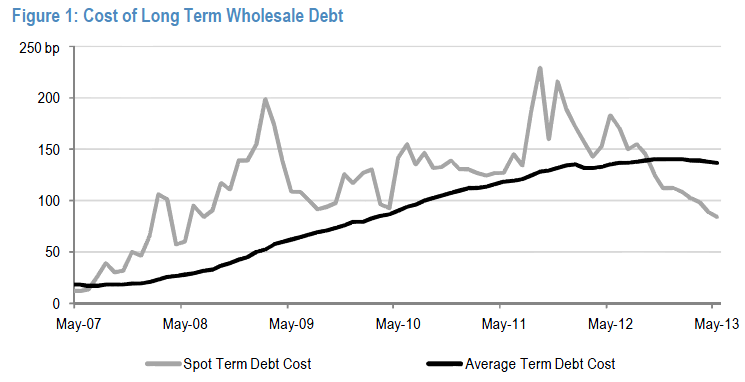

Improvements in long term wholesale funding costs are providing confidence to future margin run rates – As highlighted in our recent mortgage industry report (refer “Growth Finds A Floor, But Debt Finds A Ceiling”, on 10 April, 2013) the spot cost of funding through wholesale markets is now materially lower than the average ~140bp cost of the portfolio, the first time this has occurred since the onset of the GFC in mid-2007 (refer Figure 1).

Furthermore, the re-basing of long term wholesale spreads appears to have found an ‘additional leg’ over the last month, with 5 Yr CDS spreads declining afurther ~20bp from ~90bps to ~70bp over BBSW, holding potentially favourable implications for deposit pricing if replicated (refer Figure 2). In our view, this relatively recent improvement in the outlook for the cost of funds is behind the decision to pass on the RBA rate cut in full, noting that the typical adverse NIM impact from a -25bp reduction in the OCR and corresponding deposit compression is -2bps (refer Table 1).

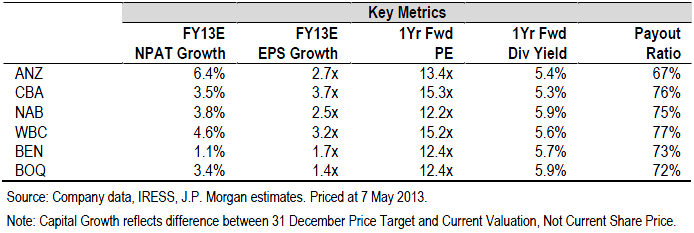

Renewed reductions to the cash rate may be taken in one of two ways – Will a lower cash rate (and likely deposit rates) continue to support the yield gap argument and allow banks to continue to trade expensive relative to fundamental valuations (refer Table 3), or will evidence of further support being required for the domestic economy start to bring the sustainability of bank earnings into question?

In our 2013 outlook piece (refer “2012 Has Been “Nice”. Will 2013 Be “Naughty”?, on 17 December, 2012), we viewed 2013 as a tale of two halves. The first half of the year held the potential to see earnings stability and the pursuit of yield by the market to drive bank share prices (up to ~30%) higher in 1H2013.

However, we are now at an interesting juncture as we approach the second half of the year. Notwithstanding above-consensus earnings and increased payout ratios (and even a special dividend with the recent WBC 1H13 result), bank share prices may be arguably beginning to show signs of fatigue, having ‘only’ performed in line with the market over recent weeks.

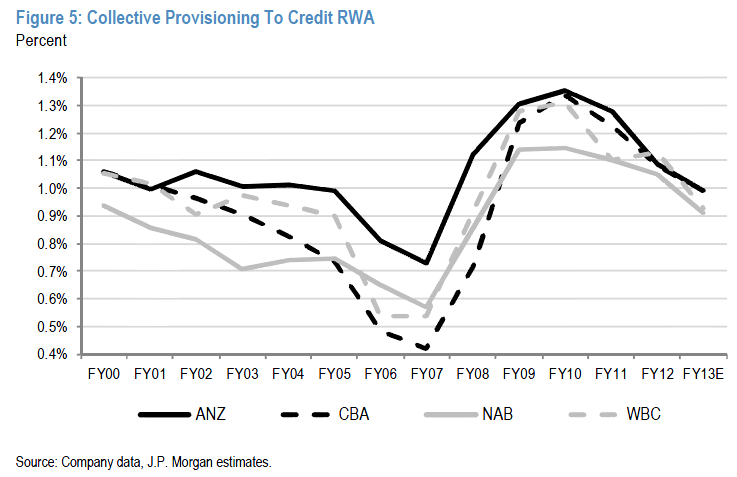

The market is well aware of the declining terms of trade, peaking capex and stubbornly high AUD all having adverse implications for the domestic economy, and therefore potentially for bank provisioning outcomes and valuations. However, the question becomes whether ongoing easing in monetary policy will be sufficient to continue to dampen and / or defer the problem. The banks provisioning cycle will lag the impacts in the real economy (under current accounting rules), and provisioning coverage is double that of 2007 levels (refer Figure 5), therefore allowing a reasonable degree of visibility.

Advertisement

These arguments precisely reflect my own thinking. I personally think that the rise in unemployment will remain mild for the next six months barring a sudden accident and there is scope for further modest inflation in bank share prices and property prices.

But there are two points to make, one short term and the other long. The latter first. It must be remembered that we are at only the very beginning of a major and historic adjustment in the Australian economy that will run for the next three years (at least). Rate cuts are happening because the RBA has so far failed to stimulate the economy enough to see us through the ongoing terms of trade correction and approaching mining investment cliff. After 175 of failed basis points I can’t see why more will help much and the weakness that is coming in the economy is not even here yet, if you’ll pardon the tautology.

The second short term point is this: much uncertainty still surrounds the timing and pitch of the mining investment cliff. We may be past it already and its slope may be as much 5-6% withdrawn form GDP over the next three years. We may not go over it until year end and the hit may constitute half of that. Moreover, when the next leg down in the terms of trade comes via iron ore prices, it will be sudden, just as it was last year.

Advertisement

That is, we could be sailing along OK this year and very suddenly find ourselves in quite a bit of trouble.

Rates are going to go lower because the dollar must fall but, in my view, the cheap money does not offset the approaching risk to house prices and bank assets. So my answer to the question posed by this post is buy neither.

Dollar hedging is what we should all be looking for. That, and staying liquid.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.