Volatility is in full force today and nowhere more so than Japan. It doesn’t matter that asset class, traders are out to play today in a big way, with the Nikkei trading in a 1459 point or 9.2% range! It’s been an incredible move, and anyone wanting to see a full-scale liquidation of a hugely over crowded trade will use this as textbook. Japanese government bonds initially pushed up to 1% on the open, but that was a bit too much and buyers have stepped in, although it has hardly been convincing. Japanese Chief Cabinet Secretary Yoshihide Suga detailed that the BoJ has done a good job in communicating its policies with the market, however he refused to comment on yields, although to be fair we want to hear more from the BoJ here.

The move in the cash market looks largely driven by the futures market, with Osaka futures getting smashed. What’s more there were monster volumes, with record volumes going through, even eclipsing the 2011 earthquake, . Data wasn’t great either, with the weekly funds flows showing Japanese domestic players sold foreign stocks (¥136 billion) and bonds (¥804 billion) after two weeks of buying. Perhaps this is a function of the higher yields and it’s something that needs to be addressed for ‘Abenomics’ to really work. Recall, like the BoE and Fed (but unlike the ECB), the BoJ is the lender of last resort, meaning it can effectively print as much money as needed and simply buy up the whole market. What a central bank wants, it usually gets.

The ASX 200 has fallen 2%% and the sell-off, as you’d expect on such a big move, falls are broad based, with 76% of stocks lower. Of course the stocks with foreign earnings have done nicely today, with AUD/USD providing them with a boost after the pair moved to 0.9606, helped largely by a poor HSBC manufacturing print. Banks have been sold with force, with the sector down 2.7%. Westpac is lower by 4.0%, with CBA the best of the four, softer by 2.7%; this looks like it has further to play out. Even the yield-plays are being taken down.

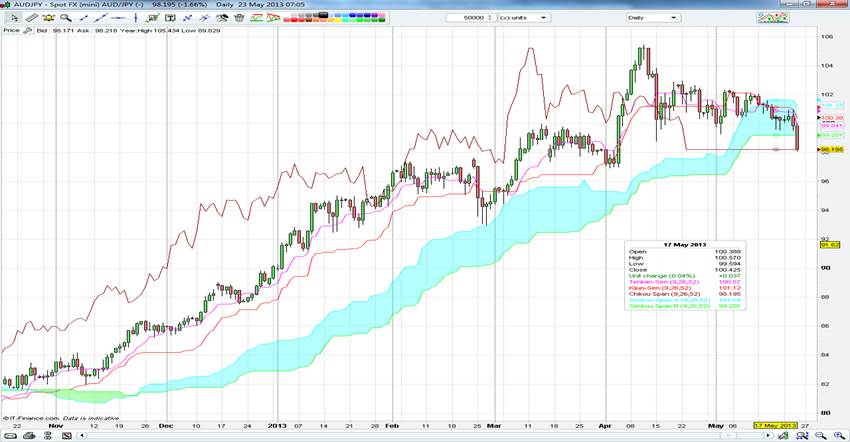

AUD/JPY has been smashed today and we’d point out that not only has it convincingly closed the 55-day moving, but it has now fallen below the bottom of the ichimoku cloud for the first time this year. This is a cross to watch and we feel this has decent downside from here, with some traders looking for a move all the way down to the 200-day moving average at 90.22. Ford pulling out of Australia emphasises the issues that are being faced in the local economy, especially after yesterday’s report from the Bureau of Resources and Energy Economics (BREE) detailing that the value of investment in Australia’s resources may drop by more than two thirds.

The Chinese PMI data came out at 49.6, down from the April final reading of 50.4 and below consensus. The new orders sub-component fell below the 50 boom/bust level at 49.5, while the employment component also showed contraction at 49.0. Chinese equities have remained flat though; sometimes it’s just incredible how this market dances to its own beat.

US futures have fallen through Asia, which is hardly a surprise given the liquidation of Japanese equities, with S&P futures down 1.1%. The S&P 500 cash market printed a bearish outside day yesterday, with the index trading up to 1687 and subsequently closing below Tuesdays’ low. Perhaps this is the pullback that many have been hoping for and we will be watching initial support at 1629.44 (the 38.2% retracement of the recent rally 1536 to 1687) to see if the bulls defend this level. US treasuries will continue to be in focus ahead of today’s ten-year auction and it will be interesting to see how traders react now they have had a bit more time to review exactly what was said from the Fed Chairman. We certainly didn’t take anything from the minutes and they went exactly to plan with certain individuals (we can guess who) calling for action sooner, rather than later from the Board. Our view is that the core of the Fed is not in a rush to curb the pace of purchases, and to be fair we feel it doesn’t actually know when it will announce policy change; of course it is now purely data dependant. We labelled the September meeting yesterday as one the market has earmarked, and this could still play out if we see two or three more months of strong payrolls. However, we need to be ready to be nimble, and weak data could easily see expectations change. Still, our strong USD call still looks promising.

European markets look set to be taken to the woodshed on the open, with 1% losses potentially on the cards, however we wouldn’t be surprised to see falls extend from the open. European PMIs will be in focus, and while the market is expecting a slight improvement in both Germany’s and France’s numbers, they will continue to be deep in contraction. Mario Draghi will speak in late European trade, while James Bullard gets another chance to speak as well, so the Fed will continue to be in focus, although he spoke on Tuesday and his views won’t have changed. The UK Q1 GDP will also be in focus, while US jobless claims will also be watched especially given how important employment is ahead of tapering.